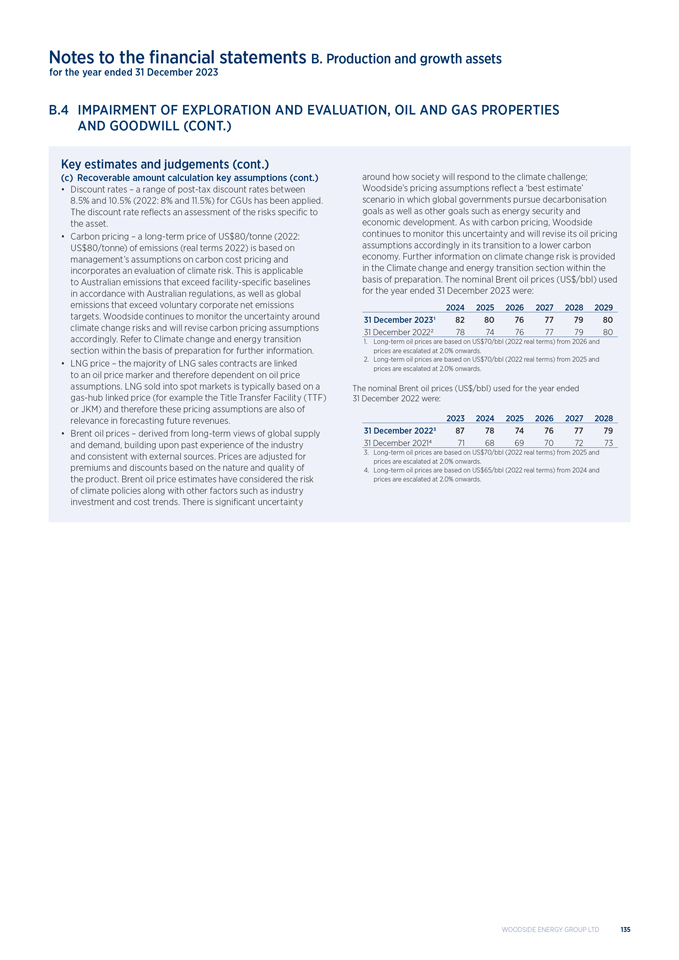

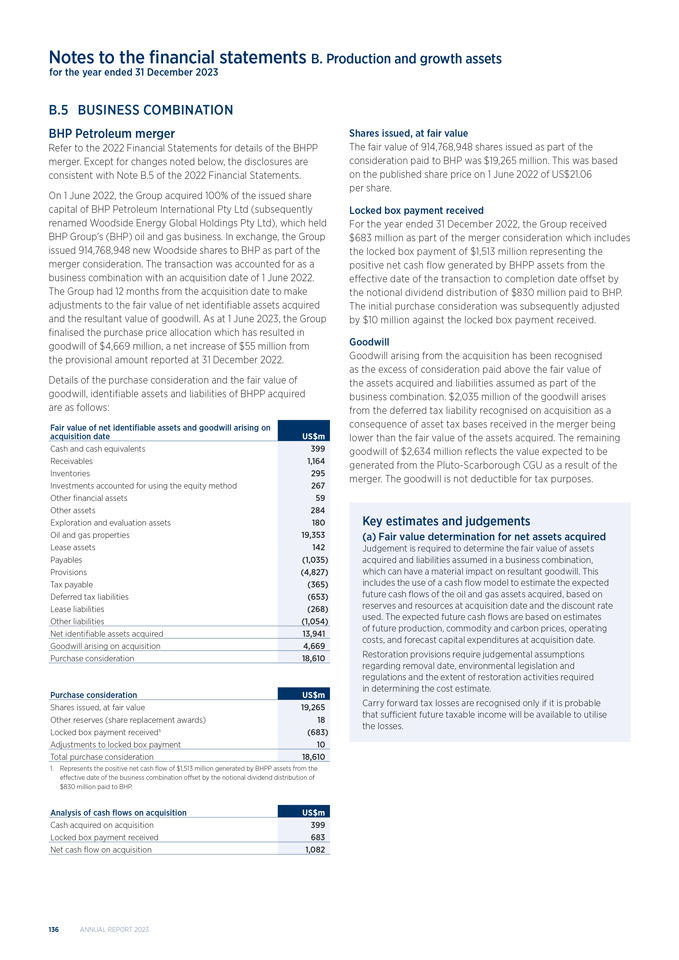

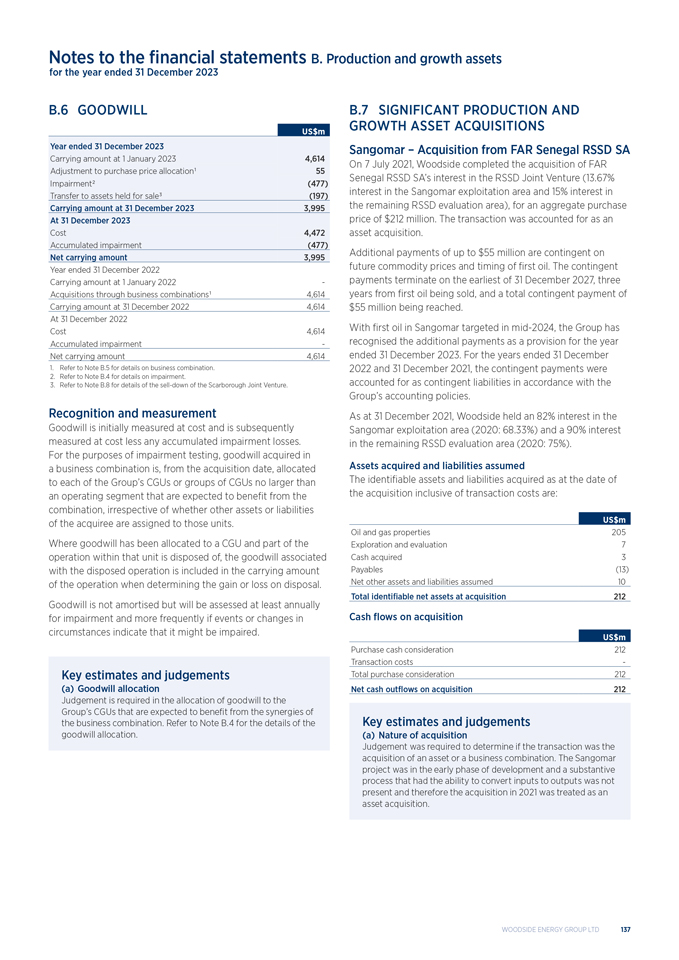

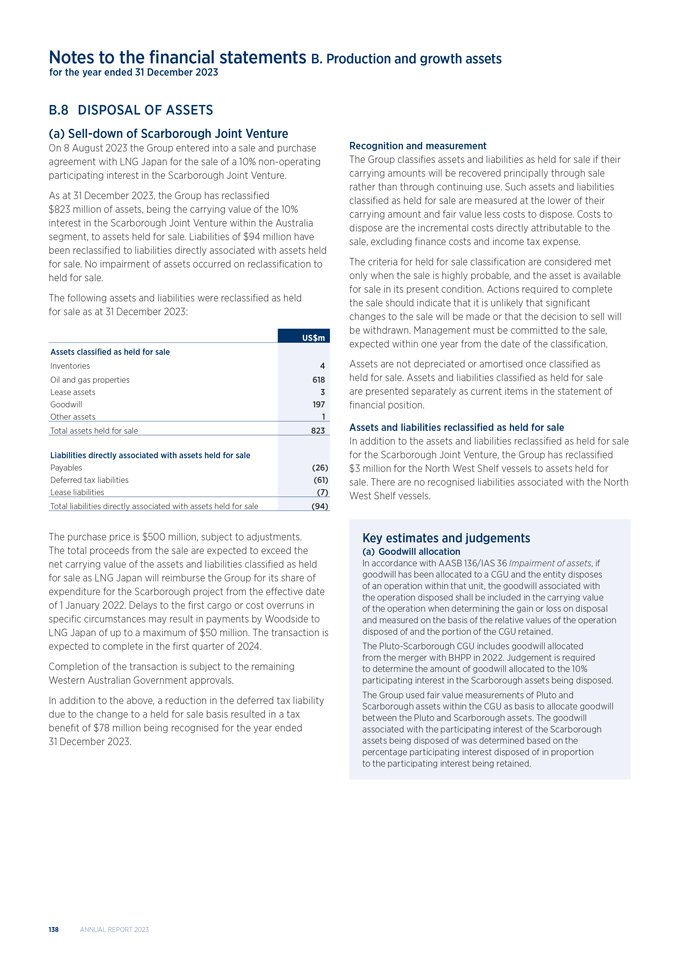

附件99.1

2023年年度合併報告附錄4E

附件99.1

2023年年度合併報告附錄4E

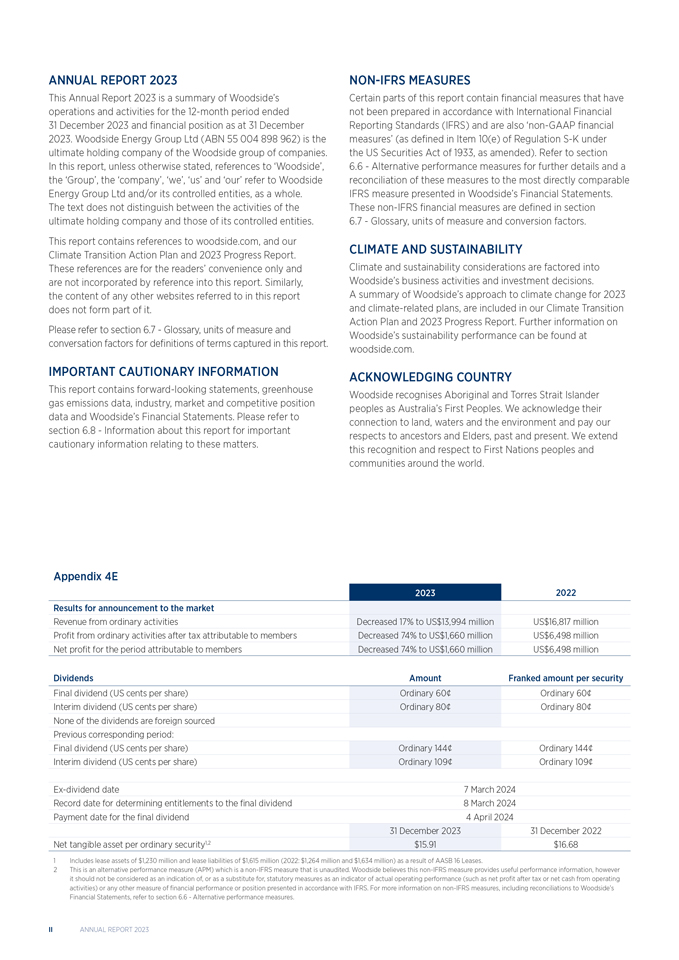

2023年年報這份2023年年報是S在伍德賽德的運營和活動的摘要截至2023年12月31日的12個月期間 和截至2023年12月31日的財務狀況。伍德賽德能源集團有限公司(ABN 55 004 898 962)是伍德賽德集團公司的最終控股公司。在本報告中,除非另有説明,否則提及伍德賽德能源集團有限公司和/或其控制的 實體時,指的是伍德賽德能源集團有限公司和/或其受控實體。案文沒有區分最終控股公司的活動和其受控實體的活動。這份報告引用了伍德賽德網站,以及我們的氣候過渡行動計劃和2023年進展報告。這些參考文獻僅供讀者參考,不作為參考併入本報告。同樣,本報告提及的任何其他網站的內容也不構成報告的一部分。有關本報告中包含的術語的定義,請參閲 第6.7節詞彙、測量單位和對話係數。重要警示信息本報告包含前瞻性陳述、温室氣體排放數據、行業、市場和競爭地位數據以及伍德賽德S財務報表。有關這些事項的重要警示信息,請參閲關於本報告的第6.8節??信息。非國際財務報告準則 措施本報告某些部分包含未根據國際財務報告準則(IFRS)編制的財務措施,也是非公認會計準則財務措施(定義見1933年美國證券法下的S法規第10(E)項)。有關詳細信息,請參閲第6.6節替代業績計量,並將這些計量與伍德賽德S財務報表中列示的最直接可比的國際財務報告準則計量進行核對。這些非《國際財務報告準則》財務計量的定義見第6.7節詞彙、計量單位和換算係數。氣候和可持續發展氣候和可持續發展考慮因素被納入伍德賽德和S的商業活動和投資決策。我們的《氣候轉型行動計劃》和《2023年進展報告》中包含了《S 2023年應對氣候變化的伍德賽德方法》和氣候相關計劃摘要。欲瞭解有關伍德賽德S可持續發展業績的更多信息,請訪問伍德賽德網站。承認鄉村伍德賽德承認原住民和託雷斯海峽島民為澳大利亞S第一民族。我們承認它們與土地、水和環境的聯繫,並向過去和現在的祖先和長老致敬。我們將這一認可和尊重擴展到世界各地的第一批國家、人民和社區。附錄4E 20232022向市場公佈的結果 普通活動收入下降17%,至139.94億美元 普通活動税後利潤168.17億美元 會員應佔税後利潤下降74%,至16.6億美元 該期間可歸因於會員的淨利潤下降74%,至16.6億美元,至64.98億美元 分紅平均每證券末期股息(美元/股) 普通股60,普通股60,中期股息(每股) 普通股80,普通股80,同期: 末期股息(每股美國分) 普通144仙普通144仙中期股息(每股美分) 普通109仙除息日期 7 2024年3月8日末期股息支付日期2024年4月31日2023年12月31日每股普通證券的有形資產淨值1,2 $15.91$16.68 1包括租賃資產12.3億美元和租賃負債16.15億美元(2022年:12.64億美元和16.34億美元) 16租賃。2這是一種替代業績計量(APM),是未經審計的非國際財務報告準則計量。伍德賽德認為,這一非IFRS指標提供了有用的業績信息,但它不應被視為作為實際經營業績指標(如税後淨利潤或經營活動淨現金)的法定指標的指示或替代,也不應被視為根據IFRS提出的任何其他財務業績或狀況指標。有關非《國際財務報告準則》計量的更多信息,包括與伍德賽德·S財務報表的對賬,請參閲《替代業績計量》第6.6節。II 2023年年報

內容1. 概述4 1.1 關於伍德賽德4 1.2 2023摘要5 1.3 主席S報告8 1.4 首席執行官S報告9 1.5 重點領域10 2. 戰略和財務業績12 2.1 伍德賽德S戰略12 2.2 資本管理13 2.3 財務概述16 2.4 能源市場18 2.5 商業模式和價值鏈19 3. 我們的業務20 3.1 澳大利亞運營20 3.2 國際運營22 3.3 營銷和交易23 項目24 3.5 退役26 3.6 勘探和開發27 3.7 新能源和碳解決方案28 3.8 氣候和可持續性29 3.9 風險因素40 3.10 儲量和資源聲明48. 治理52 4.1 公司治理聲明53伍德賽德 的公司治理53董事會 54董事會委員會 62執行領導團隊 65促進負責任和道德的行為 67風險管理和內部控制 69納入和 多樣性 71其他治理披露 74股東 754.2. 董事報告76 4.3 薪酬報告80. 財務報表105 5.1 財務報表105 6. 補充信息 172 6.1 關於石油和天然氣的補充信息未經審計172 6.2 三年財務分析178 6.3 額外披露183 6.4 股東統計195 6.5 資產事實203 6.6 替代 業績衡量207 6.7 詞彙,計量單位和換算係數210 6.8 有關本報告的信息2146.9 十年比較數據摘要第216伍德賽德能源集團有限公司

1.1Woodside 簡介我們是一家全球能源公司,成立於澳大利亞,提供可靠且負擔得起的能源,幫助 人們過上更好的生活。在創新和決心的推動下,我們35年前在澳大利亞建立了液化天然氣(LNG)行業,今天為越來越多的客户提供天然氣。幾十年來,我們一直可靠地向澳大利亞的家庭和企業輸送天然氣,支持當地工業的發展,推動經濟繁榮。自2022年與必和必拓的S石油業務合併後,通過擴大全球投資組合,我們已成為世界上更大的能源供應商。我們正在通過利用我們可靠的運營、強大的客户關係和投資於新能源的過往記錄,為能源轉型做出貢獻。我們的戰略是通過開發低成本、低碳、盈利、彈性和多樣化的投資組合來在這一過渡中蓬勃發展。1我們的液化天然氣尤其可以幫助亞洲主要經濟體的客户滿足其能源安全需求,同時支持他們的脱碳目標。我們 還在投資新的產品和服務,以幫助客户減少或避免排放。我們正在努力減少我們的淨股權範圍1和2温室氣體排放,以實現我們到2050年或更早實現淨零的目標。2我們優質的全球投資組合和強勁的資產負債表使我們能夠今天執行重大項目,同時尋找機會,為伍德賽德S帶來下一波增長。這些機會涉及天然氣、石油、新能源產品和低碳服務。我們在追求增長與注重財務回報和股東價值的紀律嚴明的投資方式之間取得平衡。我們認識到,為了保持強勁的運營和財務業績,我們需要可持續地運營我們的業務。我們繼續關注安全、環境和社會績效,並與社區保持有意義的關係。我們以我們的價值觀為指導,我們相信我們的成功是由我們的員工和文化支撐的。1有關伍德賽德如何使用低碳投資組合的定義,請參閲第6.7節詞彙、測量單位和轉換系數。2個目標和期望是淨權益範圍1和2温室氣體排放量 相對於6.32公噸的起始基數-e代表2016-2020年温室氣體年平均總排放量範圍1和2,可根據生產2或受制裁資產的潛在股本變化進行調整(向上或向下),並在2021年前作出最終投資決定。淨股本排放量包括利用碳信用作為補償。4 2023年年報

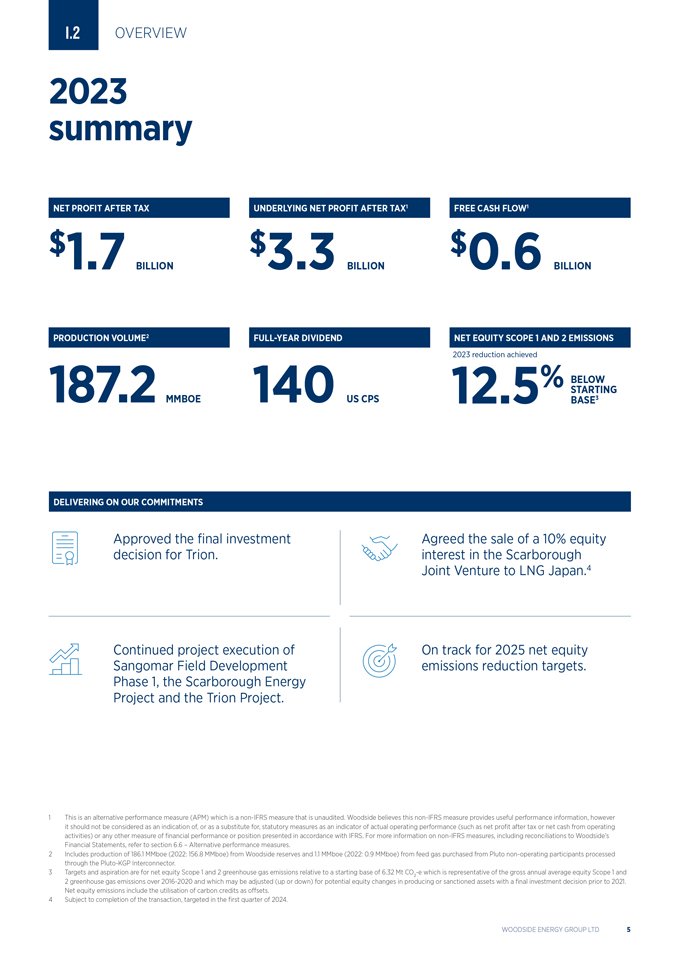

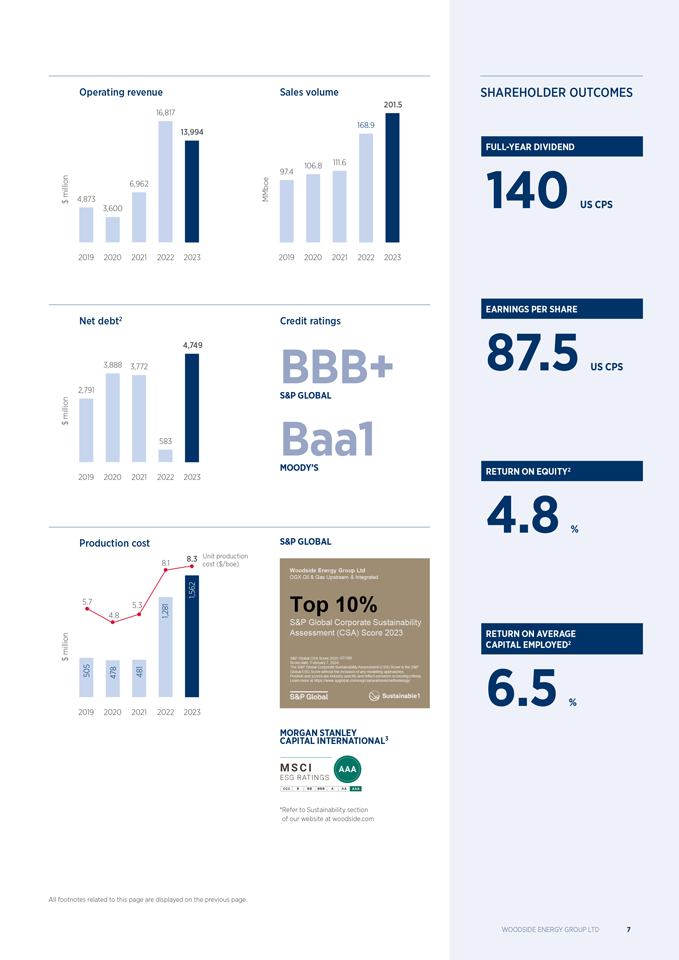

1.2概述2023年概述 税後淨利潤 基本税後淨利潤1自由現金流1$17億 $3.3 BILLIONX%$6億生產量2 全年股息淨股本範圍1和2排放量2023年實現低於187.2 140 12.5%開始MMBOE US CPS BASE 3履行我們的承諾 批准了最終的投資 同意出售 的10%股權決定。 在斯卡伯勒合資企業中的權益出售給日本液化天然氣公司。4繼續執行 的項目,按計劃實現2025年淨股本桑戈馬油田開發 減排目標。第一階段,斯卡伯勒能源 項目和Trion項目。 1這是一種替代績效衡量標準,是一種未經審計的非IFRS計量。Woodside 認為,這種非IFRS衡量標準提供了有用的業績信息,但不應被視為法定衡量標準的指示或替代,作為實際經營業績 (如税後淨利潤或經營活動現金淨額)的指標,也不應被視為根據IFRS呈列的任何其他財務業績或狀況的衡量標準。有關非IFRS 措施的更多信息,包括與Woodside公司財務報表的對賬,請參閲第6.6節“替代績效措施”。2包括從Woodside儲量生產186.1百萬桶當量(2022年:156.8百萬桶當量),以及通過冥王星—KGP互連器處理的從冥王星非運行參與方購買的原料氣生產1.1百萬桶當量(2022年:0.9百萬桶當量)。3目標和期望是相對於632萬噸二氧化碳當量起始基數的淨權益範圍1和2温室氣體排放量,該起始基數代表2016—2020年期間的年平均權益範圍1和2温室氣體排放總量,且可能會 調整(向上或向下)生產2或制裁資產的潛在股權變動,並在2021年前作出最終投資決定。淨權益排放包括使用碳信用額作為抵銷。4待 交易完成後,目標為2024年第一季度。伍德能源集團有限公司5

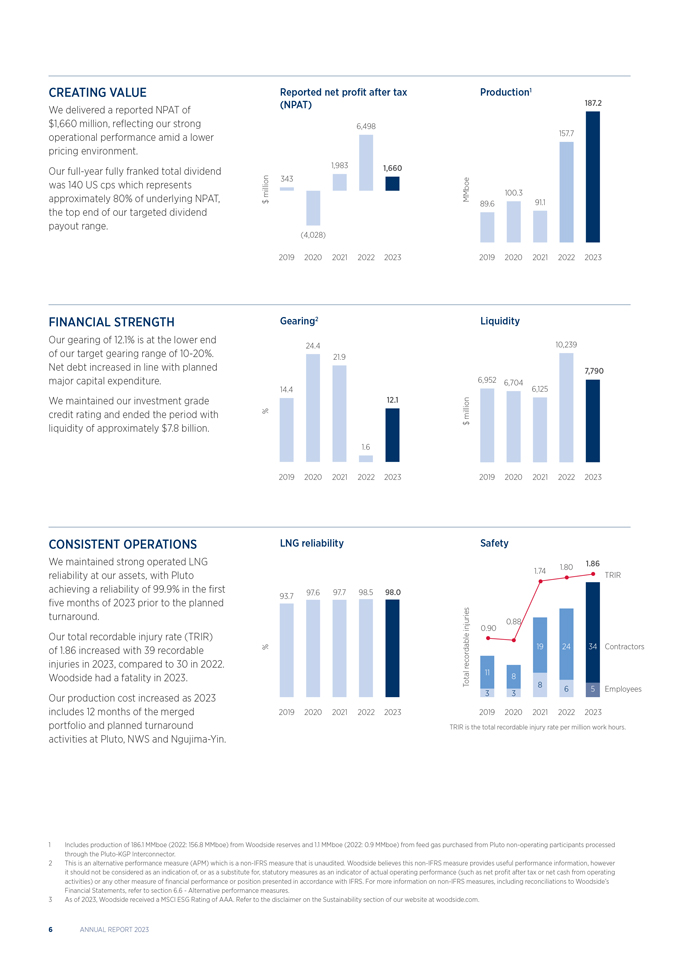

創造價值報告税後淨利潤生產1我們實現了報告的NPAT,(NPAT)187.2 16.6億美元, 反映了我們在157.7美元較低的定價環境下強勁的6498年運營業績。我們全年全額派息總額1,9831,660美元為140美分,佔基礎NPAT的343美元約80%,百萬美元100.3美元89.691.1是我們目標股息支付範圍的高端。(4,028)2019 2020 20212022202320202020212022023財務實力齒輪2流動性我們的12.1%的資產負債率是我們目標資產負債率範圍的下限24.410,239 10—20%。21.9淨債務增加與計劃的7,790項主要資本支出一致。6,9526,704 14.46,125我們維持 投資級別12.1的信用評級,期末流動性約為78億美元。$1.6 2019 20 @ 0 20212022202320192020 202120222023一致操作LNG可靠性安全我們 保持強勁的LNG 1.801.86可靠性在我們的資產,冥王星1.74TRIR在2023年的前五個月裏實現了99.9%的可靠性97.697.798.598.0 93.7,在計劃的週轉之前。0.8 8傷害0.90我們的總可記錄傷害率(TRIR)為1.86,2023年承包商受傷人數增加了39%,相比之下,2022年為30人。可記錄的Woodside在2023年發生了死亡事件。共有118 865名員工 我們的生產成本隨着2023年而增加33包括合併後的12個月2019年2023年02020212022202320192020 202120222023投資組合和計劃週轉TRIR是每百萬工時的總可記錄傷害率。 在 冥王星、NWS和Ngujima—Yin的活動。包括從Woodside儲量生產1.861億桶當量(2022年:156.8億桶當量),以及從冥王星非運行參與方購買的原料氣通過冥王星—KGP互連器處理的1.1億桶當量(2022年:0.9億桶當量)。 這是一種替代績效指標(APM),是未經審計的 非IFRS指標。Woodside認為,這種非IFRS計量提供了有用的業績信息,但不應被視為法定計量的指示或替代,作為實際經營業績指標(如税後淨利潤或經營活動現金淨額)或根據IFRS呈列的任何其他財務業績或狀況的計量。有關非國際財務報告準則措施的更多信息,包括與Woodside公司財務報表的對賬,請參閲第6.6節替代績效措施。截至2023年,Woodside 獲得MSCI ESG評級AAA。請參閲我們網站woodside.com的可持續發展部分的免責聲明。2023年度報告

營業收入銷售額股東業績201.5 16,817 168.9 13,1994年全年股息106.8 111.6 97.4 69.62百萬美元48.73百萬美元140美元CPS 3,600 2019 2020 2021 2022 2023 2019 2020 2021 2022 2023每股盈利淨負債2信貸評級4,749 3,888 3,772BBB +87.5US CPS 2,791標普全球百萬美元583Baa1情緒低落的股票儲備2 2019 2020 2021 2022 2023 4.8%生產成本S & P GLOBAL 8.3單位生產8.1成本(美元/boe)伍德賽德能源集團有限公司OGX石油和天然氣上游和綜合1,562 5.7 5.3頂部 10% 4.8 1,281標普全球企業可持續發展評估(CSA)得分2023年平均百萬資本就業回報2 $標普全球CSA得分2023年:67/100得分日期:2024年2月7日標普全球企業 可持續性評估(CSA)評分是標普全球ESG評分,不包括任何建模方法。 505 478 481職位和分數是行業特定的,反映了排除篩選標準。 欲瞭解更多信息,請訪問 https://www.example.com % 2019 2020 2021 2022 2023摩根斯坦利資本國際3 * 請參閲我們網站www.example.com的可持續發展部分與此頁面相關的所有腳註均顯示在 上一頁。 伍賽德能源集團有限公司7

1.3概述主席的報告在生活成本不斷上升的壓力之際,我們非常自豪能夠為

股東和社區回報價值。可悲的是,我們2023年的表現被我們的同事Michael Jurman 6月在North Rankin Complex的死亡所蒙上了陰影。我們必須提高安全性,並盡我們所能確保每個人誰在伍德賽德的資產和設施上工作,安全返回家園。通過我們擴大的產品組合中的業績創紀錄生產創造價值,進一步確立了Woodside作為全球能源供應商的地位。我們於二零二三年取得強勁的財務表現。

雖然石油和天然氣價格從2022年的創紀錄高位回落,但強勁的產品需求仍在繼續。於2023年,我們錄得年度除税後純利17億元,基礎除税後純利33億元。基於此,

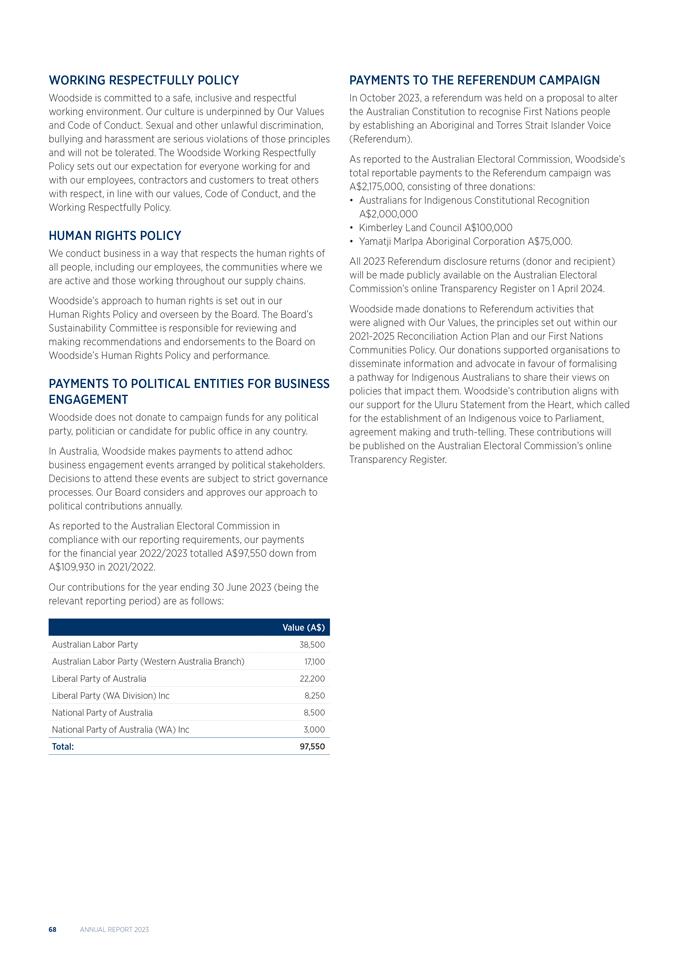

董事會已確定每股60美分的全額派息末期股息,導致全年股息總額為每股140美分。當Woodside表現良好時,我們經營的社區也會受益。2023年,伍德賽德向澳大利亞政府支付了創紀錄的50億澳元的税收和版税。

明確的增長戰略Woodside的戰略是通過構建低成本、低碳、盈利、彈性和多樣化的投資組合,在能源轉型中茁壯成長。1我們在不同商品中提供的長期機會支持了這一點。我們的主要增長項目,包括Sangomar、Scarborough和

Trion,都處於良好的位置,能夠滿足客户的需求。我們強勁的業績和嚴格的資本管理將幫助我們滿足這一需求,並繼續實現增長和回報。支持能源轉型2023年,我與許多投資者進行了交談,他們希望更多地瞭解我們應對氣候變化挑戰的計劃,這是全年董事會會議的一個常規重點。我們還繼續檢討我們的範圍3目標的方法,以迴應投資者的反饋,並決定以新的補充減排目標來補充我們現有的投資目標。我們已經改進了我們的氣候披露,將在我們的2024年年度股東大會上提交諮詢股東投票。 我們將繼續認真聽取投資者的意見,以告知我們的方針,包括我們如何考慮未來的投資。回顧2023年,中東和歐洲的衝突導致全球能源市場又出現了動盪的一年。再加上對能源安全的高度關注,這進一步表明過渡不會是平穩或線性的,我們的戰略需要作出迴應。我們相信,天然氣將繼續在全球能源結構中發揮關鍵作用,包括為可再生能源供電的電網提供後備支持。我們亦正致力於將產品組合多元化至新能源產品及低碳服務。強有力的領導代表董事會,

很高興歡迎Ashok Belani,他一開始, 非執行董事於二零二四年一月二十九日。Ashok在新能源和石油行業脱碳方面擁有豐富的經驗,將成為伍德賽德董事會的寶貴資產。我也要感謝我們的首席執行官Meg O Wanneill和整個Woodside團隊的成功一年。梅格是冷靜,有條不紊和包容。她是抓住能源轉型帶來的機遇

並應對其挑戰的合適領導者。也感謝我們的股東,感謝他們對伍德賽德的投資和信任。2024年,伍德賽德將慶祝其成立70週年,並在澳大利亞液化天然氣產業的發源地西北大陸架生產40週年。這是一個反思伍德賽德為澳大利亞經濟繁榮和區域能源安全所做的重大貢獻的機會。我們計劃在今後幾年裏繼續發揚這一傳統。

Richard Goyder,AO董事會主席2024年2月27日請參閲第6.7節術語表、計量單位和換算係數,瞭解Woodside如何使用術語"低碳組合"的定義。2023年度報告

1.4概述

高級專員的首席執行官報告

在過去的一年裏,伍德賽德創造了創紀錄的生產,同時為未來的增長和價值奠定了基礎。

在與必和必拓石油業務合併後,我們將向更大的全球能源公司過渡,作為一個團隊在多個地點有效地工作。

安全必須改善

當我回想2023年時,我會一直想起我們的同事Michael Jurman,他在我們的North Rankin Complex工作時失去了生命。他的去世繼續影響着我們中的許多人,我再次向邁克爾的家人和朋友表示最深切的哀悼。安全是我們的首要任務,我們

必須改進。2023年,我們委託對我們的安全系統進行外部檢討,這將指引我們改善安全表現的努力。強勁、可靠的生產我們的

擴大了全球產品組合,實現了創紀錄的187.2百萬桶油當量(513百萬桶油當量/天)的全年產量。Pluto LNG和西澳大利亞州Karratha天然氣廠(KGP)的可靠性為98%。主要資產的計劃週轉和維修活動已順利完成。這種強勁的運營性能

使我們能夠充分利用對產品的持續強勁需求。2023年的營業收入為140億美元,推動年度税後淨利潤為17億美元。我們實現了這一創紀錄的產量,同時繼續

減少淨權益範圍1和2排放,2023年的淨權益範圍2和2022年的淨權益排放比我們的起始基數低12. 5%(2022年為11%)。1實現下一波增長年內,我們在主要增長項目上取得了良好進展。截至2023年底,

我們的斯卡伯勒能源項目已完成超過55%,並有望於2026年交付第一批液化天然氣貨物。2年底,冥王星列車2模塊的製造正在進行中,51個模塊中的6個已經完成,現場工程進展順利。關鍵的

環境批准於2023年底獲得通過,隨後我們的地震項目成功完成。我們與液化天然氣日本公司(LNG Japan)就出售斯卡伯勒合資企業10%股權達成的買賣協議是

2023年的關鍵性協議。3 Meg O Neill塞內加爾近海的Sangomar項目於2023年底完成了93%,23口井中有17口已鑽完。4浮式生產儲油卸油(FPSO)設施駛離了

新加坡造船廠12月我們的目標是第一石油, 2024年年中。今年6月,我們對墨西哥灣Trion項目做出了最終投資決定(FID)。

浮式生產裝置(FPU)材料和水下設備的採購活動開始。我們的目標是2028年Trion的第一批石油。在我們的新能源產品組合中,我們在氫燃料堆@H2Perth上使用FID。我們的目標是在2025年向西澳大利亞州

工業和公共客户供應氫氣。我們還在推進多個碳捕獲和封存(CCS)項目。我們在美國俄克拉荷馬州擬議的H2OK氫項目以及在西澳大利亞州Karratha附近擬議的Woodside Solar項目

也正在取得進展。可持續發展績效隨着Woodside公司全球業務的不斷擴大,我們的可持續發展績效變得越來越重要。2023年,我們更新了我們的可持續發展戰略,進一步將可持續發展

績效融入我們所做的一切。最後,我為Woodside團隊感到自豪,併為在這個行業工作感到自豪。我親眼目睹了安全可靠的能源如何改變生活。在我們努力實現一個有利於後代的穩定能源過渡時,我們不能忽視這一點。

梅格·奧尼爾

首席執行官

執行官兼董事總經理

2024年2月27日

1目標和期望

是指相對於632萬噸二氧化碳起始基數而言的淨權益範圍1和2温室氣體排放量 —e代表

2016—2020年期間範圍1和範圍2温室氣體排放量的年平均權益總額,並可根據在2021年之前最終投資決定生產2或批准資產的潛在權益變動進行調整(上調或下調)。淨權益排放包括使用碳信用額作為抵銷。

2完成百分比不包括冥王星1號列車改裝項目。

3

交易完成後,目標為2024年第一季度。

4在此期間後確定的0.2%更正後,項目進度已更新為93%

。

伍德賽德能源集團有限公司9

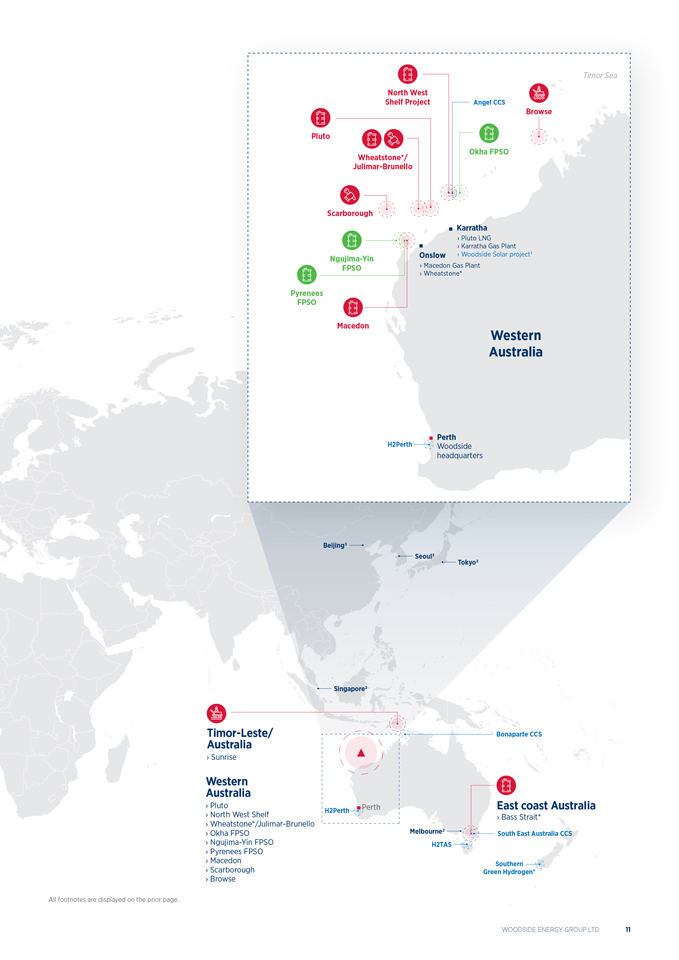

1.5概述

重點領域

休斯敦

神子亞特蘭蒂斯 *

瘋狗 *

墨西哥灣

Trion

加拿大

* *

H2OK Capella *

休斯敦

加勒比

安戈斯圖拉灣

紅寶石墨西哥

神子

亞特蘭蒂斯 *

瘋狗 *

塞內加爾

桑戈馬爾

鑰匙

初級產品階段

天然氣生產資產石油項目新能源

機會開發1或低碳服務1

* 未手術。

1須經FID和/或監管機構批准。請參閲第6.5節"資產事實",

2表示銷售辦事處。

3表示代表和(或)聯絡處。更多關於伍德賽德的利益的細節。

10 2023年度報告

帝汶海

西北大陸架項目Angel CCS

瀏覽Pluto Okha FPSO惠斯通*/Julimar—Brunello Scarborough Karratha Pluto LNG Ngujima—Yin FPSO Macedon Gas Plant

伍德賽德

總部

北京市

首爾

東京都

新加坡

東帝汶/澳大利亞波拿巴CCS

日出

澳大利亞西

冥王星珀斯東海岸澳大利亞

H2珀斯

* 西北大陸架 * 巴斯海峽 *

惠斯通*/Julimar—Brunello

墨爾本

Okha FPSO東南澳大利亞CCS

Ngujima—Yin FPSO H2TAS

Pyrenees FPSO

南馬其頓

Scarborough Green Hydrogen *

瀏覽器

所有腳註均顯示在前一頁。

伍德賽德能源集團有限公司11

2.1戰略和財務業績

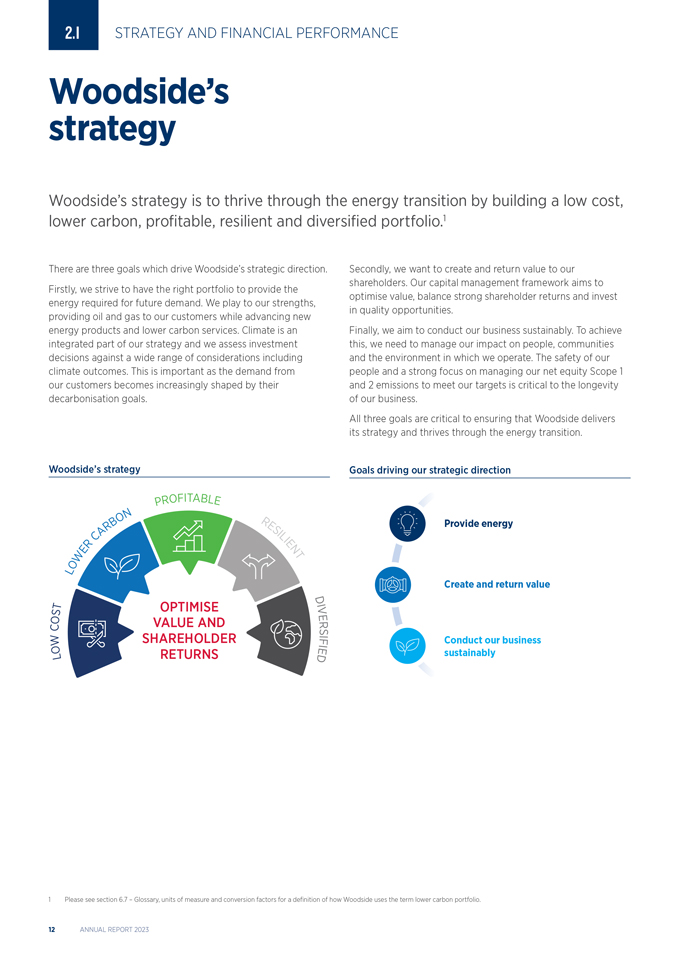

伍德賽德的策略

伍德賽德的戰略是通過構建低成本、低碳、盈利、彈性和多樣化的投資組合,在

能源轉型中茁壯成長。

有三個目標驅動伍德賽德的戰略方向。首先,我們努力擁有合適的產品組合,以提供未來需求所需的能源。我們發揮自身優勢,為客户提供石油和天然氣,同時推進新能源產品和低碳服務。

氣候是我們戰略的一個組成部分,我們根據包括氣候結果在內的廣泛考慮因素評估投資決策。這一點非常重要,因為我們客户的需求越來越受到他們的

脱碳目標的影響。

第二,我們希望為股東創造和回報價值。我們的資本管理框架旨在優化價值、平衡強勁的

股東回報並投資於優質機會。

最後,我們的目標是以可持續的方式開展業務。為了實現這一目標,我們需要管理我們對

人員、社區和我們運營所在環境的影響。我們的員工安全以及專注於管理我們的淨權益範圍1及2排放,以達到我們的目標,對我們的業務長壽至關重要。

這三個目標對於確保伍德賽德實現其戰略並通過能源轉型蓬勃發展至關重要。

伍德賽德的戰略目標推動我們的戰略方向

盈利

N

R B O RES提供能量

的1l

R C I E E NT W L O創建並返回值D T OPTIMISE I S V O VALVE AND E C R

S

W股東F I開展業務O回報E I可持續

L d

1請參見第6.7節術語表、計量單位和換算係數

,瞭解伍德賽德如何使用術語"低碳組合"的定義。

12 2023年度報告

2.2戰略和財務業績

資本

管理

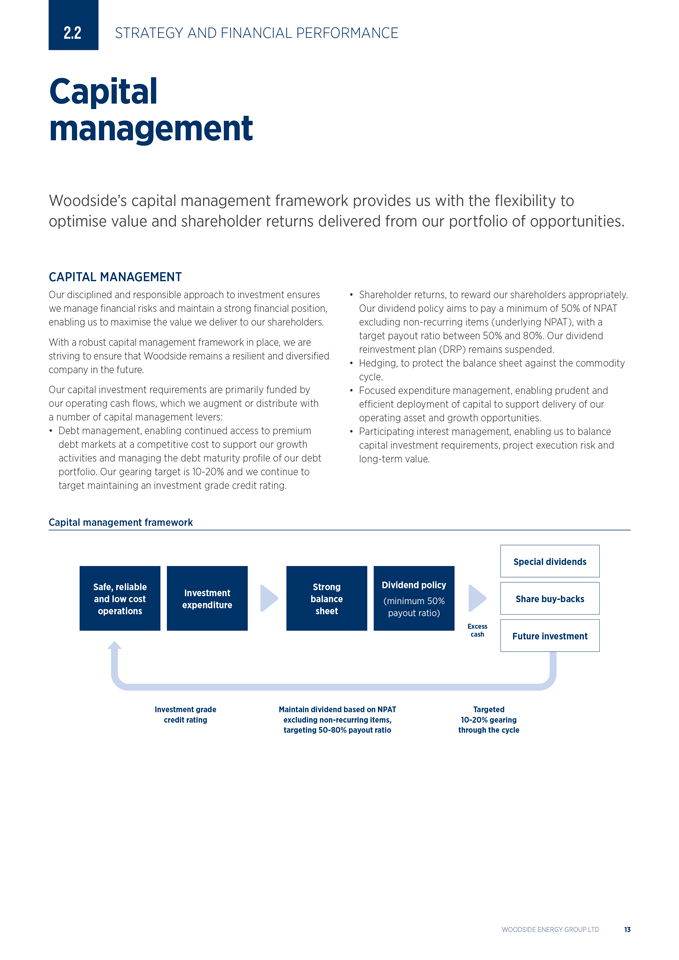

伍德賽德的資本管理框架為我們提供了靈活性,以優化從我們的

機會組合中獲得的價值和股東回報。

資本管理

我們紀律嚴明、

負責的投資方法確保我們管理財務風險並保持穩健的財務狀況,使我們能夠最大限度地提高我們為股東提供的價值。隨着一個強大的資本管理框架到位,我們努力

確保伍德賽德在未來保持一個韌性和多元化的公司。

我們的資本投資需求主要由我們的經營現金流提供資金,我們通過多種資本管理槓桿增加或分配這些現金流:

債務管理,以

具有競爭力的成本持續進入優質債務市場,以支持我們的增長活動,並管理我們債務組合的債務到期情況。我們的傳動目標是 10—20%,我們將繼續保持投資級信用評級

。

股東回報,以適當的回報股東。我們的股息政策旨在支付至少50%的NPAT, 非經常性項目(基礎NPAT),目標支付比率在50%至80%之間。我們的股息再投資計劃(DRP)仍然暫停。

套期保值,以保護資產負債表免受商品週期的影響。

集中的支出

管理,實現謹慎高效的資本部署,以支持我們的運營資產交付和增長機會。

參與式利益

管理,使我們能夠平衡資本投資需求、項目執行風險和長期價值。

資本管理框架

特別股息

安全、可靠的強股息政策投資和低成本餘額

(至少50%的股份 回購支出業務表支出比率)

過剩

現金未來投資

投資等級根據NPAT目標信用評級維持股息

不包括 非經常性項目,10—20%的資產負債率,目標是整個週期的50—80%的派息率

伍德賽德能源集團有限公司13

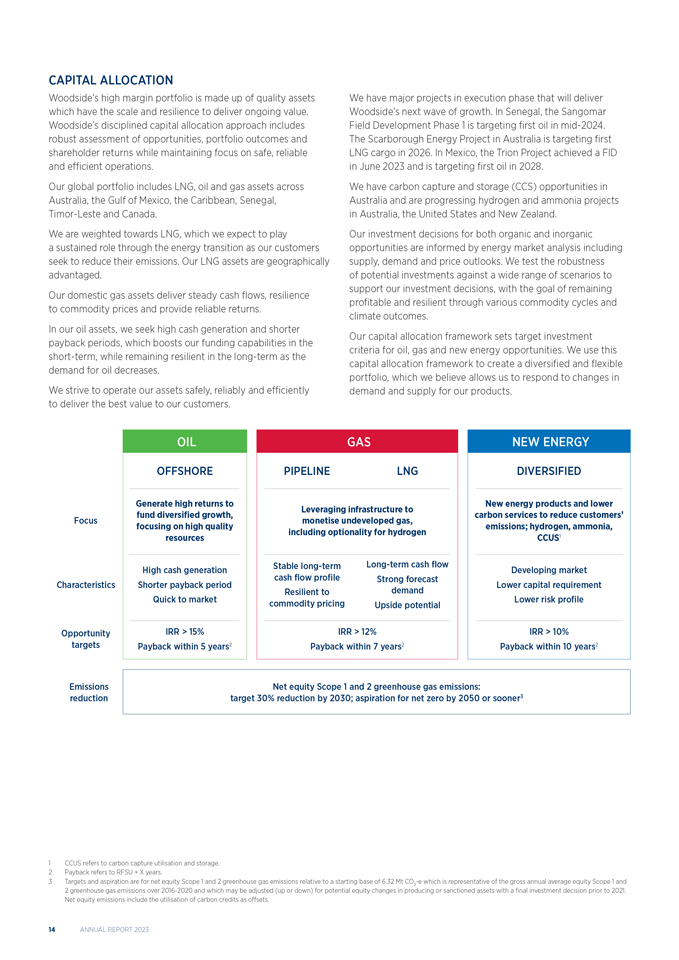

資本配置

伍德賽德的高利潤

投資組合由優質資產組成,這些資產具有規模和彈性,可以提供持續價值。Woodside公司嚴格的資本分配方法包括對機會、投資組合結果和股東回報的穩健評估

,同時保持對安全、可靠和高效運營的關注。

我們的全球投資組合包括澳大利亞、墨西哥灣、加勒比海、塞內加爾、東帝汶和加拿大的液化天然氣、石油和天然氣資產。

我們傾向於液化天然氣,我們希望液化天然氣在能源轉型中發揮持續作用,因為我們的客户

尋求減少排放。我們的液化天然氣資產在地理上是不合理的。

我們的國內天然氣資產提供穩定的現金流、對大宗商品價格的彈性,並提供可靠的回報。

在我們的石油資產方面,我們尋求高現金產生和更短的投資回收期,這在短期內提高了我們的融資能力,

同時在石油需求減少的情況下,保持長期的彈性。

我們致力於安全、可靠和高效地運營我們的資產,為客户提供最佳

價值。

我們有重大項目在執行階段,將提供伍德賽德的下一波增長。在塞內加爾,Sangomar油田開發

第一階段的目標是, 2024年年中。澳大利亞斯卡伯勒能源項目的目標是2026年第一批LNG貨物。在墨西哥,Trion項目於2023年6月實現了FID,目標是2028年的第一批石油

。

我們在澳大利亞擁有碳捕集和封存(CCS)機會,並正在澳大利亞、美國和

新西蘭推進氫和氨項目。

我們對有機和無機投資機會的投資決策均基於能源市場分析,包括供應、需求和價格前景

。我們根據各種情景測試潛在投資的穩健性,以支持我們的投資決策,目標是在各種商品週期和氣候結果中保持盈利和彈性。

我們的資本分配框架為石油、天然氣和新能源機會設定了目標投資標準。我們利用這一資本配置框架來創建一個多樣化和

靈活的投資組合,我們相信這使我們能夠應對產品需求和供應的變化。

油氣新能源

海上管道多樣化

為新能源產品創造高回報,

更低

利用基礎設施,

基金多元化增長,碳

服務減少客户成本

專注於將未開發的天然氣貨幣化,

專注於高質量的排放;氫,氨,

包括

氫的可選性

資源CCUS1

高現金生成

穩定長期長期現金流發展中市場

現金流概況強勁預測

投資回收期較短,資本要求較低

適應需求

快速上市商品定價上行潛力較低風險概況

機會IRR> 15% IRR> 12% IRR> 10%

目標5年內回收

2年內回收7年內回收10年內回收2

範圍1及2温室氣體排放:

到2030年減少30%;到2050年或更快實現淨零排放的目標3

1 CCUS是指碳捕獲利用和儲存。

2回收期指RFSU + X年。

3目標和願望是淨權益範圍1和範圍2温室氣體排放量相對於632萬噸二氧化碳的起始基數 —e,

代表2016—2020年期間範圍1和2温室氣體排放量的年平均權益總額,並可根據在

2021年之前作出最終投資決定的生產2或批准資產的潛在權益變動進行調整(上調或下調)。淨權益排放包括使用碳信用額作為抵銷。

14 2023年度報告

在評估機會時,我們考慮了與

機會相關的廣泛的投資組合評估和機會評估因素。這些評估可以適用於收購或剝離,以及評估新項目對投資組合的影響。

產品組合評估

推薦1機會評估推薦1

收益免費現金基金排放策略回報

IRR/NPV風險盈虧平衡

每股 流量配置文件週期

使用價格、情景和環境分析,根據投資組合指標篩選增長機會

可持續性

我們的可持續發展戰略支持我們的公司戰略和宗旨,並將重點放在與我們當前業務活動最相關的可持續發展主題上。我們運用可持續發展的思維來指導企業各個層面的決策。我們的可持續發展戰略旨在將環境、社會和治理績效融入我們所做的每一件事。

如第3.8節《氣候與可持續發展》中進一步描述的,2023年,我們的可持續發展活動和披露繼續發展,以迴應可持續發展主題、新出現的強制性可持續發展標準和投資者優先事項的戰略重要性。

1説明這些考慮因素。不是一份詳盡的清單。

伍德賽德能源集團有限公司15

2.3戰略和財務業績

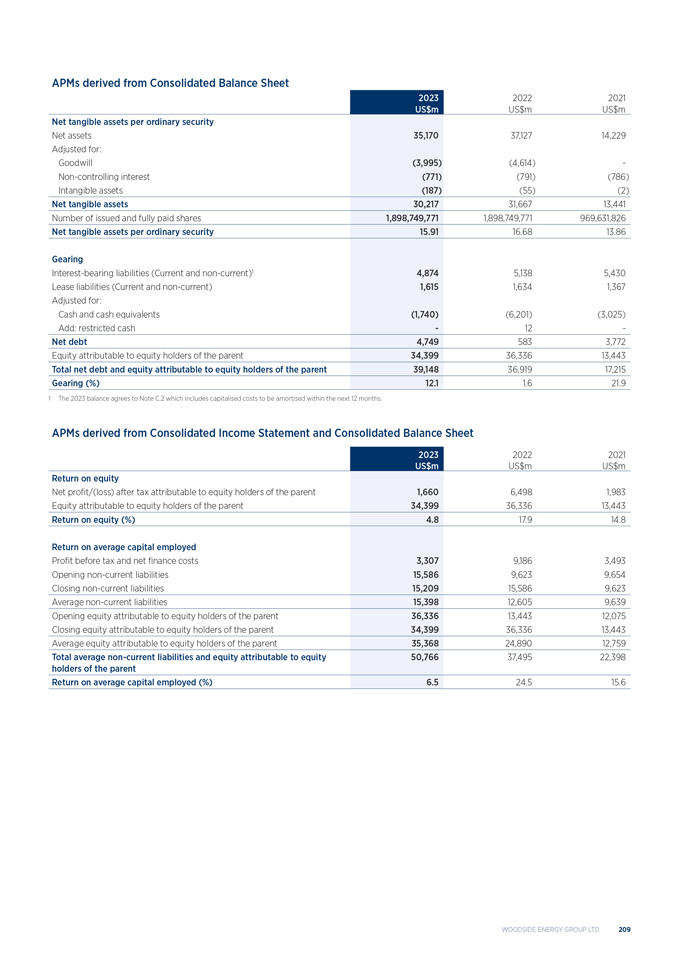

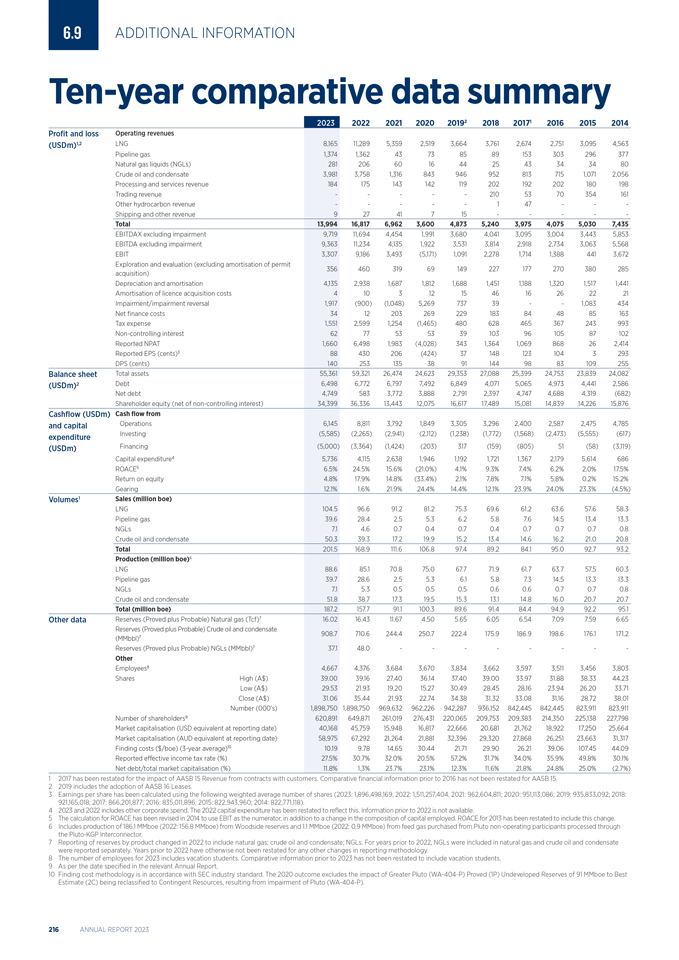

財務

概述

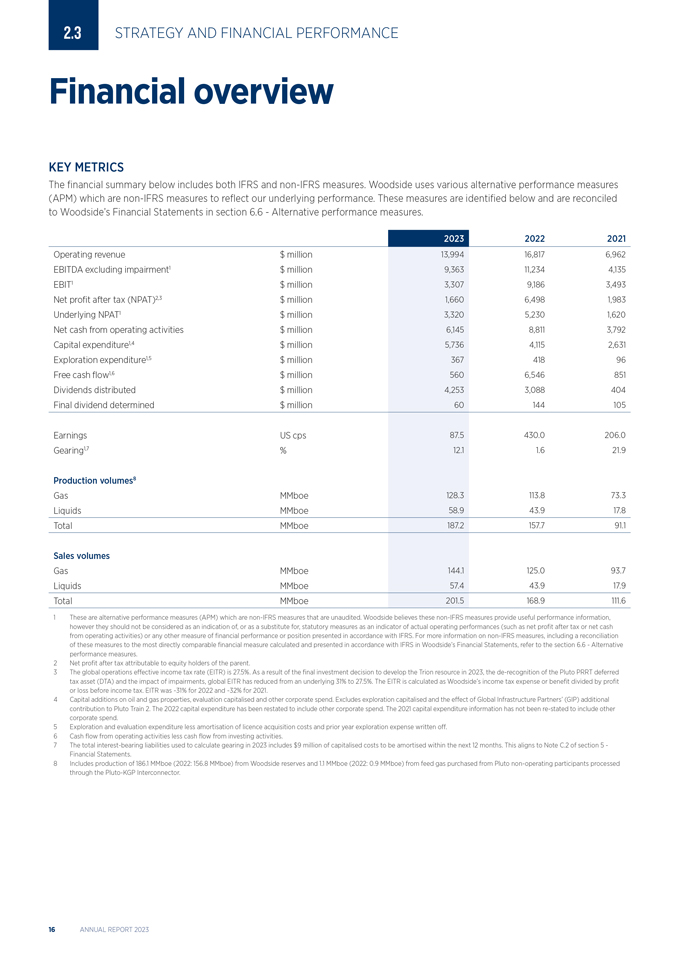

關鍵指標

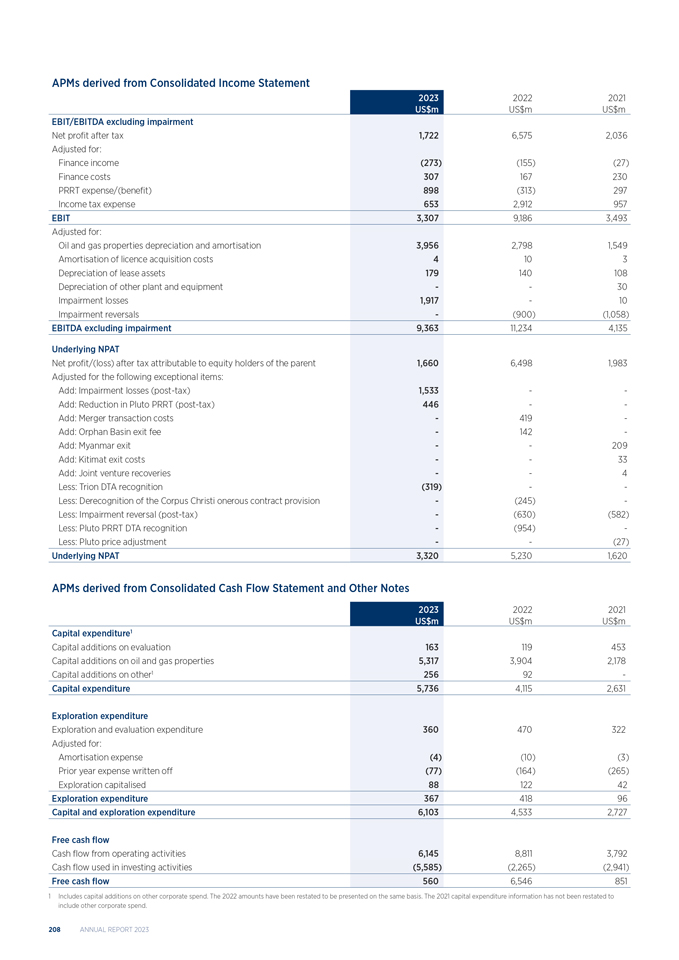

以下財務摘要包括《國際財務報告準則》和非國際財務報告準則計量。伍德賽德使用各種非國際財務報告準則的替代業績衡量標準(APM)來反映我們的基本業績。這些衡量標準如下所示,並與伍德賽德S財務報表第6.6節中的替代績效衡量標準進行了核對。

2023

2022 2021

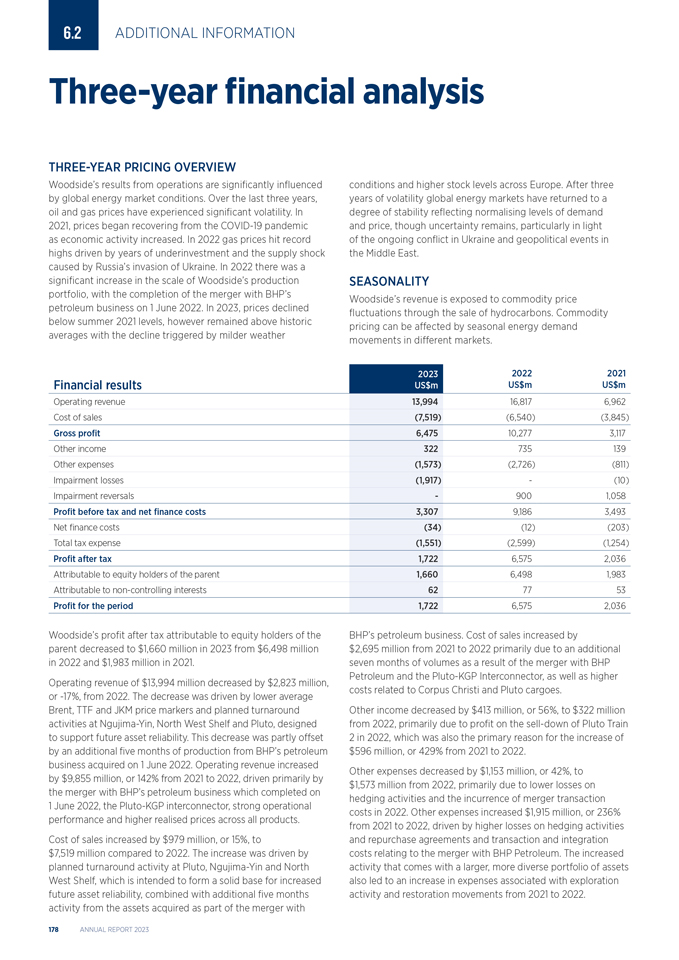

營業收入 $13,994 16,817 6,962

不包括減值的EBITDA(1) $9,363 11,234 4,135

息税前利潤(1) 百萬美元3,307 9,186 3,493

税後淨利潤(2,3) $1,660 6,498 1,983

基本淨利潤(1) 百萬美元3,320 5,230 1,620

經營活動淨現金 $6,145 8,811 3,792

資本支出(1,4) 百萬美元5,736 4,115 2,631

勘探支出(1,5) 百萬美元

367 418 96

自由現金流(1,6) 560 6,546 851

分派之股息 百萬美元4,253 3,088 404

最終

股息已確定 百萬美元60 144 105

盈利 美國cps 87.5 430.0 206.0

傳動裝置(1,7) % 12.1 1.6

生產量(8)

氣體 MMboe 128.3 113.8 73.3

液體 MMboe 58.9 43.9 17.8

總 MMboe 187.2 157.7 91.1

銷售

卷

氣體 MMboe 144.1 125.0 93.7

液體 MMboe 57.4 43.9 17.9

總 MMboe 201.5 168.9 111.6

1這些是替代績效指標(APM), 未經審計的非IFRS計量。Woodside認為,這些非IFRS指標提供了有用的業績

信息,但它們不應被視為法定指標的指示或替代,作為實際經營業績指標(如税後淨利潤或經營活動現金淨額)或任何其他

財務業績或根據IFRS呈列的狀況的指標。有關非IFRS計量的更多信息,包括這些計量與根據IFRS計算和列報的最直接可比財務計量的對賬,請參閲第6.6節替代績效計量。

2歸屬於母公司股權持有人的税後淨利潤。

3全球業務實際所得税率(EITR)為27.5%。由於最終

投資決定在2023年開發Trion資源, 由於取消確認冥王星PRRT遞延税項資產(DTA)和減值的影響,全球EITR已從基礎31%降至27.5%。

EITR的計算方法是Woodside的所得税費用或收益除以所得税前損益。二零二二年的EITR約為31%,二零二一年約為32%。

4石油及天然氣物業的資本增加、資本化評估及其他企業開支。不包括資本化勘探以及全球基礎設施合作伙伴基金(GIP)對冥王星列車2號額外捐款的影響。2022年資本

支出已重列,以包括其他企業支出。2021年資本開支資料尚未 重列以包括其他公司支出。

5勘探及評估開支減特許權購置成本攤銷及過往年度勘探開支撇銷。

6經營活動現金流量減去投資活動現金流量。

7用於計算2023年資產負債的

計息負債總額包括將於未來12個月內攤銷的900萬美元資本化成本。這與第5節財務報表附註C.2一致。

8包括從Woodside儲量生產的1.86億桶當量(2022年:156億桶當量)和從Pluto購買的原料氣生產的1.1億桶當量(2022年:0.9億桶當量)

通過冥王星—KGP互連器處理的非操作參與者。

16 2023年度報告

資本管理

末期股息和股息

再投資計劃

已確定2023年全額蓋印末期股息60美分。末期股息派付總額為11. 39億元,

佔二零二三年下半年相關NPAT約80%。1股息再投資計劃(DRP)仍暫停。

流動性和償債

伍德賽德銀行的主要流動性來源是現金和現金等價物、經營活動產生的淨現金、雙邊貸款和銀團貸款項下的未使用借貸能力、發行債務或股權證券以及其他來源,如出售 非戰略性資產。

在這一年中,伍德賽德從經營活動中產生了61.45億美元的現金流,並提供了5.60億美元的正自由現金流。2,3伍德賽德將其備用債務額度從40.5億美元增加到60.5億美元,並償還了2.84億美元的到期債務。期末,提取債務為48.74億美元,2024年無償還本金債務,流動性為77.90億美元。

有關Woodside的信貸融資的其他詳情,包括於2023年12月31日的總承擔、到期日和利息以及未償還金額,可參見Woodside於2023年及2022年12月31日的經審核財務報表附註C. 2。

伍德賽德的主要持續使用現金是滿足營運資金要求,為債務義務提供資金,併為伍德賽德的資本支出和收購提供資金。我們

相信流動資金足以滿足我們目前的需求。伍德賽德公司2024年的資本支出預計在50億美元至55億美元之間,主要是由於Sangomar、Scarborough和Trion項目

的支出。這不包括任何其後出售資產、收購或其他權益變動的影響。我們的目標是第一石油, Sangomar將於2024年中期交付,Scarborough將於2026年交付第一批液化天然氣貨物,Trion將於2028年交付第一批石油。

伍德賽德沒有 資產負債表外安排,或有可能

,當前或未來對伍德賽德銀行的財務狀況,收入或支出,經營結果,流動性,資本支出或資本資源有重大影響。

資產負債表

伍德賽德公司對投資級信用評級的承諾保持

不變,並支持伍德賽德公司根據我們的資本配置框架為股東提供可持續回報和投資於未來增長機會的目標。於2023年,伍德賽德的信貸評級分別為BBB+及Baa1。4伍德賽德的負債率於2023年底為12. 1%,處於我們目標範圍的低端, 10—20%。伍德賽德公司的資產負債率

有時可能會超出10—20%的目標範圍,因為資產負債表是在整個投資週期中進行管理的。5

商品

價格風險管理

伍德賽德對衝以保護資產負債表免受大宗商品價格下行風險,特別是在高資本支出時期。

伍德賽德對衝了大約22023年卷的2200萬桶。該等油價對衝的變現價值為 税前支出

約為2億美元。

截至2023年12月31日,Woodside已以每桶約76美元的平均價格對2900萬桶油當量的2024年產量進行了油價對衝。

Woodside還對Corpus Christi液化天然氣量進行了對衝,以防範下行定價風險。這些對衝是

Henry Hub和所有權轉讓設施(TTF)商品互換。平均63%的二零二四年成交量及17%的二零二五年成交量因對衝活動而降低定價風險。

1.《反腐敗條約》是一個 非IFRS措施。請參閲第6.6節"替代績效措施",以瞭解這些措施

與Woodside公司的財務報表的對賬。2自由現金流量是一種非IFRS計量。請參閲第6.6節—替代績效措施,以瞭解這些

措施與Woodside公司財務報表的對賬。3經營活動現金流量減去投資活動現金流量。4信貸評級是對信貸風險的前瞻性意見。標普全球評級和穆迪評級

表示每個機構對伍德賽德按時全額履行其財務義務的能力和意願的意見。信用評級不是購買、出售或持有證券的建議,評級機構可能隨時暫停、降低

或撤銷評級。任何評級應獨立於任何其他信息進行評估。5資本負債率和淨債務為非IFRS計量。請參閲第

第6.6節"替代績效指標",以瞭解這些指標與Woodside公司財務報表的對賬。伍德賽德能源集團有限公司17

2.4戰略和財務業績

能源

市場

2023年,地緣政治事件繼續擾亂能源市場,加強了為客户提供可靠、負擔得起的

和安全能源的重要性。

最近的事件,包括歐洲的能源安全局勢和中東的衝突,為能源轉型帶來了積極和消極的驅動力。對石油和天然氣的需求增加突出表明了繼續生產和投資碳氫化合物的必要性,而對可再生能源和低碳服務的政策支持繼續

。

宏觀經濟

2023年,全球經濟表現強勁,儘管面臨通脹水平持續高企和利率上升的雙重挑戰;國內生產總值(GDP)增長3.0%。1自2022年起採取鷹派貨幣政策,遏制通脹。許多發達經濟體正在越過利率峯值

;然而,政策的長期宏觀經濟影響尚不清楚。

隨着經濟在不温不火的需求、較低的信心

以及房地產行業面臨流動性問題的情況下掙扎,中國呈現出不確定性。然而,最近的政府刺激措施對未來增長是一個積極的跡象,使中國能夠實現2023年GDP增長約5%的官方目標。

到2050年,世界人口預計將增加約20億人,國內生產總值預計將幾乎翻一番,從而推動能源需求的增加。

油

OPEC+繼續在平衡石油市場方面施加控制,並承諾在2024年

進一步減產。3然而, 非歐佩克的產量,特別是美國48個國家,加拿大,巴西和圭亞那將繼續增長到2024年,這可能抵消歐佩克+減產的影響。

2023年,布倫特原油的平均價格為83美元/桶,比2022年的平均價格低18%,比能源危機導致的2022年平均價格高出14%受地緣政治風險溢價、歐佩克+生產管理和非歐佩克產量增速放緩的支撐,油價預計在2024年之前仍將居高不下。

液化天然氣

2023年,全球天然氣市場開始重新平衡,但仍然緊張,俄羅斯液化天然氣制裁的不確定性加劇了這一趨勢。儘管東北亞液化天然氣價格平均為2022年平均價格的一半,為14美元/MMBtu,但全球天然氣價格仍然強勁,符合長期預期。4 Wood Mackenzie在其基本情景預測中預測,在歐洲(到2029年)、中國和新興亞洲市場的增長的支持下,到2033年,全球液化天然氣需求將增長53%.5

新能源產品

在全球範圍內,在政府激勵措施的推動下,對新能源技術的投資有所增加,如REPowerEU和美國通脹削減法案,以及減少長期排放的共同目標。補貼推動了風能和太陽能的早期增長,隨後是技術的改進和大規模製造,這提高了人們的承受能力。儘管新能源產品的環境仍然受到技術證明方面的不確定性、產品未來需求的保障、激勵措施應用的不明確性以及不利的項目經濟效益的挑戰,但伍德賽德相信,新能源產品將在能源轉型中發揮重要作用。

澳大利亞國內天然氣市場

澳大利亞國內天然氣市場在2023年經歷了供不應求的供應短缺。在西澳大利亞州,燃煤發電的逐步淘汰、多次停電和項目延誤支撐了需求。預計到2029年,需求將超過供應高達11%,隨着煤炭供應的淘汰,供應缺口將擴大到2032年。6儘管聯邦政府在2023年對新供應實施了12澳元/GJ的價格上限,以提高人們的承受能力,但未來仍需要在供應和基礎設施方面進行進一步投資,以確保能夠滿足需求。

國際貨幣基金組織,2024年1月。《世界經濟展望》更新。

伍德·麥肯齊,2023年9月。《2023年能源轉型展望》。

《歐佩克石油市場月報》,2024年1月。

湯森路透Eikon。

伍德·麥肯齊,2023年10月。·全球天然氣投資地平線展望。

澳大利亞能源市場運營商,2023年。西澳大利亞州天然氣公司的機會聲明。

2023年年報

2.5戰略和財務業績

業務

和價值模型鏈

伍德賽德的S商業模式尋求通過優先考慮競爭性增長機會、利用我們的運營、開發和技術能力以及投資於客户關係來優化整個價值鏈的回報。

2023個例子

收購、剝離、探索和開發

我們通過收購、

剝離和勘探來管理我們的投資組合,基於

採用嚴格的方法優化股東價值並適當管理風險。2023年6月,參加FID參與Trion

項目。

我們在世界一流的資產和盆地中尋找與我們

能力和現有組合。我們專注於價值,並希望產生低成本,實現了10%的股權出售

低碳發展機遇。在開發階段,我們的目標是優化斯卡伯勒合資企業。1

通過選擇最佳的概念來提取、處理和輸送能量,從而實現價值,

受到廣大客户一致

項目執行

我們以數十年的項目執行專業知識為基礎,投資機遇

在全球範圍內伍德賽德正在受益於其項目的範圍和規模的擴大,現場開發第一階段,斯卡伯勒,

通過跨項目的知識共享以及我們與供應商和Trion的關係來實現產品組合。

承建商我們設計和執行項目時注重安全、成本和可持續性。

操作

我們的運營將安全放在首位,同時注重強大的可靠性和

環保

在偏遠和富有挑戰性的地方。在澳大利亞,我們運營的資產包括Pluto LNG的可靠性達到98%,

西北大陸架(NWS)項目和冥王星液化天然氣項目。我們還在神梓運營Macedon和三艘FPSO KGP,可靠性超過97%。

設施, 巴斯海峽和惠斯通的非經營性權益在國際上,準備

2024年Sangomar上的第一次石油。

我們經營墨西哥灣的Shenzi和特立尼達和多巴哥的Angostura和Ruby,

有在亞特蘭蒂斯和墨西哥灣Mad Dog的非運營權益。我們努力做到

採用技術和持續改進的思維來支持運營性能

並優化我們資產的價值。

市場

我們與客户的關係一直通過可靠的 的跟蹤記錄來維護

自1989年新創建項目以來,S向日本交付了第一批液化天然氣貨物。We Are 簽署了買賣協議(SPA)

通過擴大我們的全球供應業務,在我們的產品組合中建立規模和靈活性, 與墨西哥太平洋有限公司將購買

通過我們與第三方簽訂的液化數量和承購協議。這將在20年內創造出 1.3Mtpa的液化天然氣

優化我們的液化天然氣運輸並抓住短期貿易機會的機會。 薩瓜羅能源液化天然氣項目2

我們將繼續尋找與客户就低碳 開展合作的機會

能源解決方案。

Dismit 已成功完成移除

從開發 Nganhurra立管轉塔繫泊的最早階段開始,退役就被納入項目規劃。

直到田野生活的盡頭。我們與全球承包商合作,安全地拆除恩菲爾德堵塞和廢棄(P&A)設施。

並封堵和廢棄我們不再需要的油井。我們繼續與 合作,所有18口井都在繼續

監管機構兑現我們的退役承諾。 永久堵塞和18個聖誕節中的16個

樹木被移走了。

待交易完成後,預計於2024年第一季度完成。

SPA受墨西哥太平洋公司在Saguaro Energia LNG項目擬議的第三列列車上使用FID的限制。FID預計將於2024年下半年投入使用,商業運營計劃於2029年開始。

伍德賽德能源集團有限公司19

3.1我們的業務

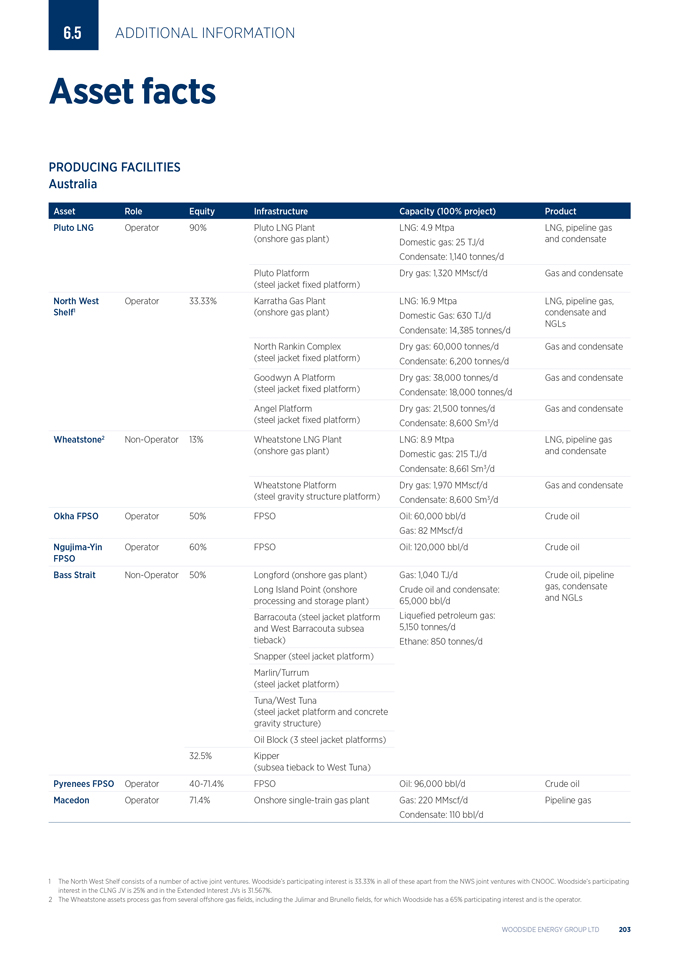

澳大利亞業務

伍德賽德S澳大利亞投資組合由運營型和澳大利亞各地的非運營油氣項目。2023年,伍德賽德·S在澳大利亞業務生產中的份額為145.1 Mboe,與2022.1相比增長了6%

冥王星液化天然氣

Pluto LNG是西澳大利亞州皮爾巴拉地區的天然氣加工設施,由一個海上平臺和一列陸上LNG加工列車組成。

2023年,伍德賽德S在冥王星生產中的份額為51.8Mboe,與2022年相比下降了1%,這是由於計劃的週轉活動部分被2023.1年持續高達98.2%的可靠性所抵消。2023年上半年,伍德賽德成功地完成了陸上和海上設施的主要週轉,執行了必要的維護範圍,以支持持續安全、可靠和高效的生產。

主要的週轉包括安裝了額外的潛力的對接點碳轉化為產品價值流和從擬議的伍德賽德太陽能項目進口太陽能的可能性。

布魯託LNG發生了一起一級安全殼工藝安全事故。

此次事故沒有造成人員傷亡,現已展開調查,找出了事故原因和糾正措施。

西澳大利亞州珀斯的冥王星遠程操作中心於2023年6月全面投入運營,日常工作冥王星液化天然氣的運營現在由總部設在珀斯的團隊遠程承擔。

伍德賽德是運營商,持有90%的參股權益。

伍德賽德太陽能機遇

伍德賽德正在通過利用擬議的伍德賽德太陽能項目的太陽能,

減少冥王星液化天然氣1級温室氣體總排放量的潛在機會。該項目計劃從位於西澳大利亞州卡拉塔西南約15公里處的一個大型太陽能光伏發電場產生約50兆瓦的初始電力,並將輔之以電池儲能系統。2023年,伍德賽德獲得了擬議中的太陽能設施和相關基礎設施的規劃批准以及州和聯邦環境批准。

2023年12月,伍德賽德簽訂了一項有條件的協議,根據該協議,第三方將開發擬議的太陽能設施,並從該設施向伍德賽德供應可再生能源。伍德賽德繼續推進商業協議,包括輸電協議,以支持擬議的項目。

包括從冥王星購買的原料氣生產1.1Mboe(2022年:0.9Mboe)通過冥王星—KGP互連器處理的非操作參與者。

2023年年報

西北陸架項目

NWS項目由三個海上平臺和陸上KGP組成,陸上KGP包括五個陸上液化天然氣加工列車。2023年,伍德賽德·S在新創建項目生產中的份額為40.8Mboe。這與2022年相比增長了11%,原因是

在2022年6月完成與必和必拓的合併後,伍德賽德和S的股權份額增加。2023年,11.2百萬噸冥王星氣體在KGP通過冥王星-KGP互連。互聯器使冥王星液化天然氣能夠被輸送到KGP進行處理。2023年6月,北蘭金建築羣發生了一起死亡事件。我們的同事,一名承包商員工的悲劇性損失,導致根據對該事件的初步調查洞察,實施了額外的運營控制。對這起事件的外部調查正在進行中。由於天然氣田減少和第三方天然氣加工需求有限,預計KGP在2024年的空置量將增加

。為了優化陸上基礎設施的利用,NWS正計劃在2024年讓一列液化天然氣列車下線。新創建與其他

資源擁有者繼續就第三方天然氣的加工進行討論,新創建繼續推進利用KGP的充填和近場機會的開發。NWS項目於2023年開始以低速率處理Waitsia天然氣,並將在Waitsia第二階段設施上線後開始大規模處理,預計將於2024年上線。國家和聯邦監管機構繼續審批西北陸架項目擴建項目,該項目支持KGP未來第三方天然氣資源的長期運營和加工。2023年下半年,伍德賽德成功完成了北蘭金綜合體、Goodwyn平臺和KGP的計劃週轉和維護活動。伍德賽德是運營商,持有33.33%的參股權益。惠斯通和Julimar-Brunello Wheatstone是西澳大利亞州昂斯洛附近的液化天然氣加工設施,包括一個海上生產平臺和兩個陸上液化天然氣加工列車。它處理幾個海上氣田的天然氣,包括Julimar和Brunello。2023年,伍德賽德·S在惠斯通生產中的份額為13.5百萬桶,高於2022年的12.2百萬桶,這是受到重大設施扭虧為盈的影響。Julimar-Brunello第三階段的FID於2023年4月獲得批准。該項目涉及鑽探從Julimar油田與現有Julimar油田生產系統捆綁在一起的多達四口開發井。伍德賽德是運營商,持有Julimar-Brunello油田65%的股份。伍德賽德持有惠斯通項目13%的非運營權益。

巴斯海峽

巴斯海峽位於澳大利亞東南部,通過海上平臺、管道和陸上加工設施網絡生產石油和天然氣。巴斯海峽的資產包括吉普斯蘭盆地合資企業(GBJV)和Kipper單位合資企業(KUJV)。2023年,伍德賽德·S在巴斯海峽的天然氣產量中所佔份額為22.8百萬桶,原因是澳大利亞東海岸天然氣市場需求下降,原因包括冬季變暖。S所生產的伍德賽德天然氣全部供應給澳大利亞東部的國內天然氣市場,支持了澳大利亞對S的能源需求。隨着生產率下降,天然氣資產精簡項目在優化設施方面取得了進展

。該項目將支持實施以天然氣為重點的業務。Kipper壓縮項目已取得進展,預計將在2024年繼續向國內市場供應天然氣。伍德賽德持有50%的股份在GBJV的營業外權益和在KUJV的32.5%的營業外權益。

澳大利亞其他石油和天然氣資產

伍德賽德在西澳大利亞州西北海岸運營着三個浮式生產儲油輪設施。這些是Ngujima-Yen FPSO(Woodside權益:60%)、Okha FPSO(Woodside權益:50%)和比利牛斯FPSO(Woodside權益:40%娃-43-L和71.4%的哇-42-L)。伍德賽德·S在浮式生產儲油船資產中的產量份額為8.0百萬桶,低於2022年的10.6百萬桶,主要是由於計劃進行五年一次的Ngujima-Yen FPSO維護週轉。在新加坡執行的Ngujima-Yen FPSO週轉於2023年6月安全完成

。比利牛斯山的翻身計劃在2024年上半年進行。馬其頓(Woodside權益:71.4%)也由Woodside運營,是一個位於西澳大利亞州昂斯洛附近的天然氣項目,為西澳大利亞州的國內天然氣市場生產管道天然氣。2023年,伍德賽德·S在馬其頓生產的股票份額為8.2Mboe。2023年,馬其頓工廠供應的天然氣約佔西澳大利亞州國內天然氣市場供應量的17%。伍德賽德能源集團有限公司

3.2我們的業務

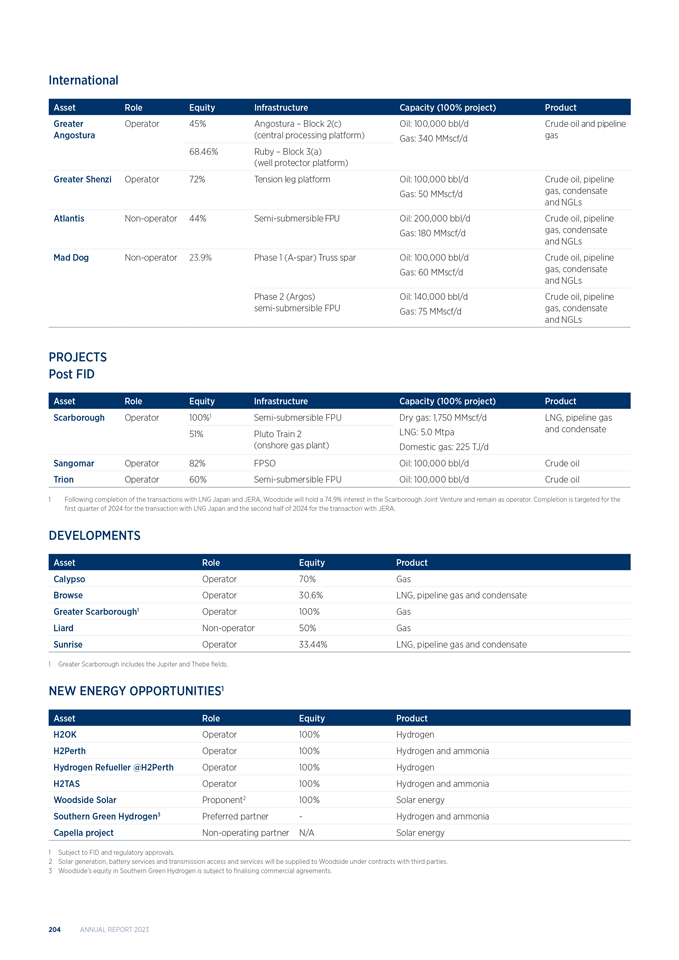

國際業務

伍德賽德·S國際投資組合包括在美國墨西哥灣和加勒比海地區的資產,並嵌入了增長選項。2023年,伍德賽德·S在國際業務生產中的份額為42.1百萬桶。

沈子

神子是通過位於美國墨西哥灣的張力腿平臺(TLP)開發的常規油氣田。有16個生產商流入TLP和6口注水井。此外,兩口海底油井被綁回不運行的馬可波羅平臺。Shenzi North是

Shenzi TLP的雙井水下回接。該項目於9月實現迴流。由於儲層連通性,生產表現低於預期。深梓設施於二零二三年的可靠性達到97%以上。伍德賽德公司在深子公司的產量份額為10.8萬桶。Woodside是運營商,持有72%的參與權益。

亞特蘭蒂斯

Atlantis是一個傳統的石油和天然氣開發項目,是美國墨西哥灣最大的油田之一。Atlantis開發項目包括一個半潛式

設施,其中有28口生產井和3口注水井。兩口井(一口生產井和一口注入井)於2023年完成,同時進行了廣泛的井榦預活動。Woodside公司在Atlantis的產量份額於2023年為1260萬桶。伍德賽德持有44%的股份。 非經營性參與利益。 圖片來源:BP

瘋狗

Mad Dog是一個傳統的石油和天然氣開發項目,位於美國墨西哥灣。第1階段開發包括一個Spar設施

(A—spar)具有鑽井能力和10口活躍生產井。Mad Dog二期是通過新的Argos浮動生產設施開發的Mad Dog油田南側。第一批石油於2023年4月實現,全年產量均有所增加。2023年成功鑽探了一口評價井,將油田擴展到西南部。隨後,共同所有者批准了三口井

水下回接。伍德賽德在2023年的《瘋狗》中的份額為720萬桶。Woodside持有23.9%非經營性參與權益。

大安哥拉

大安戈斯圖拉包括位於特立尼達和多巴哥近海的安戈斯圖拉和魯比常規油氣田

。該開發項目包括一個海上中央處理設施和五個井口平臺。Woodside是運營商,持有Angostura油田45%的參與權益和Ruby油田68.5%的參與權益。伍德賽德集團於2023年在大安戈斯圖拉的產量份額為11.2百萬桶。2023年實施的增產活動包括天然氣

注入器—生產器油井轉換、降低油井背壓和增加射孔。這些增加導致儲備金增加。22年度報告

2023

3.3我們的業務

市場營銷和貿易

Woodside在亞太和大西洋盆地擁有一個全球投資組合,在LNG、凝析油、原油和液化天然氣(NGL)貨物的綜合航運、運營、營銷和貿易

活動方面擁有良好的業績記錄。市場營銷分部於二零二三年的税前溢利為3. 75億元。這反映了優化活動和通過

營銷、貿易和運輸Woodside Koses石油和天然氣以及通過第三方購買價值產生的增量價值。伍德賽德公司的液化天然氣投資組合通過短期、中期和長期合同組合進行管理,供應的貨物來自生產

資產或從第三方購買。2023年,伍德賽德公司生產的液化天然氣對天然氣樞紐指數的敞口為30%。伍德賽德公司的液化天然氣貿易活動旨在最大限度地提高我們液化天然氣投資組合的價值。第三方貨物通過長期承購協議從Corpus

Christi LNG購買,並通過我們與其他生產商和貿易商的關係從現貨市場購買。原油、凝析油和天然氣液化油的營銷主要基於短期銷售,並輔之以期限

安排。在墨西哥灣,原油被出售給美國墨西哥灣沿岸的煉油廠和貿易商。Woodside還通過向國際市場出口原油的能力增加了其運營靈活性。在特立尼達和多巴哥,原油銷往國際市場,天然氣銷往國內市場。天然氣在西澳大利亞州和東海岸都有銷售。在西澳大利亞州,Woodside公司的國內天然氣義務

由多個生產資產支付。所有伍德賽德的生產從巴斯海峽銷售到東海岸的國內市場。2023年,伍德賽德公司的西澳大利亞州資產生產了76千兆焦耳(PJ)天然氣,約佔西澳大利亞州國內天然氣供應的19%。伍德賽德公司在巴斯海峽產量中的份額為97 PJ,約佔供應給東海岸市場的所有天然氣的19%。Woodside公司的營銷和交易組合

由我們的航運能力支持,其中包括六艘長期合同船舶和多艘短期租賃船舶。伍德賽德又租了五輛 新建液化天然氣船舶,以支持斯卡伯勒液化天然氣貨物的交付和貿易活動的增長。新建造的船隻預計將在2024年至2026年之間交付。2023年4月,與PerDaman Chemical and Fertiliser Pty Ltd.簽訂的長期天然氣買賣協議(GSPA)

成為無條件協議。根據GSPA,天然氣的供應量約為每天130 TJ,預計從2026年或2027年開始,為期20年。伍德賽德還簽署了幾項天然氣銷售協議,向東海岸和西澳大利亞州的國內客户(包括零售商和商業和工業用户)總共供應約128PJ的管道天然氣。交付已經開始,預計將持續到2026年。此外,Woodside還與Pilbara Minerals的全資子公司Pilgangoora Operations Pty Ltd簽署了一項SPA,從冥王星卡車裝載設施供應國內液化天然氣。SPA項下的供應合同將於2024年開始,為期五年。2023年8月,伍德塞德和LJ斯卡伯勒私人有限公司(液化天然氣日本)簽訂了一項不具約束力的協議,從2026.1開始的10年內每年銷售和購買12批液化天然氣(每年約90萬噸(Mtpa))。該協議是與日本液化天然氣及其母公司更廣泛戰略關係的一部分,其中包括出售斯卡伯勒合資企業10%的非運營參與權益,並就新能源的機會進行合作。2 2023年12月,伍德賽德與墨西哥太平洋有限公司(墨西哥太平洋)簽署了一項SPA,從墨西哥太平洋S位於墨西哥太平洋海岸的Saguaro Energia液化天然氣項目購買130萬噸液化天然氣,為期20年。SPA將接受墨西哥太平洋公司對擬議中的第三列列車的FID,預計將於2024年下半年進行。商業運營計劃於2029年開始。期後,伍德賽德和傑拉簽訂了一份不具約束力的協議負責人,從2026年開始,每年從伍德賽德S全球投資組合出貨,銷售和購買六批液化天然氣貨物,為期10年。這項協議是與JERA更廣泛戰略關係的一部分,其中包括在斯卡伯勒合資企業中的股權以及在新能源和低碳服務方面的合作機會。1 LJ Scarborough Pty Ltd目前是LNG Japan Corporation的全資子公司,LNG Japan Corporation是住友商事株式會社和Sojitz Corporation各持股50%的合資企業。2交易完成後,目標為2024年第一季度。伍德賽德能源集團有限公司23

3.4我們的業務

項目

伍德賽德S的項目組合以專注於安全、低成本和低碳解決方案的項目交付能力為基礎。

斯卡伯勒能源項目

斯卡伯勒氣田位於卡納馮盆地,距離西澳大利亞海岸約375公里。該油田正通過一條約430公里長的管道與現有冥王星液化天然氣陸上設施的第二列液化天然氣列車相連的新海上設施進行開發。斯卡伯勒油田的開發包括安裝一個浮式機組,在初始階段鑽8口井,在油田的整個生命週期內鑽13口井。Pluto LNG的擴展包括建造第二個LNG列車(Pluto Train 2),

安裝額外的國內天然氣處理設施和配套基礎設施,以及對現有的Pluto Train 1進行改造,使其能夠處理斯卡伯勒天然氣。斯卡伯勒天然氣預計將從冥王星列車2生產約5 Mtpa的液化天然氣

,從現有的冥王星列車1生產高達3 Mtpa的液化天然氣。斯卡伯勒儲氣庫含有不到0.1%的CO。結合海上浮式2生產裝置和陸上冥王星列車2的加工設計效率,斯卡伯勒能源項目將是輸送到北亞市場的最低碳強度的液化天然氣來源之一。1 2023年底,該項目完成55%。2浮式生產裝置的製造正在進行中,生活區調試正在進行中,船體和頂部正在進行中。在這段時間之後,船體離開了它的第一個幹船塢,火炬吊杆安裝在頂部。海底輸油管和幹線的製造已經完成。監管機構於去年12月接受了地震、鑽井、海底和幹線安裝活動的環境規劃。在這一批准之後,地震規劃順利完成。在此期間之後,安裝了第一條海底輸油管,開始鑽探生產井,並完成了近岸管道安裝工作。英聯邦水域管道剩餘部分的工作正在進行中。冥王星列車2號現場工作進展順利,準備在2024年交付設備和模塊。截至2023年底,已澆築了約33000立方米混凝土,豎立了564噸結構鋼,並安裝了3公里長的管道。6個模塊的製造已經完成,另外38個模塊正在進行中。在該期間之後完成了更多的單元。工程、採購和建設管理(EPCM)承包商被選為冥王星1號列車改裝的承包商,長期項目的工程和採購正在進行中。冥王星列車2號的準備工作在2023年5月冥王星液化天然氣週轉期間進行了對接。Woodside於2023年11月參加了斯卡伯勒綜合遠程操作中心(IROC)的FID。IROC將允許斯卡伯勒和冥王星設施從珀斯遠程操作。2023年8月,Woodside與LNG Japan訂立協議,出售斯卡伯勒合資企業10%的非經營性參與權益。3期後,Woodside與JERA達成協議,出售Scarborough合資企業15.1%

非經營性參與權益。4 Woodside是運營商,持有100%股權斯卡伯勒(Scarborough)的參與權益、冥王星列車2(Pluto Train 2)的參與權益和冥王星LNG(Pluto LNG5)的參與權益。

桑戈馬爾

Sangomar油氣田位於達喀爾以南約100公里處,是塞內加爾第一個海上石油項目。Sangomar油田開發第1階段正在開發

不太複雜的儲層單元,並測試其他儲層,以支持潛在的未來階段。石油將通過一個獨立的FPSO設施生產,該設施有23口水下油井和配套的水下基礎設施。它的設計是為了讓 後續階段的配合。FPSO Léopold Sédar Senghor是一艘改裝的油輪,配有新的上部結構、炮塔和繫泊系統,生產能力為每天100,000桶。FPSO於2023年12月離開新加坡,並於2024年2月抵達塞內加爾近海。第一階段鑽井和完井活動包括23口生產井、注氣井和注水井。天然氣和水的回注旨在

幫助最大限度地提高石油的採收率,並使天然氣能夠儲存起來以備將來使用。於2023年底,17口油井已完工,另有6口油井已部分完工。伍德麥肯齊排放基準。完成百分比不包括冥王星列車1號修改項目。LJ Scarborough Pty Ltd(LNG日本)目前是LNG日本株式會社的全資子公司,LNG日本株式會社是住友株式會社和Sojitz株式會社的50:50合資企業。待

交易完成後,目標為2024年第一季度。該買賣協議是與JERA Scarborough Pty Ltd簽署的,JERA Scarborough Pty Ltd是JERA Co.的全資子公司,Inc.待交易完成後,目標為

2024年下半年。在與LNG日本和JERA的交易完成後,Woodside將持有Scarborough合資企業74.9%的權益,並繼續擔任運營商。與LNG

Japan的交易預計於2024年第一季度完成,與JERA的交易預計於2024年下半年完成。2023年度報告

截至2023年底,該項目第一期已完成約93%。1於2023年5月,Sangomar合資企業批准鑽探額外生產井,以優化油田採收率。截至二零二三年底,該井的鑽探部分完成。Woodside致力於一個強大的本地內容計劃,其中包括培訓計劃,當地就業, 供應商商機和塞內加爾的能力建設。截至2023年6月,主要項目承包商報告塞內加爾員工完成了3000多個工作。能力建設活動現在集中在操作階段 。Woodside是Sangomar開採區的運營商,持有Sangomar開採區82%的參與權益,以及剩餘的Rufisque Offshore、Sangomar Offshore和Sangomar Deep Offshore(RSSD)評估區的90%的參與權益。Trion Trion是位於墨西哥灣的一個石油開發項目,距墨西哥海岸線約180公里,距美國/墨西哥海上邊界以南30公里,水深約2500米。Woodside於2023年6月宣佈Trion公司FID,墨西哥監管機構國家Hidrocarburos(CNH)於2023年8月批准了油田開發計劃(FDP)。伍德賽德以競爭性的方式投標了開發的主要範圍,在FID,大約70%的預測資本由一次總付或基於固定利率的確定投標支持。自國際開發署以來,關鍵合同逐步得到執行。FPU的工程、採購和建築合同是與現代重工簽訂的。 採購活動正在進行,與迄今為止執行的工程的成熟度相稱。推進這些活動將支持計劃於2024年進行的一次總付轉換。浮式儲運(FSO) 船 前端工程和設計(FEED)和船廠工程已經開始與SBM Offshore。經過充分談判的FSO裸船租賃以及運營和維護合同的目標是 在2024年FEED結束時執行。還授予了鑽井和完井、設施安裝和水下設備等關鍵合同。合同授予後,已訂購了用於上部結構和水下設施的長週期設備和材料 。Transocean於2023年7月獲得鑽井平臺合同。鑽機將在12個月前選定。該項目正在完善Trion本地內容計劃各要素的機會,並讓墨西哥的主要利益相關者 參與瞭解本地能力並確定優先次序。Woodside是運營商,持有60%的參與權益。1在 週期後確定的0.2%修正後,項目進度已更新為93%。伍德賽德能源集團有限公司

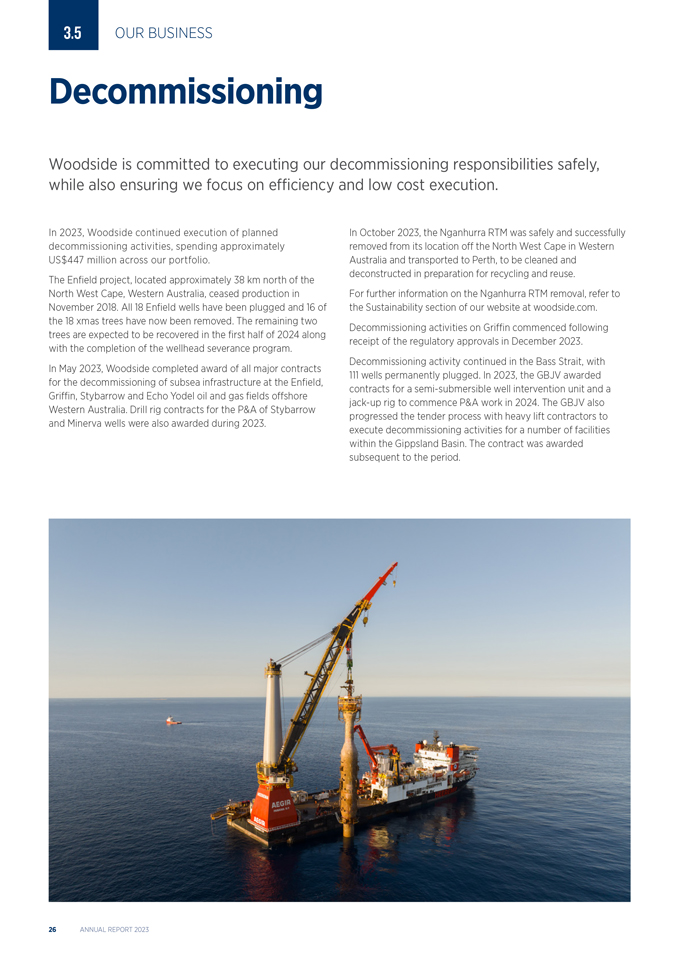

3.5我們的業務退役伍德賽德致力於安全地履行我們的退役責任,同時確保我們 專注於效率和低成本執行。2023年,伍德賽德繼續執行計劃中的退役活動,在我們的投資組合中花費了約4.47億美元。Enfield項目位於西澳大利亞州西北角以北約38公里處,於2018年11月停產。所有18個恩菲爾德油井都被堵住了,18棵聖誕樹中的16棵現在已經被移走。剩餘的兩棵樹預計將在2024年上半年隨着井口切斷計劃的完成而恢復。2023年5月,Woodside完成了西澳大利亞州近海Enfield、Griffin、Stybarrow和Echo Yodel油氣田海底基礎設施退役的所有主要合同的授予。2023年還授予了Stybarrow和Minerva油井P&A鑽機合同。2023年10月,Nganhurra RTM被安全、成功地從澳大利亞西北部開普敦附近的位置移走,運往珀斯,進行清潔和拆解,為回收和再利用做準備。有關移除Nganhurra RTM的更多信息,請參閲我們網站的可持續發展部分,網址為Wood side.com。格里芬上的退役活動在2023年12月收到監管批准後開始。巴斯海峽的退役活動仍在繼續,111口油井被永久封堵。2023年,GBJV授予了一個半潛式油井榦預裝置和一個自升式鑽井平臺將於2024年開始P&A工作。GBJV還推進了與重型起重設備承包商的招標進程,以執行吉普斯蘭盆地內許多設施的退役活動。合同是在這段時間之後授予的。2023年年報

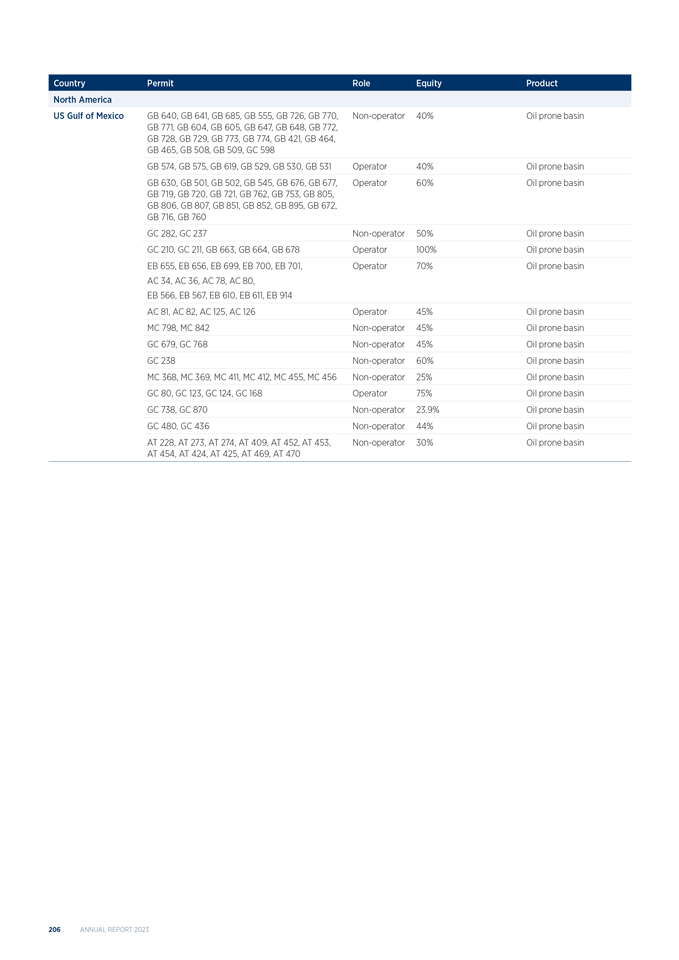

3.6我們的業務勘探和開發伍德賽德和S開發組合和有針對性的勘探計劃專注於 確定和解決關鍵的技術和商業元素,以使資源能夠競爭資本。Calypso Calypso位於距離特立尼達海岸約220公里處,水深2100米。該資源包括23(A)號區塊和TTDAA 14號區塊的幾個天然氣發現。該開發項目位於一個擁有現有基礎設施和有利需求前景的地區。2023年上半年,伍德賽德完成了概念性研究,並選擇了一個內場東道主作為首選的開發理念。預飼餵工程於2023年下半年開始,以完善這一概念的定義。繼續與主要利益相關者進行營銷和商業討論,以評估將資源貨幣化的選擇。伍德賽德是運營商,持有70%的參股權益。Browse Browse由位於西澳大利亞州布魯姆以北約425公里的離岸Browse盆地的CAlliance、Brecze和Torosa氣田和凝析氣田組成。繼續開展關鍵工作活動,以支持擬議的Browse to NWS項目開發,包括與環境監管機構就批准和推進商業協議進行接觸。海上設計中採用了CCS解決方案,以減少Browse油藏CO的很大比例。Browse合資企業正在評估進一步的碳減排2和能源效率機會,以減少和管理温室氣體排放。 伍德賽德是運營商,持有30.6%的股份。Liard The Liard氣田是一個位於加拿大不列顛哥倫比亞省的非常規氣田。2023年,伍德賽德完成了一筆交易,總部位於卡爾加里的派拉蒙資源公司獲得了利亞德油田28個租約50%的股權和運營權。伍德賽德簽署了一項協議,加入落基山脈液化天然氣合作伙伴關係,作為可能通過加拿大西海岸出口液化天然氣的選項。落基山脈LNG合作伙伴關係正在與不列顛哥倫比亞省KSI Lisims LNG項目的開發商西部LNG和Nisga國家合作。伍德賽德持有Liard油田50%的參股權益。日出日出包括日出和特魯巴杜爾氣田和凝析油氣田,這些氣田位於澳大利亞達爾文西北約450公里,東帝汶以南約150公里。2023年,日出合資企業(Sjv)的參與者繼續與澳大利亞和東帝汶政府就新的大日出生產分享合同和其他相關文件進行接觸。Sjv還與東帝汶和澳大利亞政府達成協議,將在2024年對潛在的發展進行概念研究,向相關利益攸關方通報情況。該研究將審議通過東帝汶和澳大利亞開發、加工和銷售天然氣的關鍵問題。除此之外,澳大利亞的NT/RL2和NT/RL4的保留租約也得到了續簽。伍德賽德是運營商,持有33.44%的參與權益。勘探伍德賽德S的勘探戰略仍然專注於獲取、測試和開發低成本、低碳、增值的機會,這些機會的特點和項目進度能夠在能源過渡期間保持彈性。在美國墨西哥灣,伍德賽德在259年的租賃銷售中獲得了5個租約,並在261.1租賃銷售的18個租約中出價最高。伍德賽德獲得了綠色峽谷延伸區兩個租約的44%的工作權益 ,並參與了尖晶石油井的鑽探(未運營),該油井沒有遇到碳氫化合物。此外,還收購了阿特沃特河谷延伸區11個租約30%的營運權益。埃及監管機構批准了伍德賽德·S收購希羅多德盆地兩個未運營區塊27%的權益。伍德賽德簽署了一項期權協議,收購了位於納米比亞近海奧蘭治盆地的石油勘探許可證87至少56%的權益。地震採集已經完成,將在2024年對地震數據進行評估後,決定是否行使進入選擇權。伍德賽德繼續優化其勘探組合,退出不再被視為有前景的區塊。這包括決定撤出特立尼達和多巴哥深水第5區塊,並完成加拿大、大韓民國、祕魯和緬甸A-6近海區塊的正式撤離活動。1租賃銷售租約的最終授予261正在等待監管部門的批准。伍德賽德能源集團有限公司27

3.7我們的業務新能源和碳解決方案Woodside專注於開發新能源產品和低碳 服務,以幫助Woodside和我們的客户減少排放。NEW ENERGY United States H2OK H2OK是一個擬議中的液氫項目,位於俄克拉荷馬州Ardmore,預計每天生產60噸液氫(tpd)。 Woodside於2023年繼續推進技術、監管和承包活動。Woodside正在評估擬議的美國聯邦政府税收激勵標準,以確定對該項目的影響,並正在努力敲定客户 承購協議,以支持潛在的FID。Woodside是運營商,持有100%參與權益。2023年,Woodside評估了地點,並在一個潛在的大規模氨生產和出口設施的機會的早期階段進行了進展。Heliogen協作公司Woodside和Heliogen有一項項目協議,將在加利福尼亞州部署Heliogen公司人工智能使能集中太陽能技術的5兆瓦示範模塊,稱為Capella項目。2023年,該項目完成FEED。亞太H2Perth是一個擬議的氫氣和氨生產設施,位於西澳大利亞州Perth。2023年,向英聯邦和西澳大利亞監管機構提交了主要環境批准申請文件。H2Perth的氫氣補充站是一個擬建的自給式氫氣生產、儲存和燃料補充站,於2023年實現FID。H2TAS是一個擬議的可再生 氨和氫氣生產設施,位於塔斯馬尼亞州的貝爾灣地區。2023年,Woodside繼續評估電力解決方案和承購機會。Southern Green Hydrogen是一個擬建的可再生氨生產設施 ,位於新西蘭Southland。1 2023年,繼續為Southern Green Hydrogen的商業安排敲定工作。碳捕獲和回收(CCS)Woodside作為多個合資企業的參與者,持有三個温室氣體 評估許可證,並且是擬議的東南澳大利亞(SEA)CCS項目的參與者。2 2023年,Woodside進入了三個 不具約束力的諒解備忘錄,以便研究日本和澳大利亞之間潛在的CCS價值鏈。項目3 Angel(已運行)Bonaparte(未運行)SEA CCS(未運行)描述擬議的大規模多用户CCS樞紐擬議的大規模多用户CCS樞紐擬議的多階段CCS項目。 第一階段旨在捕獲排放的碳,旨在捕獲項目排放的碳,將利用現有的基礎設施多 行業。多個行業。 在枯竭的布里姆油田儲存CO。地點Offshore,North West Australia Offshore,South East Australia Offshore利息20% 21% 50% 2023年活動開始FEED前研究並進展於2023年8月開始概念選擇。 支持提交環境 轉介的活動。碳信用投資組合4 Woodside利用碳信用來抵消股權範圍1和範圍2的温室氣體排放,這些温室氣體排放高於我們的淨減排目標。 2023年,Woodside在西澳大利亞種植了約270萬株混合 幼苗,作為我們在Woodside擁有的土地上約4,700公頃土地上種植的原住民再造林項目的一部分。5在塞內加爾,Woodside正在為Sine Saloum和Casamance地區多達7,000公頃紅樹林的恢復提供資金。伍德賽德預計將在30年內從該項目獲得多達140萬個碳信用額度。Woodside專注於與碳捕集和利用(CCU) 技術開發人員合作,並正在評估在示範規模試點項目中部署其技術的機會,以便在可能的大規模部署之前。在2022年達成協議後,Woodside於2023年與CCU技術開發商LanzaTech、NovoNutrients、StringBio和多家工程公司完成了多項工程研究。伍德賽德在南方綠色氫的股權將取決於最終確定的商業協議。有關我們的温室氣體評估許可證的信息,以及《氣候轉變行動計劃》和《2023年進度報告》,以瞭解有關伍德賽德公司CCS項目的更多信息。本表提供了有關建議的CCS機會的信息,重點是範圍3排放。我們還在努力開發這裏沒有提到的其他機會。請參閲第3.4節"氣候轉型行動計劃和2023年進度報告中碳信用額度的使用",瞭解更多 有關Woodside公司碳信用額度使用的信息。該項目有潛力在25年內隔離約2,000 kt CO—e。2023年度報告

3.8我們的業務環境及可持續發展我們應用可持續發展的理念,指導業務各級決策。 2023年,我們的可持續發展活動和披露持續發展,以應對可持續發展主題、新出現的強制性可持續發展標準和投資者優先事項的戰略重要性。因此,我們將重大可持續發展主題的摘要披露 提升至年度報告,不再發布獨立的年度可持續發展報告,並在woodside.com上納入額外信息。氣候過渡行動計劃和2023年進展報告 氣候過渡行動計劃和2023年進展報告概述了伍德賽德公司2023年1月1日至2023年12月31日期間的氣候相關計劃、活動、進展和氣候相關數據。Woodside認為, 氣候轉變行動計劃和2023年進度報告包含的披露內容符合TCFD的四項建議和11項建議披露內容,並注意到其針對所有部門的指南和 Non-Financial Groups.1,2 This Annual Report should be read in conjunction with Woodsides Climate Transition Action Plan and 2023 Progress Report.3 SUSTAINABILITY STRATEGY We refreshed our Sustainability Strategy in 2023, to incorporate relevant sustainability-related risks and opportunities and reflect the direction of our business. The Sustainability Strategy supports our Corporate Strategy and places an increased focus on those sustainability topics most relevant to our current business activities and the communities where we are active. Our Sustainability Strategy is built on the foundation of the following principles: Integrity, accountability and transparency drive our environmental, social and governance aspirations and guide decision making at all levels of our business. We strive to operate responsibly across our business activities. Enduring and meaningful relationships with communities are fundamental to our social performance. We recognise that our success is driven by our people and our culture. We value diversity and we strive to keep each other safe. More information regarding our Sustainability Strategy is available at woodside.com. MATERIALITY PROCESS Woodside conducts a materiality assessment process to inform our understanding of which sustainability topics are most relevant to our business activities and stakeholders. This considers potential risks, opportunities and impacts of sustainability topics upon our financial performance, as well as the potential impacts of our operations on stakeholders. This process involves a study by internal subject matter experts drawing from a range of internal and external inputs, including from our Executive Leadership Team and Directors. We also continue to monitor developments, trends and stakeholder views throughout the year. Our approach seeks to understand the topics relevant to our business activities and to our stakeholders. Potential risks, opportunities and impacts on the economy, environment and people, including impacts on human rights, are taken into account. Engagements with stakeholders via online surveys and interviews help verify and prioritise relevant topics. We engage with stakeholders such as customers, employees, investors, banks and ratings agencies, joint venture participants, First Nations communities, local communities, local, state and national governments, non-government organisations, suppliers and contractors. We classify the topics into three categories of material, significant or important. This is followed by an endorsement process with our Executive Leadership Team and the Boards Sustainability Committee. Our 2023 material sustainability topics remain consistent with the previous year, including Climate, Health safety and wellbeing, Environment and biodiversity and First Nations cultural heritage and engagement.4 Climate Health, safety and wellbeing Environment First Nations cultural heritage and biodiversity and engagement 1 Financial Stability Board, 2017. Recommendations of the Task Force on Climate-related Financial Disclosures. Final Report. Figure 4, p. 14. Some elements of the TCFDs four recommendations and 11 recommended disclosure have been presented in different order to enhance readability. 2 Financial Stability Board, 2021. Implementing the Recommendations of the Task Force on Climate-related Financial Disclosures. 3 Woodside notes that following the completion of its 2023 status report, the TCFD has fulfilled its remit and disbanded. The Financial Security Board of the Bank of International Settlements has asked the International Financial Reporting Standards (IFRS) Foundation to take over the monitoring of the progress of companies climate-related disclosures. 4 For the purposes of Woodsides sustainability disclosures we classify the topics into three categories of material, significant or important. For these purposes, material topic means a 2023 sustainability topic described in this report, determined as part of the 2023 materiality assessment process undertaken by Woodside. Classification of any topic as material, significant or important should not be read as a determination of whether that topic may necessarily rise to the level of materiality of disclosures required by law, including the laws of Australia, the United States and the United Kingdom. WOODSIDE ENERGY GROUP LTD 29

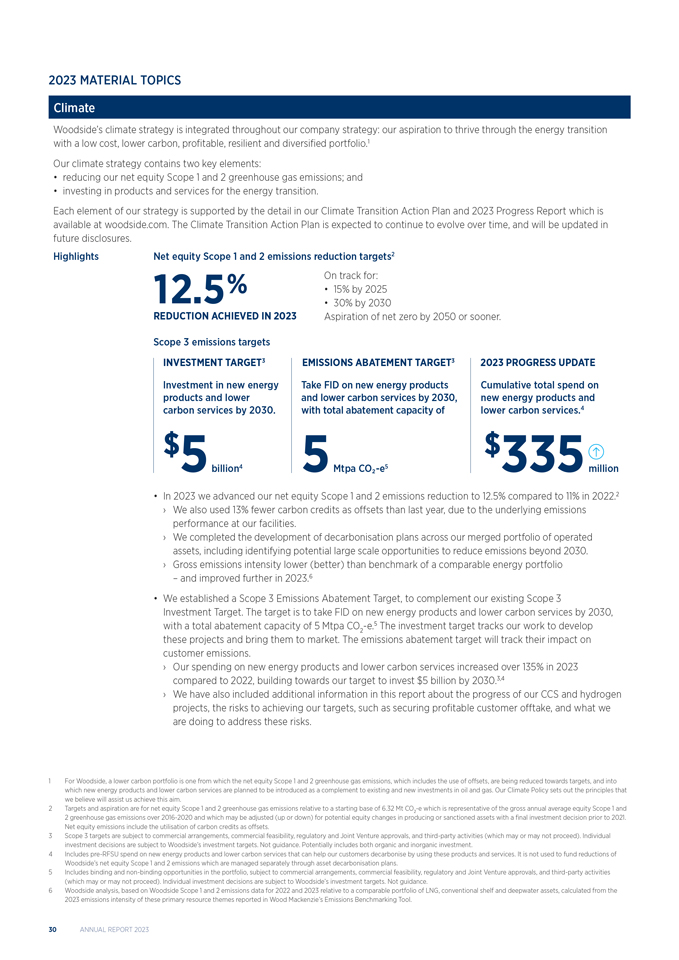

2023材料主題氣候伍德賽德的氣候戰略貫穿我們的整個公司戰略:我們希望通過低成本、低碳、盈利、彈性和多樣化的投資組合,在能源轉型中蓬勃發展 。1我們的氣候戰略包含兩個關鍵要素:減少我們的淨資產範圍1和範圍2温室氣體排放;以及投資 促進能源轉型的產品和服務。我們戰略的每一個要素都得到了我們的氣候轉變行動計劃和2023年進度報告的詳細支持,該報告可在woodside.com上查閲。預計《氣候過渡行動計劃》將隨着時間的推移而不斷演變,並將在未來的披露中更新。亮點淨權益範圍1和2的減排目標2如期實現:到2025年減少12. 5%至2030年減少30%至2023年減少 預期到2050年或更早實現淨零。 範圍3排放目標投資目標3減排目標3 2023年進展新能源投資採用FID對新能源產品的投資到2030年前, 產品及低碳及低碳服務的累計總支出,到2030年,新能源產品及碳服務的累計總支出,以及低碳服務的總減排能力。4 50億美元4 5百萬噸二氧化碳5 $3. 35億美元二零二三年,我們將 範圍1及2的淨權益減少幅度提高至12. 5%,而2022年則為11%。 我們完成了 在合併後的運營資產組合中制定脱碳計劃,包括確定2030年以後減少排放的潛在大規模機會。 總排放強度低於 可比能源組合的基準,並於2023年進一步改善。6目標是到2030年,在新能源產品和低碳 服務方面採用FID,總減排能力達到500萬噸二氧化碳 -e.5 The investment target tracks our work to develop these projects and bring them to market. The 2 emissions abatement target will track their impact on customer emissions. Our spending on new energy products and lower carbon services increased over 135% in 2023 compared to 2022, building towards our target to invest $5 billion by 2030.3,4 We have also included additional information in this report about the progress of our CCS and hydrogen projects, the risks to achieving our targets, such as securing profitable customer offtake, and what we are doing to address these risks. 1 For Woodside, a lower carbon portfolio is one from which the net equity Scope 1 and 2 greenhouse gas emissions, which includes the use of offsets, are being reduced towards targets, and into which new energy products and lower carbon services are planned to be introduced as a complement to existing and new investments in oil and gas. Our Climate Policy sets out the principles that we believe will assist us achieve this aim. 2 Targets and aspiration are for net equity Scope 1 and 2 greenhouse gas emissions relative to a starting base of 6.32 Mt CO -e which is representative of the gross annual average equity Scope 1 and 2 greenhouse gas emissions over 2016-2020 and which may be adjusted (up or down) for potential equity changes in producing 2 or sanctioned assets with a final investment decision prior to 2021. Net equity emissions include the utilisation of carbon credits as offsets. 3 Scope 3 targets are subject to commercial arrangements, commercial feasibility, regulatory and Joint Venture approvals, and third-party activities (which may or may not proceed). Individual investment decisions are subject to Woodsides investment targets. Not guidance. Potentially includes both organic and inorganic investment. 4 Includes pre-RFSU spend on new energy products and lower carbon services that can help our customers decarbonise by using these products and services. It is not used to fund reductions of Woodsides net equity Scope 1 and 2 emissions which are managed separately through asset decarbonisation plans. 5 Includes binding and non-binding opportunities in the portfolio, subject to commercial arrangements, commercial feasibility, regulatory and Joint Venture approvals, and third-party activities (which may or may not proceed). Individual investment decisions are subject to Woodsides investment targets. Not guidance. 6 Woodside analysis, based on Woodside Scope 1 and 2 emissions data for 2022 and 2023 relative to a comparable portfolio of LNG, conventional shelf and deepwater assets, calculated from the 2023 emissions intensity of these primary resource themes reported in Wood Mackenzies Emissions Benchmarking Tool. 30 ANNUAL REPORT 2023

我們與氣候相關的機遇和風險概述如下,並在《氣候轉型行動計劃和2023年進展報告》第5.0節中詳細描述。這包括如何將這些流程集成到Woodside的整體風險管理框架中的細節。潛在氣候相關機會的類別包括:資源效率、能源、機會、產品和服務、市場和復原力。 潛在風險潛在氣候相關風險的類別包括:政策和法律風險、技術、市場和 聲譽等過渡風險;急性和慢性等物理風險。 另見第3.9節"風險因素"。我們的方法這是我們的氣候轉變行動計劃和2023年進展報告的簡要摘要,應全文閲讀, 可在woodside.com查閲。減少淨權益範圍1和2温室氣體排放Woodside的目標是到二零二五年將淨權益範圍1和2温室氣體排放量減少15%,到二零三零年減少30%,並期望到二零五零年或更快實現淨零排放量。減少我們的淨權益範圍1和2温室氣體排放由三個槓桿支持:在設計中避免排放,在運營中減少排放 ,以及在碳信用額中抵消剩餘部分。Woodside長期以來一直關注能源效率。我們第一個正式的氣候相關目標是在2016—2020年期間實現5%的能源效率目標。我們超過了這個目標,達到了8%。脱碳規劃我們的首要任務是避免及減少排放。伍德賽德運營的所有資產和項目必須制定脱碳計劃,以確定減少設施排放的技術機會,以便 機會可以進一步評估工程和商業可行性。估計成本低於我們內部長期碳成本(80美元/噸CO)的機會 -e (real terms 2022) are 2 incorporated into asset or project level business plans.2 These opportunities are at varying levels of maturity. To date: Opportunities that we estimate could avoid approximately 16 million tonnes CO -e (cumulatively to 2050) have been incorporated 2 into the design of the Scarborough, Pluto Train 2 and Trion projects3 Around a further 70 opportunities, which we estimate could avoid approximately 12 million tonnes CO -e (cumulatively to 2050) 2 are targeted for completion at our existing facilities by 2030.3 We estimate that the opportunities still to be implemented at our existing operating facilities could have a combined capital cost of around $200 million.3 Large scale abatement plan Emissions reduction opportunities that are estimated to cost more than $80/t CO -e are reviewed by our Executive Leadership 2 Team.2 They are subject to more engineering, cost reduction or technology maturation in a company-wide large scale abatement plan, as depicted in the chart below. If they can be matured to an appropriate level, they will be reassessed by the Executive Leadership Team and progressed where appropriate. The proposed Woodside Solar project is an example of a project likely costing more than $80/t CO -e that is progressing. 2 LNG facilities are the source of the majority of our emissions. They arise from reservoir CO , power generation, mechanical turbines and our flaring system. Electrification (using renewable or lower carbon power), CCS and hydrogen 2 fuelling of turbines are all options that could reduce these emissions, creating choices in the optimal mix. 1 Targets and aspiration are for net equity Scope 1 and 2 greenhouse gas emissions relative to a starting base of 6.32 Mt CO -e which is representative of the gross annual average equity Scope 1 and 2 greenhouse gas emissions over 2016-2020 and which may be adjusted (up or down) for potential equity changes in producing 2 or sanctioned assets with a final investment decision prior to 2021. Net equity emissions include the utilisation of carbon credits as offsets. 2 Woodsides assumptions on carbon cost pricing include a long-term carbon price of US$80/tonne of emissions (real terms 2022). Woodside continues to monitor the uncertainty around climate change risks and will revise carbon pricing assumptions accordingly. 3 Indicative only, not guidance. Potential impact of opportunities identified in asset decarbonisation plans assuming all opportunities identified progress to execution, which is not certain and remains subject to further maturity of cost and engineering definition. Greenhouse gas quantities are estimated using engineering judgement by Woodside engineers. Please refer to Climate Transition Action Plan section 7.6 Disclaimer, risks, emissions data and other important information for important cautionary information relating to forward looking statements. WOODSIDE ENERGY GROUP LTD 31

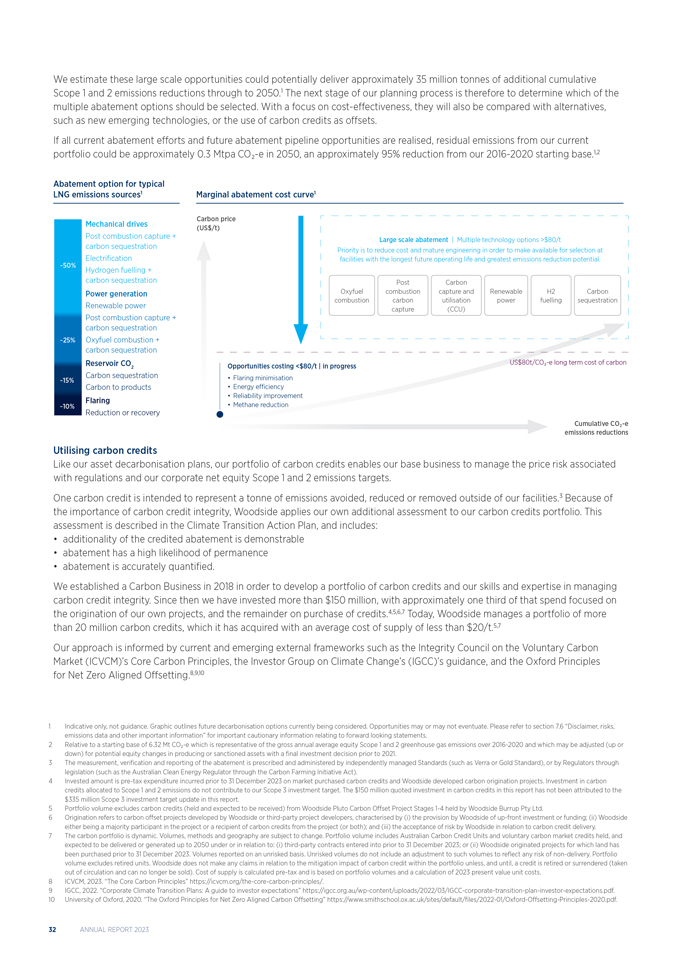

我們估計,這些大規模機會可能會在2050年之前實現約3500萬噸的額外累積 範圍1和範圍2減排量。因此,我們規劃過程的下一階段是確定應選擇多個減排方案中的哪一個。在注重成本效益的情況下,它們還將與 替代品進行比較,例如新興技術,或使用碳信用額作為抵消。如果當前的所有減排努力和未來減排管道機會都得到實現,我們當前產品組合的剩餘排放量可能約為 0.3百萬噸/年 到2050年,二氧化碳排放量比我們2016—2020年的起始基數減少約95%。1,2典型LNG排放源的減排方案1邊際減排成本曲線1碳價格 機械驅動器(美元/噸)燃燒後捕集+大規模減排 多種技術選項> 80美元/噸碳封存優先事項是降低成本和成熟的工程設計,以便 未來運行壽命最長和減排潛力最大的電氣化設施可供選擇。 | ~50%氫燃料+碳封存後碳發電富氧燃料燃燒捕集 和可再生H2碳燃燒碳利用功率燃料捕集再生電力捕集(CCU)燃燒後捕集+碳封存~25%富氧燃料燃燒+碳封存儲集 CO2機會成本

INVEST IN PRODUCTS AND SERVICES FOR THE ENERGY TRANSITION Investing in products and services for the energy transition is supported by three levers: assessing investments for their resilience to the energy transition diversifying our products and services and supporting our customers and suppliers to reduce their emissions. Assessing investments The precise shape and pace of the energy transition is uncertain. It is expected to vary across countries because they have different starting points, development requirements, resources and capabilities. However, the scale of the transition is clearer as it will take many trillions of dollars, invested over decades. The International Renewable Energy Agency (IRENA) estimates it will require $150 trillion of cumulative investment by 2050.1 Whilst the scale of the investment required for the energy transition creates opportunity for Woodside, its inherent uncertainty and potential volatility creates risks. We believe that acknowledging the uncertainty and building resilience to it is a better response than picking a single future scenario and acting as if it were certain. This approach requires us: to carefully analyse a wide range of energy market and climate-related scenarios diversify our portfolio to meet changing customer demand have a disciplined capital allocation framework to focus our investments where we believe we will be most competitive work diligently with our customers to understand and meet their needs so that ultimately we secure their purchase of our products and services. We have developed a transition case methodology which, like a business case and a safety case, helps us to manage risk by assessing investment opportunities across a range of climate-related factors. There are currently six elements to our transition case methodology, which was first applied to the final investment decision for the Trion development in the Mexican segment of the Gulf of Mexico in 2023. Transition case for oil and gas investments We consider: 1. Investment attractiveness utilising a range of economic 4.Climate-related risks and opportunities by comparing assumptions informed by climate scenarios as well as the impact with and without opportunity on our other factors such as geopolitics and macroeconomics. portfolio aggregate climate risk exposure. 2. Cash flow scenario analysis impact by comparing the 5.Scope 1 and 2 portfolio emissions assessing the impact with and without opportunity on future cash impact of design out work on project emissions, and of flows using scenarios, including a 1.5°C case.2 residual emissions upon portfolio emissions abatement 3. Potential demand resilience analysis considering the demand, and portfolio emissions intensity. competitiveness of the projects cost of supply relative 6. Scope 1, 2 and 3 portfolio emissions intensity by to the range of demand in IPCC scenarios, including comparing the impact with and without opportunity 1.5°C cases. on our portfolio. 1 IRENA, 2023. World Energy Transitions Outlook 2023: 1.5°C pathway. International Renewable Energy Agency, Abu Dhabi. Page 134. 2 IPCC, 2023. Climate Change 2023: Synthesis Report. Contribution of Working Groups I, II and III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change, [核心寫作團隊,H。Lee and J. Romero (eds.)].氣專委,日內瓦,瑞士,doi: 10.59327/IPCC/AR6—9789291691647,https://www.ipcc.ch/report/ar6/config/downloads/report/IPCC_AR6_SYR_FullVol. pdf在本頁後續腳註中被稱為IPCC,2023。CHAR6—SYR CHINA.伍德能源集團有限公司33

多樣化我們的產品組合Woodside正致力於通過在現有 產品的基礎上增加新產品和服務來實現產品組合的多樣化,我們相信我們擁有競爭優勢,可以在能源轉型期間成功地提供這些產品。2021年,Woodside制定了範圍3投資目標,旨在到2030年在新能源產品和低碳服務方面投資50億美元。1,2截至2023年底,我們已累計為該目標支出超過3.35億美元,2023年支出較2022年增長超過135%。1,2我們預計支出將繼續增加至目標期的後期 ,由於大部分項目支出發生在建設階段,因此要視市場的發展而定。Woodside已經設定了一個補充的範圍3排放減排目標,以表明這些產品 和服務對客户範圍1或2排放的潛在減排影響。該目標是到2030年對新能源產品和低碳服務做出最終投資決定,總減排能力為500萬噸二氧化碳 —e.1,3 2投資目標跟蹤我們開發這些項目並將其推向市場的工作。減排目標將跟蹤其對客户排放的潛在影響。我們方法的其他要素在我們的 氣候轉型行動計劃和2023年進度報告中有更詳細的描述。我們的表現見上文的重點章節,以及《氣候變化行動計劃》和《2023年進展報告》以瞭解更多信息。1範圍3目標受商業 安排、商業可行性、監管和合資企業批准以及第三方活動(可能會進行也可能不會進行)的約束。個人投資決定受Woodside的投資目標限制。不是指導。潛在 包括有機和無機投資。2包括RFSU前在新能源產品和低碳服務上的支出,這些產品和服務可以幫助我們的客户通過使用這些產品和服務實現脱碳。 其不用於為伍德賽德公司淨權益範圍1和2排放量的減少提供資金,這兩項排放量通過資產脱碳計劃單獨管理。3在 投資組合中包括有約束力和不具約束力的機會,取決於商業安排、商業可行性、監管和合資企業的批准以及第三方活動(可能進行也可能不進行)。個人投資決策受伍德賽德投資 目標的影響。不是指導。34 2023年度報告

Health, safety and wellbeing Protecting the health and safety of our people, our contractors and our host communities is a top priority at Woodside. We focus on health and safety because we believe that everyone should be able to go home in the same condition as they started the day. We aim to be an industry leader in health and safety outcomes to protect people, communities and environments. We expect all our workers (including employees and contractors) to prioritise their own health and safety and that of others to keep each other safe. We strongly believe in embedding a safety culture where our people are empowered to take action to prevent injuries and maintain a safe working environment. The fatality of our colleague, a contractor employee, on the North Rankin Complex (NRC) continues to affect many of us. Our response prioritised the immediate safety and wellbeing of the workforce on the NRC. The Woodside Board convened and members of our Board and Executive Leadership Team visited our operational sites to meet with our workers (including employees and contractors) and offer their support. We completed a significant internal investigation into the incident and presented the findings and agreed actions to the Board and the National Offshore Petroleum Safety and Environmental Management Authority. In the fourth quarter of 2023, we facilitated an external review of our integrated safety and operational systems and plan to incorporate recommendations of this review into actions as part of a continuous improvement to our safety performance. Highlights Employee survey results showed us that our people feel empowered to speak up and act on health and safety issues. The framework for our new Woodside Field Leadership Program was developed and we commenced testing with our Australian based workforce. Integration of our global approach to wellbeing, event reporting and investigations, health, safety and environment (HSE) in contracting and performance monitoring was progressed. Potential Continue to learn from the incident on the NRC that led to the fatality of our colleague employed opportunities by a contractor company and other significant events. Embed our Field Leadership Program to strengthen understanding of our work practices and make improvements to HSE risk controls. Improve tracking and visibility of leading indicators of HSE performance. Potential risks Significant loss of primary containment process safety events. Failure to effectively plan and execute high-risk work activities. Failure to apply lessons from investigations and Field Leadership Program engagements leading to repeated events. See also section 3.9Risk factors. Our approach At Woodside everything we do is guided by Our Values. Everyone has the right to come to work and feel safe. Woodside continues its longstanding commitment to building and maintaining a work environment that is free from all forms of discrimination and inappropriate behaviour including sexual harassment. Our Code of Conduct defines the expected behaviours of everyone working at Woodside. Implementation of our Working Respectfully Policy supports the psychological safety of our workforce. Refer to woodside.com for our Code of Conduct and Working Respectfully Policy. Our We Care value, guides us to keep each other safe and care for communities. We prioritise safety and promote a positive safety culture by encouraging everyone to speak up and intervene on safety issues. We acknowledge providing energy to the world in the form of oil, gas and new energy potentially presents safety risks. We aim to control or mitigate the potential impacts of these risks on people, the economy and the environment. Our Health and Safety Policy outlines the objectives and principles that shape our approach. This approach is consistent across all our business operations. When assessing safety risks, we consider the potential negative impacts of our business activities to communities and our workforce, including impacts on human rights. We implement systems and processes to identify, assess and control safety risks by applying the hierarchy of controls. Our expectations and procedures set mandatory requirements for managing high-risk work, including obligations to stop unsafe work to prevent potential fatalities and high-consequence injuries. We take action to protect the health of our workforce and facilitate earliest recovery from work-related injury or illness. We aim to eliminate or mitigate workplace health hazards at the design stage of projects or control them as far as reasonably practicable based on the level of assessed risk. If hazards remain and there is a risk of exposure, we strive to ensure that worker exposure does not exceed legal limits through implementation of the hierarchy of controls method. WOODSIDE ENERGY GROUP LTD 35

我們根據適用法律進行健康監測,以發現職業病的早期跡象,因此可以進行幹預, 必要時,可以啟動康復。潛在有害的工作場所健康危害包括不受控制地暴露於噪聲、有害物質(例如苯、甲苯、乙苯和二甲苯(BTEX)和汞)、天然存在的 放射性物質(NORM)、傳染病(例如, COVID-19), hazardous manual tasks and psychological hazards. Refer to woodside.com for additional information about our approach to Health, safety and wellbeing. Our performance A fatality of our colleague on the NRC occurred in June 2023. Three additional high-consequence injuries were also recorded for 2023. Two musculoskeletal injuries that required surgery with extended recovery beyond six months and partial amputation of a thumb following a crush injury. Following insights from event investigations, we are focusing on field leadership and engagement, risk assessments and equipment management processes. In 2023, Woodside experienced two Tier 1 and one Tier 2 loss of primary containment (LOPC) process safety events (PSE). All events were investigated, and actions were put in place to address the root causes, including preventative actions across our facilities. We are also embedding lessons learned relating to equipment selection and maintenance. The workforce exposure hours in 2023 (total hours 20,914,483) increased by 25%, when compared to 2022 (total hours 16,699,730). The increase in exposure hours in 2023 was due to increasing project activity and merger integration. Our total recordable injury rate (TRIR) of 1.86 increased with 39 recordable injuries in 2023, compared to 30 in 2022. The main injury types were lacerations, wounds and soft tissue injuries. Our total recordable occupational illness frequency (TROIF) increased to 1.15 per million hours worked from 0.72 in 2022. The 24 recordable occupational illnesses comprised 12 noise induced hearing loss, five psychological illnesses, four musculoskeletal conditions and three skin reactions. Process safety We recognise the critical importance of effective Process Safety Management (PSM) to avoid major accident and environmental events due to loss of control of hazardous substances. We continue to focus on process safety leadership to ensure consistent awareness of contemporary PSM approaches, organisational status, personal expectations, and accountabilities. In 2023, we rationalised and improved our competency curriculum and continued with regular assessment and assurance of process safety critical roles across global operations. Future focus areas include continuing our efforts to embed a strong process safety culture, building competency across our hydrocarbon business and increasing process safety applications in our new energy and carbon business areas. In 2024, we are targeting a 95% company-wide completion of competency assessments for people in process safety critical roles requiring a skilled (advanced) level of competency. Field Leadership Program Woodsides Field Leadership Program provides a structured approach to work team engagement, where leaders build their understanding of onsite work practices and develop the leadership skills that aim to lead to a safer workplace. The program has been designed to be applied at all worksite types from operating assets to the office environment. A key objective is to learn from frontline workers which is aligned with Our Values and Human Organisational Performance (HOP) principles. Outcomes from the program include increased organisational knowledge of risks and controls, a sustainable method to identify and improve organisational factors, and to further develop our culture of care. In 2023, the Field Leadership Program framework was tested with operational groups. This required extensive workforce engagement to listen and learn from current approaches to HSE and work management so that the program can be tailored to enable a safer Woodside. In 2024, the program will evolve by listening and supporting end users through training and coaching activities. We aim to develop and implement a strategy to rollout and sustain the program across our global sites. Mental health and wellbeing Our wellbeing vision is to be recognised as an employer of choice. We aim to cultivate a work environment where everyone can flourish by focusing on people, empowerment, and quality leadership. To achieve this, we have expanded and refreshed our Global Wellbeing Framework to focus on six key elements: (1) protecting from harm, (2) promoting health and wellbeing, (3) connection and community, (4) work-life balance, (5) opportunities for growth, and (6) meaning and purpose. Each element has a strategic goal, enabling activities and metrics to track progress, including the use of our employee survey to seek regular feedback from our people. In 2024, we plan to launch our refreshed wellbeing framework across our global business areas, and work with our leaders to commence enabling activities. 36 ANNUAL REPORT 2023

環境和生物多樣性伍德賽德認識到管理和保護環境和生物多樣性的重要性,以支持我們活躍的社區的可持續發展。我們承諾盡我們的一份力量。我們理解並接受我們的責任,以環境可持續的方式開展活動,積極促進 生物多樣性並幫助扭轉生物多樣性的喪失。亮點:無碳氫化合物泄漏或危險 non-hydrocarbon spills greater than 1 bbl. In 2023, obtained secondary approvals for construction-related environment plans for the Scarborough Energy project. We supported a number of scientific programs and industry working groups to further our knowledge and understanding on noise-related issues and offshore whale species. Through these programs, bespoke underwater noise controls were developed to avoid and minimise marine noise impacts for offshore projects. A consultation approach for Environment Plans in Australia which has successfully addressed evolving regulatory requirements was developed. Invested in science and biodiversity programs and conservation partnerships to support improved knowledge outcomes. Established Woodsides Biodiversity Positive Program framework. In 2023, Woodside planted approximately 2.7 million mixed biodiverse seedlings across approximately 4,700 hectares of land at Woodside owned properties. These activities bring the total number of hectares planted to approximately 10,000 hectares since the Native Reforestation Project began in 2020. Potential Integrating the Environment and Biodiversity Policy into environmental management decision-making opportunities processes. Assess biodiversity positive opportunities for individual Woodside assets. Begin to invest in biodiversity positive projects in the regions where we are active. Continue to collect knowledge on environmental and biodiversity benefits of in-situ decommissioning. Ongoing development of technology to identify the seasonality of offshore cetaceans and further manage our underwater noise impacts. Potential risks Increased regulatory landscape and stakeholder expectations leading to extended timeframes for assessment and complexity of environmental approvals. Failure to progress biodiversity positive outcomes in a timely manner in the regions and areas where we operate. Potential incident resulting in significant loss of hydrocarbon to the environment. See also section 3.9Risk factors. Our approach The nature of our operations are accompanied by certain environmental impacts and risks. We work to minimise our impacts by integrating environmental management into our activities, including the design, construction, operation and decommissioning of our facilities. We continue this integration by reviewing our processes and commitments, identifying areas of strength to build on and look to embed renewed environmental standards across Woodside and set appropriate targets and metrics against these. Our focus on implementing leading environmental management and mitigation strategies has allowed us to avoid and minimise our environmental impacts and maintain a more than 30 year record of oil and gas operations without any major environmental incidents. We recognise that it is not just how we approach environmental management, such as the use of a risk-based assessment which matters, but that we also need to be clear and transparent. We engage with our stakeholders to better understand the possible impacts of our activities and to further understand preferred methods and frequency of engagement. Our hydrocarbon spill preparedness and response framework continues to be a focus across the companys global portfolio. The approach is underpinned by a comprehensive process informed by international best practice conventions. These require all activities to assess credible spill scenarios to marine environment, evaluate surface and subsea response options and recommend appropriate response techniques. These activity specific plans are supplemented by corporate plans, regional equipment, and locally trained resources. Environmental management We recognise our activities have an environmental footprint and we seek to avoid or minimise adverse environmental impacts to the natural environment in the regions we operate. We do this by adopting a risk based approach that allows us to address the environmental impacts and risks associated with our activities in a consistent way. It allows us to focus our effort and resources on the most significant risks associated with our activities no matter where we operate or what a regulatory regime may require. WOODSIDE ENERGY GROUP LTD 37

我們的表現我們的營運及增長策略取決於取得及維持我們的社會營運許可。考慮到這一點,以及 我們自然環境面臨的壓力越來越大,環境績效和環境影響的管理對我們業務的未來成功至關重要。2023年,未發生涉及碳氫化合物或 危險的環境事件 釋放到環境中的非碳氫化合物泄漏超過1桶。作為我們減少影響和風險的承諾的一部分,我們的碳氫化合物泄漏準備和響應框架嵌入了我們的全球活動和運營組合。這使我們的業務能夠根據我們的環境方法來規劃和評估對海洋環境的泄漏風險。2023年,我們制定了新的石油污染應急計劃 ,幫助監管部門接受了我們澳大利亞資產的11項環境審批。我們還為我們運營的地區提供能力和培訓計劃。我們將繼續與地區和國際行業組織合作,以協助主動管理和監控新出現的風險。自2023年以來,伍德賽德一直致力於支持我們所在地區的積極生物多樣性成果。我們的方法建立在現有的生物多樣性積極項目的基礎上,這些項目始於2023年前。伍德賽德在2023年開發了一個框架,以評估和實施未來的項目。伍德賽德尋求支持具有可衡量的生物多樣性結果的生物多樣性積極項目,這些項目加強了利益相關者的參與並充分管理風險。我們繼續投資於科學,以支持我們全球投資組合中更好的環境績效和成果。我們還在澳大利亞、特立尼達和多巴哥、美國、墨西哥和塞內加爾繼續推進我們的環境監管授權,以推進我們的項目。見第3.7節:新能源和碳解決方案。原住民文化遺產和參與我們承認原住民社區與土地、水域和環境之間的獨特聯繫。我們相信原住民文化遺產和工業可以成功共存。我們尋求確保傳統所有者和保管人是遺產管理的核心,以便了解並繼續保護文化價值。我們明白識別那些與我們存在的土地和水域有長期文化和精神聯繫的人並與他們合作的重要性,我們在他們的指導下努力避免或最大限度地減少我們的行動對這些原住民社區的潛在影響。我們與原住民社區合作,創造積極的成果,留下持久的遺產。我們承認我們所在地區的第一批國家社區的多樣性。在與廣泛的聽眾交流時,伍德賽德交替使用土著和第一民族這兩個詞。在地方層面上,伍德賽德將接受社區的指導,以確定適當的職權範圍。重點介紹了 就文化遺產管理審批進行的廣泛磋商。在新西蘭與與南方綠色氫氣項目相關的Ngāi Tahu iwi的關係取得進展, 繼續側重於加強利益攸關方關係。為與第一民族利益攸關方就批准環境計劃進行協商提供支助。繼續致力於支持Murujuga的水下遺產研究,為項目實施和管理可能產生的影響提供信息。原住民諮詢小組圓桌討論會。潛在的 可能會在現有的和解行動計劃目標之外採取其他舉措。Opportunities 進一步 在我們活躍的地區與原住民社區發展關係。在我們活躍的領域尋求和正規化第一民族夥伴關係。 -Woodside的潛在風險會對Murujuga巖石藝術造成負面影響。伍德賽德沒有滿足原住民社區的當地內容結果。伍德賽德在我們活躍的地區沒有達到原住民社區的期望。另見第3.9節:風險因素。我們的方法我們的原住民社區政策定義了我們的方法,並根據需要定期審查和更新。伍德賽德員工、承包商和在伍德賽德S運營控制下從事活動的合資夥伴共同負責政策的應用,並接受培訓以確保他們能夠做到這一點。政策指出,伍德賽德將遵循《聯合國土著人民權利宣言》,該宣言表明我們致力於在與不同的原住民社區接觸時理解相關的人權考慮。38年報2023年

In Australia, we maintain relationships with First Nations communities in the Pilbara, Kimberley, South West and Perth. Due to recent changes to regulatory compliance requirements our approach to consultation has been extended. In 2023, Woodsides First Nations relations team consulted with a range of First Nations communities, in Australia, from Esperance to the Tiwi Islands and as far east as Melbourne. The diversity of the environments we are operating in as a global company has expanded our engagements with a range of community stakeholders in the United States, Mexico, Trinidad and Tobago, and New Zealand. Refer to woodside.com for our First Nations Community Policy. Our performance In 2023, new relationships were formed and new land use and relationship agreements were executed. Woodside remains committed to close consultation with the relevant persons in the areas in which we operate by way of community and individual meetings, attending community-initiated events, and ensuring accessibility for feedback or questions as needed. A key element of our consultation efforts is our willingness to be flexible and adaptable in our consultation format to suit the audience. Cultural heritage Woodsides Cultural Heritage Management Procedure reflects our publicly available First Nations Communities Policy. This policy includes engaging with affected communities of First Nations peoples in ways that are consistent with the principles of seeking Free, Prior and Informed Consent (FPIC). Our approach to the identification, management and protection of tangible and intangible cultural heritage seeks to avoid impacts, or if avoidance is not possible, to minimise and mitigate those impacts. We seek to ensure Traditional Owners and Custodians are central to heritage management so that cultural values are understood and remain protected. Woodside also prepares detailed Cultural Heritage Management Plans (CHMPs) for nearshore and onshore facilities and projects and completes heritage audits and surveys with Traditional Custodians and independent heritage experts. Woodside is also committed to ensuring our management of cultural heritage is thorough, transparent and underpinned by consultation and continued engagement with First Nations communities, which is illustrated through our extensive consultation on our Environment Plans, completed heritage surveys for the proposed Woodside Solar project, and support for Murujugas World Heritage Listing. Cultural heritage management approvals Woodsides activities are the subject of environmental assessments by a range of regulators including the Australian National Offshore Petroleum Safety and Environmental Management Authority. Woodside has consulted extensively with Indigenous stakeholders on a variety of activities in 2023. These consultations have included the tangible and intangible cultural heritage of the environments in which we plan to operate, as well as the environmental values. In 2023, we also agreed the Scarborough Cultural Heritage Management Plan with Murujuga Aboriginal Corporation (MAC), which is publicly available on our website at woodside.com. The CHMP is designed to ensure that impacts to heritage sites and values, including to Murujugas National Heritage Listed and World Tentative Heritage Listed values, are adequately protected in a manner agreed between Woodside and Traditional Owners and Custodians represented through MAC. It aims to preserve the tangible and intangible heritage values and protect the cultural and spiritual values of the Traditional Owners and Custodians. Woodside is also progressing the agreement of a CHMP with Ngarluma Aboriginal Corporation for the development of a proposed solar photovoltaic farm on the Maitland Strategic Industrial Estate. Our continued commitment to reconciliation Woodside has been part of Reconciliation Australias Reconciliation Action Plan (RAP) program since 2009. Woodsides vision for reconciliation is to partner with Indigenous communities to create positive economic, social and cultural outcomes. It is also to reflect on our shared history, empower Indigenous voices to speak and be heard so all Australians can learn, and work together towards a better, shared future. We are continuing to move away from recording completed activities, in favour of measuring longer-term impact outcomes. Woodside reports annually on progress towards the committed outcomes that support our four Reconciliation Action Plan pillars: respect for culture and heritage, capability and capacity, economic participation and stronger communities. In 2023, Woodside made donations to the Aboriginal and Torres Strait Islander Voice Referendum activities that were aligned with Our Values, the principles set out within our 2021-2025 Reconciliation Action Plan and our First Nations Communities Policy. Our donations supported organisations to disseminate information and advocate in favour of formalising a pathway for Indigenous Australians to share their views on policies that impact them. Woodsides contribution aligns with our support for the Uluru Statement from the Heart, which called for the establishment of an Indigenous voice to Parliament, agreement making and truth-telling. For further information, please see the Corporate Governance Statement included in this report and the Sustainability section of our website at woodside.com. WOODSIDE ENERGY GROUP LTD 39

3.9我們的業務風險因素伍德賽德認識到,承擔風險對我們的業務是必要的,有效地管理風險對於實現我們的目標至關重要。我們致力於以積極、知情和有效的方式管理風險,以此作為競爭優勢的來源。我們的方法旨在實現風險知情決策,這將保護我們免受 潛在的負面影響,並使我們能夠尋找正確的機會。我們風險管理框架的目標是提供整個公司風險的單一綜合視圖,以瞭解我們的全面風險敞口,並確定風險管理和治理的優先順序。有關我們風險管理流程的更多信息,請參閲我們網站Wood side.com上的風險管理政策。伍德賽德和S的風險管理流程是一個迭代序列,我們 以協調的方式進行。該流程幫助我們實施風險管理,以有效地識別、評估和控制風險,從而提高實現目標的可能性。這一過程包括:與關鍵利益攸關方進行溝通和 協商,以確定風險範圍、背景和標準,進行風險評估,進行風險處理,監測和審查風險管理流程;以及記錄和報告風險。該流程在我們的風險管理程序中進行了定義,旨在為識別、管理和報告可能對伍德賽德和S的業務目標實現產生重大影響的風險提供一致的流程。審計與風險委員會在使董事會能夠履行與伍德賽德S風險管理相關的監督責任方面發揮着至關重要的作用。可持續發展委員會還關注與可持續發展相關的風險管理。 有關審計與風險委員會和可持續發展委員會的更多信息,請參閲第4.1.3節董事會委員會。我們將風險分為三類:1.戰略風險:可能影響我們組織S實現戰略目標的能力的風險。2.實體風險可能影響我們組織S實現業務目標的能力的風險。它們可以是積極的,也可以是消極的,也可以兩者兼而有之;它們可以應對、創造或導致機會和威脅 。3.新出現的風險定義為由於快速或快速的風險而具有高度不確定性的外部威脅或機會非線性演化。它們有可能對戰略目標的實現產生重大影響。伍德賽德和S的風險偏好聲明是我們風險框架的重要組成部分。2023年,該聲明進行了更新,以反映合併後的組織S承擔風險的意願和對結果的寬容。 聲明旨在使我們的組織能夠在瞭解風險的情況下做出決策。40年報2023年

我們的風險因素概述氣候變化全球應對氣候變化正在改變世界生產和消費能源的方式 。氣候變化的複雜和普遍性質意味着轉型風險與其他風險相互關聯,並可能放大其他風險。此外,潛在的社會應對氣候變化的內在不確定性可能會給全球經濟造成系統性風險。氣候變化還可能造成重大的物理風險,例如風暴、野火、洪水和其他氣候事件的頻率和嚴重性增加,以及温度和降水模式的長期變化 。這一因素與伍德賽德有何關聯?伍德賽德S與氣候變化和向低碳經濟轉型相關的風險包括對石油、天然氣及其替代品需求(和定價)的可能影響,其勘探、開發和生產的政策和法律環境,以及伍德賽德S的聲譽和經營環境。我們還可能面臨與氣候變化相關的風險,S可能會對我們的資產或供應鏈造成有形損害或中斷。伍德賽德是一家能源公司,為了滿足我們的客户和我們所在社區的持續需求,我們必須瞭解、預測和管理幾個關鍵風險,才能在這種過渡中發展和繁榮。這些要素包括:*石油、天然氣、新能源產品和低碳服務的需求和定價;石油和天然氣勘探、生產和消費的監管;全球向低碳經濟過渡的時間和速度;公眾對伍德賽德和更廣泛的石油和天然氣行業獲得碳信用或排放限額的機會和價值的看法;以及與天氣模式變化相關的不確定性。 此因素可能如何影響伍德賽德對我們的資產或我們的供應商、客户的資產、 的可用性和排放額度或碳信用的成本的影響的示例可能會或社區因嚴重 影響的頻率或強度增加而造成 伍德賽德S有能力滿足其2025年和2030年淨資產範圍內的天氣事件。 1和2的減排目標。在我們的供應和全球需求之間,過度或過少地投資於石油和天然氣儲備,導致了 失衡,以及其他組織未能達到整個行業的排放目標。 更廣泛的石油和天然氣行業。未能以符合全球 的速度過渡到新能源、伍德賽德或石油和天然氣行業需求方面的聲譽風險、或利益相關者情緒,或總體上開發和實施 。伍德賽德的S戰略可能依賴的低碳技術。 面臨金融風險,包括資金可獲得性的限制、氣候驅動的石油和天然氣項目立法、法規和政策或 融資條款的變化,或者獲得資本的能力 與氣候相關的訴訟導致額外成本,防止或 市場。限制伍德賽德開展活動並對 伍德賽德S的聲譽造成不利影響。 這些影響可能會導致股東價值損失、市場份額被競爭對手搶走、我們的運營延遲或停頓、為資本項目提供資金的能力降低、監管審批延遲或暫停、法律責任以及對伍德賽德S聲譽、社會經營許可證和我們戰略交付的不利影響。伍德賽德如何管理這些風險? 伍德賽德正在努力實現其淨股本範圍1和2温室氣體排放 我們參與並倡導關鍵的行業和治理氣體減排目標,並對產品和 利益相關者進行投資。我們的氣候轉型行動計劃和2023年能源轉型進展服務。這包括石油、天然氣、新能源 報告包括有關伍德賽德S產品和低碳服務方法的進一步信息。1 管理氣候變化風險。有關這一主題的更多信息,請參考伍德賽德網站和氣候轉型行動計劃和2023年進展報告。1個目標和期望是淨權益範圍1和2温室氣體排放量相對於6.32公噸CO的起始基數-e代表2016-2020年温室氣體排放總量年度平均權益範圍1和2和 ,可根據生產2或受制裁資產的潛在股本變化進行調整(向上或向下),並在2021年前作出最終投資決定。淨股本排放量包括利用碳信用作為補償。伍德賽德能源集團有限公司 41

Social licence to operate Risks associated with actual or perceived deviation from social or business expectations of ethical behaviour (including breaches of laws or regulations) and social responsibility (including environmental impact and community contribution), particularly as these expectations evolve and as Woodside expands its global operations. How is this factor relevant to Woodside? Woodside relies on maintaining healthy relationships with our numerous stakeholders in order for us to achieve our objectives. Our employees, host communities, Traditional Owners and Custodians, government authorities, investors and other groups form significant relationships with our organisation. These relationships are built on the trust that Woodside will meet our stakeholders expectations. We must also consider the role our commercial agreements play in relation to human rights around the world, as we have a responsibility to ensure the rights of all humans are not negatively affected by our organisation. Some of the most significant risks to our relationships with stakeholders include: Engaging in activities that have real or perceived adverse impacts on the environment, biodiversity, human rights or cultural heritage. Failing to meet our net equity Scope 1 and 2 emissions reduction targets or investment targets in new energy. Inadequately responding to quickly evolving expectations of Woodside (including expectations that may significantly differ in the various jurisdictions in which we operate). Additionally, third-party risks that are outside of our control could negatively impact our reputation and licence to operate, such as oil spills or other disasters or scandals that cause collateral damage to Woodsides licence to operate via reputational damage to the oil and gas industry at large. Failure to maintain healthy relationships with our various stakeholders may result in violation of local or national laws or regulations, significant reputational damage, delayed approvals, civil suits and ultimately the deterioration of our licence to operate. Examples of how this factor may impact Woodside Limited, delayed or failed approvals from local and national These impacts may lead to a loss in shareholder value, loss of market government bodies. share to competitors, decreases in the value of assets, delays or Lost or limited stakeholder support for our current business stoppages in our operations or infringements on our ability to execute and future opportunities. and complete transactions, reduced capacity to fund capital projects, Risks related to class action lawsuits, litigation and activism, delayed or suspended regulatory approvals, legal liabilities and adverse including allegations of greenwashing. impacts on Woodsides reputation, social licence to operate and on the Reductions in the availability, or less favourable terms, of financing. delivery of our strategy. Decreased ability to attract and retain a talented workforce, and other operational concerns. How is Woodside managing these risks? Woodside proactively maintains and builds our social licence to operate Our fraud and corruption framework aims to prevent, detect and through the application of our values, effective stakeholder engagement respond to unethical behaviour. It incorporates policies, standards, strategies, our regulatory compliance framework and our anti-fraud and guidelines and training, which will enable us to conduct our activities corruption program. ethically and to a high standard. Our regulatory compliance framework assists Woodside to proactively Our business conduct is informed by the United Nations Guiding maintain relationships with governments and regulators within countries Principles on Business and Human Rights (UNGPs), which set a global that support base business and future growth opportunities. standard of conduct for all businesses wherever they operate. These principles exist over and above compliance with national laws and Woodside maintains meaningful relationships with stakeholders, regulations protecting human rights. seeking proactive engagement to inform decisions and gain support for changes. 1 Individual investment decisions are subject to Woodsides investment targets. Not guidance. Potentially includes both organic and inorganic investment 42 ANNUAL REPORT 2023