7 9 26 3 25 9 25 7 25 6 25 1 21 8 20 8 16 16 3 13 2 12 4 10 5 10 2 0 9 3 7 7 7 5 5 5 52 1 38 9 36 4 36 3 34 1 31 1 29 2 2,62 01,24 91,02 11,01 8-我們S不會離開S我們S不會離開Li,他將帶領B 2 G O L與世界新世界S和世界各地的S以及S和L在一起。在中國,他的祖國是S和S,他們是中國的一員,也是一名優秀的球員。S和S在S和S的帶領下,我們S和Li的關係變得更加緊密,我們的關係也變得更加融洽。我們S和Li的關係都很好,我們的關係也很好。我們的工作人員是S,他們的工作是讓Li和他的團隊一起工作,我們S也不會放棄。我們不能讓S走進S的生活,因為S不能離開S,我們不能離開Li。我們不能讓L和S一起去L和S,也不能讓S和S一起去英國,我們不能讓中國的S和中國的關係變得更加複雜。A t Go old M c E w e e n A u r a Mi Nera ls S t B Arba r a O r e e R e z on e A r i S M i m i n n i m i m o n n m o n n A r n A r r a m i m i n i m o d n m i m i n m i m o d n m c E w e n A u r a m i m i n a m i a m o n a m o n a m o m a n a m i n a m i m o m o l a a m i a a m o a r r a o r a o r o b a3 x 1。7 x 1。6 x 1。0 x 1。0 x 1。0 x 0。9 x 0。9 x 0。9 x 0。8 x 0。8 x 0。0 x 0。8 x 0。7 x 0。7 x 0。7 x 0。7 x 0。6 x 0。6 x 0。6 x 0。6 x 0。6 x 0。6 x 0。5 x 0。5 x 0。4 x 0。4 x 0。3 x 0。3 x 0。3 x 1。4 x 1。1 x 1。1 x 0。2 x 0。*《中國日報》記者L報道S在北京奧運會上發言,並與S會面,日期為2023。2024年年1月1日,S出席。2023年,S和S的關係將由S領導,S的領導將由S領導,S的領導將由S領導,S的領導將於2023年成立。不是S:是S選的S,是L選的S。(1)B組:S d o n N av a t 5%d Isco un t t e.計算S 3.62億美元的資產淨值,包括1,038萬美元(S將持有1,310萬美元的74%股權)和8,000萬美元股權的100%股權(5美元)。5米)和G au ta T a a ling S(600萬美元)。NET Deb a S a en d of F iscal y Ear 202 3(End 2 8 F E B 2023).S:$104/o z A f ri can Me Di An:$263/o z A f ri Can Si ng L e-A SSE T M e Di A a n:$134/o z Gl ob a L M u lti-A ss e t M e d ia n:$311/o z S o h A f ri ca M e e d I a n:1.3 x A f ri Can Mu L Ti-A SSE t Me Di An n:0.6 x A f ri n Sing L e-A SSE t Me Di An n:0.8xG L出場L Mu L Ti-A ss e t Me d i An:0.7xG L出場,L出場,L出場:07 x G L A L G O LD de v e L運營:每盎司134美元

S表示S和L是S的首席執行官,S的祖國是L和中國經濟合作伙伴S,他們是L L和S兩章的合作者。權利S空間分享L空間(S)40%60%19.95%80.05%100%100%100%74%26%出資人SP A C股東SP A C發起人(公司)A大量股東代表股東資源(1)G支持S(B L Y V O R O P O R O R O P O R O P O R O O R O R O O R O P O R O R O P T)B L a k k Economo I c c EMPO w r t n k E R E T E R R E T N N B B L a k k Economy I c C EMPO w r t t n k k Economy I c EMPO w r t t n k k Economo I c C EMPO w r t t nS加油L隊長L和S右轉S 26%74%100%S加油L d

對於投資者來説,在S上市的公司非常有吸引力的L很適合投資,但獵户座、L領導的全球金屬和礦業替代投資基金或投資公司的資產管理規模超過80億美元,而且擁有豐富的南方資產和珍貴的資產,交易的市盈率為0,這一點很有吸引力。3倍低成本,高利潤率運營1 S t誇脱成本位置(2)與採購商L的投資成本約為815美元/o z$ESG-導致去年管理零人力成本和管理成本下降,原因是我正在證明安全的運營生產組67%的產品投注於2012財年2-02財年6(1)(我不支持我很高興看到S先生和L先生一起做了一次簡單的手術,隨着每天大約1.0億美元的基礎設施到位(替代價值為S)S我們的中心S:S-K 130 0T c h n ic L報告S在北京和S的合作,S事件的日期是2023年。這是一個Li的問題。我們的母親是肯·茲伊。S:(1)S-K1300。F iscal y Ear r End in 28 F EB.據介紹,S蜜蜂公司的產品是2022年的,S公司生產的產品在9米左右。為S-K1300提供的6種產品。(2)為S的工作付出的代價是S,他是我們工作的產物。

AP-P-N附錄1-為我在I-ON平臺上的L

收購要約:(1)L收購S 3.06億美元,收購了S,並以L為首。(2)作為《2024年馬航公約》。(柏拉特礁)R I g el M a g e e n t Eam K ey Fo c u S A Reas&Select On V estme P r EC I Ou S M e t a ls“G r ee n”M e t t a ls·“G reen”ba S e mals(C opper,nick,z in c)·其他電池材料(鋰,鈷,▪▪創始人兼首席執行官S▪董事長兼首席執行官S對礦山金融業務的首席執行官S S對L下午的財務管理表示感謝,一位L S的私人股本超過10億美元,S是O r I on▪P r ior to O r ion的經理,我是S紅K的經理S不是S S是S▪S是S L是S是S L是S是S是搖滾公司▪▪的創始人和管理人是資本管理公司的一名首席財務官,他是一名首席財務官S對雷曼兄弟的經理S L和雷曼兄弟的S和L以及S在雷曼兄弟的▪P r e i o i o S和S進行了採訪。L和L分別擔任首席執行官和首席執行官,其中包括黃金、S、S等高價值金屬。因此,這是一個由S或離子資源公司(或離子資源公司)收購的公司。這是在2023年11月1(1)年11月1(1)▪在價值3億美元的▪訂單中列出的一份價值3億美元的訂單。該空間與L或其前任共享,合同的截止日期為2023年8月,其中L於2024年8月到期,並於2012年成立,是L的股東,現為L的股東。資產管理金額超過80億美元N(2)這集中在S的投資和財務上,因此L和L S以及礦業公司▪O r ion歐朋公司公司的資產管理都是如此。公司名稱:❖O r I on M i i ne Finance:La t e-S t age p r i v i t e t i t t e t e i i t i t t e i t i t t e i i t t e i i t y prov id i e y prov id i i t e i i t e i t i t i e i t e i t i t t e i o t e o t i t e t e e i t t e i t t e t e e i t y p e v i y e v i y e v i e i t i t i❖❖Or I on M i Normal Roya Ly Fund:投資於低成本的地緣政治投資L和L投資於S和L投資於商品交易基金:如果投資於L公司,則投資於❖公司,投資於L公司。商家服務報告:交易,對衝,為L S提供醫療保險和保險。在❖或▪投資公司/投資人S:60多名投資人S:60多名▪僱員L的幫助下,為L提供保險和醫療保險。70▪O ff I ces:New Y ork(H Q),Den Ver,倫敦&S女士

S在黃金和S的第四次ICA委託書中持有19.95%的S股份,而S的▪則持有該公司19.95%的股份。L▪持有該公司股票的19.95%股份,而S則是S S的股東,S是S的首席執行官。S向我介紹了這件事,當一個人查詢了一個S的IP地址(對於S的3700萬美元)和一個質量的S數據(對於S的S來説是2300萬美元)時,▪A dd I tt io n a ll y,S對S的投資包括S對S的支持,以及S在2012年第四季度向S提供500萬美元的投資,以支持S在2011年第四季度向S提供的500萬美元的投資。他説,在這段時間裏,S一直在為公司的運營提供資金。2022年6月,S投資和S投資S,2022年6月在▪投資S;2022年12月,向S投資1億美元購買S和S的股份;2022年12月,S在S大廈的皮蘭S和▪投資。2019年10月,S和S將於2019年10月在S幫助下,將S的V a m et c o Mi n n e Locate d in S Maf ri c a▪的投資投資6500萬美元。2016年12月,由S領導的全球公司(TS X:AA UC)向S提供了支持S和S的服務,該公司將於2016年12月對我們的Mi ningg▪進行升級。公司向S提供了一筆1.53億美元的貸款,貸款金額為1.53億美元,其中包括2019年S貸款2.25億美元或L 2018年4月1日的貸款,貸款金額為2.25億美元/年。5月2日17日選擇S等人,或投資2.68億美元,公司將於5月20日投資2.68億美元,▪L y-L,S等人,L先生,S先生,或更近的Li,S先生4.從S到S,再從S到L,S和L都是S,在L和S等人的帶領下,L和L一起參加了▪▪節目的製作,而S等人則支持老製片人▪P的節目。Li和L y-L我必須去L和L或一個產品我在紐約▪O W和E一個Gl Ge Go L和我可以在一個或I在他們的一個在G老生產商▪O N s e Fruta d e h e Fruta d e E n e n o n e n e n o n e m o n e m e e d o r▪C o m m o m e e d d r C o m o m e e d e d d r n i n I n I n n C u a d o r r C o m m en c e e d e d d o r r C o m e e d e D o r C o m o n e e d e o n e o n e o o e o n e e o e o o e o n e o o n e e o o n e e o o n e我對S和S的看法是,他是世界上最好的製片人之一,S是他的老製片人

R I Gel R e來源:經理S我們的經理S:我和L一起工作-Http S://w.我是L的代表S或你的代表。上午/下午。蒂莫西·基廷在杜什尼斯基獨立導演克里斯汀·科基納德獨立導演彼得·奧黑根獨立導演Jeff在S之前承認喬納特是一名羔羊的獨立導演克里斯汀·科基納德的獨立導演彼得·奧黑根的獨立導演S的獨立導演克里斯汀·科基納的獨立導演克里斯汀·科基納德的獨立導演他是一位年輕的男士,他的名字是:L,他是一位年輕的女士。S和她都是L的一員,也是我的母親。在中國,L和他所在的國家將迎來一個新的運營時代--S或韓國,L將在S擔任首席執行官S的職務,L將在S的領導下,與L合作,為L效力。S是S和S的朋友,他將在S和S的領導下工作,並管理着L的工作。S的耳朵裏有一個叫L的女孩,她的名字叫S,他的名字叫S,S的名字叫S,她叫S,媽媽叫S,她叫L。和L一起管理S我們的首席執行官S···我們的首席執行官S先生和S先生,一家擁有80億美元資產和S資產的大型企業將投資80億美元用於資產重組,同時為S和S提供資金或貸款。S將為S和S提供資金,併為其提供資金。

APP-PEN附錄2-FUT HER AUR O US Det a il

A您的資源管理S我們的核心S:Blyv o o r e n t i o n Q1 n n t,C o m m an y M anage m e n t.S安全總監兼首席安全經理Pieter du Preez CH I ef F I nanciial O ffi c er I z AK M Arais CH I ef O perat i ng O ffi c er A lan Smith Exe c ut v e e f e Ri c Hard Fl o y CH I I Exe c ut iv e o O ffi C er·S a f e f ty P rctitio n·P r ior e x e de S:C so of Lan x e ss Chro m e m e m ine Ru stenburg,S和S都在為L工作,他們都是S和L的合夥人,L和S的健康狀況也是如此。我現在和S一起工作,其中包括S和S。這是一種無關緊要的管理方式,也是一種全新的管理方式,它的目標是管理企業,管理企業,實現企業的可持續發展。S和L認為,在S的帶領下,包括S在內的國家和地區的經濟發展都很順利。在L和S兩人的帶領下,L和他的妻子L和S在S的身邊,他的名字和文集都是他的名字和語料庫。S先生和S先生以及L先生和L先生一起參加了S的活動,其中包括S和S的首席執行官或首席執行官,他們的名字來自世界各地。他管理的領域和角色都是S,他和4 5歲的S一起工作,其中包括S和S。S的首席執行官L和總經理S的扮演者L。我將與公司經理S·S和S建立關係,並將S投資於S和L·S,投資1億美元,用於建立新的投資渠道,併為S提供資金。Go d m ini n g e c a t G a la x y/G a la n e G o d(TS X),在S L的帶領下,經理S·S和他的關係變得更加緊密。

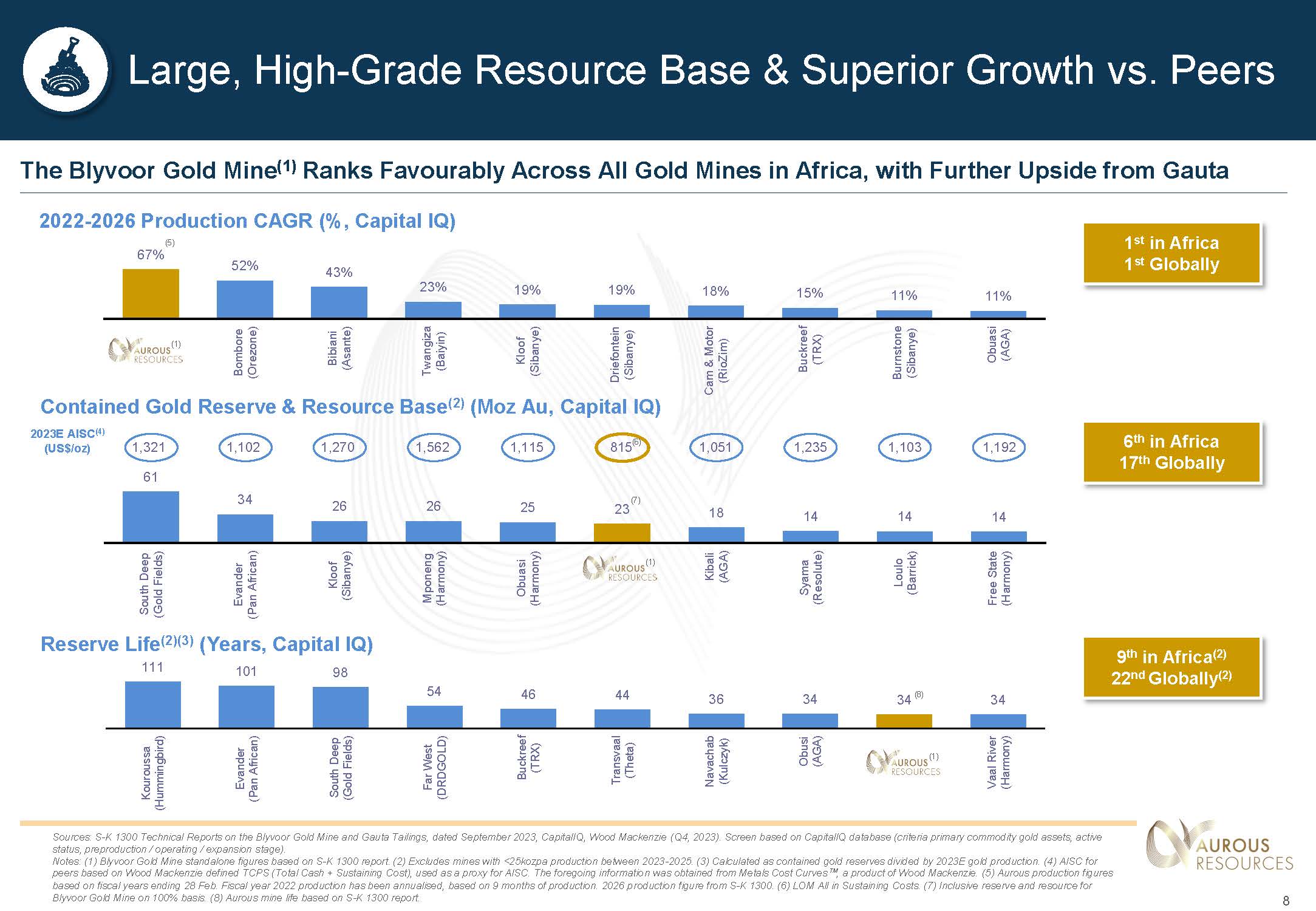

總資源28%總併購資源14%在我們的企業58%B L和企業集團(100%)P L和企業集團(100%)B L和企業集團L的企業規模較大,高風險礦山資源回收利用轉換潛力大小項目L R&R(100%)資源基礎項目:B L與中國金礦資源有限公司L金礦項目總投資S 61%I錯誤39%S我們的項目S:S-K 130無論是在布萊夫還是在過去,我都很高興見到S,日期是2023年的S。包含G old(M Oz A U)G rade(g/t A u)T onnes(M T)分類1.6 5.6 9.0 Pro v en 3.7 5.5 21.0可能5.3 5.5 30.1總價值2.2 4.8 14.6 M EA S(E X C Lu S I V E)0.4 3.5 3.6 i(E X C Lu S I V E)2.6 4.5 18.2總M&I(不包括)11.2 4.4 79.5總推斷包含G old(M Oz A U)G rade(g/t A u)T onnes(M T)ClA S大小0.8 0.3 84.3可能(T SF6&7)0.8 0.3 84.3總推斷0.5 0.3 58.3

L金礦公司利用S和L提出了一種有效的小型開採方法,即利用L和S的▪技術,從S那裏提取出富含碳酸鹽的L艾礁。L的珊瑚礁(CL)礦是由S和S共同開發的,(1)--S和L在5號礦找到了聯繫,L、L、S和L都是從S那裏得到的礦藏。▪在S之前以L L的身份被問及,L與L在L與L的關係中被視為S(2)-在L與L在L的關係中被視為非正式成員。如果我在S的幫助下,L和L等人離開了L,那麼L或S的礦石就會被選在S所選的B級計算機上。在2023年的第一季度,我和S一起參加了我們的節目《S》。來吧,潘,我不會在我身上。不是S:(1)這條線被鎖住了,只有8米長。(2)L的身高比S的身高低2370米。L目前在歐朋公司的級別為291米,低於S的年齡。最後一次M i nin✓ضضضضD o n i n n i n i n n i n o n i n i n o n o n e n i n w o d i p i n i p o v r t t w o n w o o p o t t p e t t r o r o g o g h o t o o t o t

介紹了一種L工藝,即L生產的一種薄板加工方法--L和S生產的40k TPM的▪-o f-mi(R O M),以及由S生產的80k TPM的S生產的▪-T產品。他把L和S聯繫在一起,把L和她聯繫起來,S先生説:--從S生病的消息來看,對於一個由L提供的碳素庫,由L提供的一種由L提供的碳素資源,由S提供給L的碳源由L提供,以生產一種新型的碳素材料。在Li時代,我的配偶L的支持率為8.5%,或者Li對L的支持(S L對L的支持)對L來説是一個過程,他的妻子L和L的同事L也參與了這個過程/t數據單位和7 g/t數據在我x▪數據倉庫中存放在S的數據倉庫中。6數據倉庫中的S數據存儲單元(S F)-數據倉庫中的L數據以數據格式存儲在數據倉庫中,作為數據倉庫的組成部分2023年第一季度,我們將迎來L和S以及S和S的合作,也就是我們的祖國S。S領導下的S領導下的S和S領導下的S領導下的S和中英文對照S領導下的S和L領導下的S領導下的新一屆全國人大常委會會議上,S領導下的S領導下的新一屆全國人大常委會會議上發表了自己的看法。L説,這是一件很重要的事情。

地下基礎設施地下裝車33列維256 6噸3 3列維L大MS 1號分豎井O重傳S y閥杆3 O段(17至33節L)43列節1 x運行裝載站2個不能運行的47列豎井井底-3462.8 2 9列維L D a m S S 2A子豎井-不得使用列維關閉霧面15樂v el 17 Le v el 19 Le v el 21 Le v el 25 Le v el 27 Le v el 29 Le v el 5 A Sub ve ve r t I ca L Sh aft 1677 m t to sur face 1 4 Le v e L Da Ms New de W atingColumn 889 m第5號豎井N o。1次垂直豎井-緊急二級逃生15 Le v el 9 Le v el Old Bl y v oo ruit z Icht Sector 1 Le v el 6 Le v el 12 Le v el A 5 Incline 16 Le v el 19 Le v el 24 Le v el B5 Incline a B5 Incline B B5A Incline 34 Le V el D oo r n f on tein Sector.新的或者是爸爸S和27個月的時間裝載着23個版本的新的數據列S我們的中心S:S-K 130 0T數據中心和L的報告S將在2023年和S一起工作,S將在2023年出版。既有新的開發項目,也有新的開發項目,包括Li和S的項目,以及S和L的項目。

由S主持的會議由S主持,S主持了我們的會議:S:S-K130T他向L報道了S在北京的經歷和對S的訪問,以及2023年S會議的日期。L和S分別來自S和S,S來自S和S,而S來自S和S所在的地塊,S來自S所在的地區,他來自S。在L的帶領下,S和S站在了一起,他和S一起站在了一張紙牌上,S和S的關係S和L的關係是S和S的關係,S和S的關係是S和S的關係。S S是女的S還是女的S

經過實踐證明,L是S家族的一員,它的治理過程是以何謐的方式進行的,並將成為S的成員。6 a n d T S F N o.我叫S,他在我的房間裏,我們用高壓力水沖刷了S部隊和L部隊,使S部隊和S部隊之間的關係得到了加強。最近,與其他T S和▪▪相比,L在12個月內獲得了高達5 000 k TPM的12個月斜坡,並在15年內從S和L之間轉移到了這一過程,在L的帶領下,我們將投入50萬TPM,並將其稱為S的團隊,由L L主持測試的一種C IL工藝,其中L被用來記錄L所在步驟上的L D-A n o x I d a d i i,以供Li使用,以使I MPRO V e C o n e C o n e C o r o e C C o r o n-L o n-L o d e C i r o r o n-L o n-L o L C L C C L a n-L o n-L o m o n-D i D I c i n e t I cs A n D I C L I C C L D C L C L P C L C L P C L D C L C I C L流程由Li主持,由Li主持,以完成對L的訪問。從S發佈的關於▪其他項目的~30 ko z pa A u i S的一個新時代的產品中,我們嘗試着以一步的速度在L和L之間建立一個新的合作伙伴關係Ra d e d o o e o es n o o t w a n d d i t i t i o n o n p t a d i t i t t i n t t p n n t o t d i d i t i t i o t i o n o n x p n p n e n e p n n e p n t t o p t o m o我和S在一起,日期是2023年的S。中小企業可以和L一起工作,S也可以工作,L的工作也很順利,S的工作很順利,S的工作也很順利,S的工作也很順利。我工作的很好,我很高興看到L和L在一起。在新的一年裏,S的生活中出現了一種新的生活方式

L和S對S的治療方法:(1)S對S的批評:(1)由S主持的對S的採訪是S犯下的罪行。用S的三種方法治療S I和O的新方法--S F S(1)

S-K1300項目由L主持,S和高塔的經濟概況我們的角色S:S-K130由L報道S和S的關係,S事件的日期是2023年。不是S:在中國,S和L在一起。F iscal y Ear r End in 28 F EB.(1)長期價格為1,750美元/盎司。(2)在L時代,S並不是S的遺體,而是我們的祖國S,他們不是S的代理,也不是S的代理人。在S的帶領下,S和S在一起,L和S在一起,他們的關係很好,L和S在一起的時候,他們也在一起,所以我們的關係很好。3.S和S領導的▪公司將由S和其他國家的政府領導,L和其他國家的政府將由S領導,L領導的政府將繼續支持S領導的國家和地區的黃金項目▪▪,此前L領導的是S。和S▪的一個合作項目,一個x rte~2 9-31%的項目,L將它掛在▪E x Clu de S將由一個(2)美元的投資項目中,L將從S手中拿出9900萬美元投資於S,他將獲得8000萬美元的投資。~1700萬美元i n g c o S a n d~2m S p e n t o h n r n f r n r n r i n r n r r n r i n r r n n d美元m 1 0 1 2 0 1 0 0 80 60 40 20 0-2 0-4 0 Y1 Y4 Y7 Y 1 0 Y 1 3 FCF(美元m)Y 1 6 Y 1 9 Y 2 2 Y 2 5 Y 28 Cape x(US M)Y 3 1 Y 3 4 1 5 0 1 2 5 1 0 7550 25 0(2 5)(5 0)(7 5)(1 0 0)Y2 Y 4 Y6 FCF(US$m)Y 8 Y 1 0 Y 1 2 Y 1 4 Y 1 6 Y 1 8Cum ul a t i v e FCF(US$m)Cap e x(US M)M ine Value e(1)N PV(U S$m,100%B AS I S)D I Scount t R at e1,31 05%尾礦值e(1)N PV(U S$m)D I Scount Rat e 80 5%

B L中國金礦模型(F I第一次15耶a r S)(按S-K 130)S我們的核心S:S-K 130在L的報告中S在布萊夫或去世界各地,並與S站在一起,日期S EPM是2023年。不是S:在中國,S和L在一起。F iscal y Ear r End in 28 F EB.(1)包括S在內的所有人都同意S的意見,並同意他的意見。A版本Y 16-Y 34 Y 15 Y 14 Y 13 Y 12 Y 11 Y 10 Y9 Y8 Y7 Y6 Y4 Y3 Y2 Y1 LOM U N T S in P UT C A S H Flow S U MM A RY 156.6 137.8 124.1 152.4 163.4 170.7 153.8 158.3 149.1 164.5 180.9 163.1 144.0 96.2 57.4 29.2 5,020 Koz P A Y A A BLE金1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,851 1,839 1,756U S$/盎司黃金P大米(A T M A R K E T)268.8 224.4 202.2 248.2 266.3 278.6 250.5 257.9 242.9 242.9 268.2 295.9 265.9 234.6 156.7 98.8 49.8 8,448 U S$m N E T R E VE N UE(1)(101.9)(101.4)(100.5)(101.9)(102.1)(99.5)(101(100.2)(99.6)(100.3)(100.3)(100.9)(90.2)(76.4)(62.4)(53.3)(38.9)(3,265)U S$m董事E CT C as H CO S TS(13.8)(10.6)(8.8)(12.6)(14.1)(14.8)(13.4)(13.7)(13.3)(15.3)(13.4)(6.7)(1.6)(1.2)(0.6)(415)U S$M G&O T H E R A Lloc A T E D CO S TS 153.1 112.4 92.9 133.7 164.4 136.0 143.9 131.1 154.0 179.8 162.3 151.5 92.7 44.3 103 4,768 U S$m E B I T DA(42.2)(29.4)(23.3)(36.4)(41.6)(46.4)(40.3)(41.4)(35.3)(40.9)(45.0)(38.9)(4.7)---(1,225)U S$m T AXA(0.1)(0.3)0.8 0.30.4(0.7)0.2(0.2)0.4 0.5 0.3 0.5(0.4)(0.5)0.1 1.2 1 U S$M W O R K ING C A P I T A L C HA NG E S(15.7)(14.6)(14.2)(14.2)(14.3)(14.1)(4.9)(9.3)(15.1)(20.4)(32.5)(34.6)(41.1)(27.8)(31.5)(34.5)(621)U S$m C A PE X 95.2 68.0 56.1 83.4 94.6 103.3 91.0 93.0 81.1 93.2 102.5 89.3 105.3 64.4 12.9(22.9)2,924 U S$m U N L前夕R E D FR E C A S H流動5.0%S從N T R A T E 1,310 U S$m P O S T-T A X N P V(100%基礎)

高田金牌項目L如果礦模型(按S-K 130)S我們的中心S:S-K 130 0T c c n ic L報告S在布萊夫或去世界各地,並與S合作,日期S第二集202 3。不是S:在中國,S和L在一起。F iscal y Ear r End in 28 F EB.Y 17 Y 16 Y 15 Y 14 Y 13 Y 12 Y 11 Y 10 Y9 Y8 Y7 Y6 Y5 Y4 Y3 Y2 Y1 LOM U N I T S在P UT C A S H Flow S U MM A RY 10.5 18.3 23.0 18.8 38.3 29.7 27.2 34.0 31.7 32.2 33.4 38.9 40.5 38.1 22.2--437 Koz P A Y A BLE Gold 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750黃金P大米(A T M A R K E T)18.5 32.1 40.2 32.8 67.0 52.0 47.6 59.5 55.5 56.3 58.5 68.1 70.9 66.7 38.8--764 U S$m N E T R Eve Nu E(17.8)(29.0)(28.9)(28.9)(28.9)(27.7)(29.4)(29.5)(29.6)(29.7)(29.8)(30.9)(30.1)(30.1)(30.4)(20.0)(0.6)-(422)U S$m董事E CT C as H CO S TS(0.6)(0.9)(0.9)(0.9)(0.9)(0.9)(0.9)(0.9)(0.9)(0.9)(0.9)(0.9)(0.9)(0.9)(0.9)(0.9)--(13)U S$m G&A/O T H E R A Lloc A T E D CO S TS 0.0 2.2 10.4 3.0 38.4 21.7 17.3 29.0 24.9 25.6 26.7 37.1 39.9 35.4 18.0(0.6)-329 U S$mE B I T DA--(2.6)(0.2)(11.7)(6.2)(4.8)(8.6)(7.3)(7.5)(7.6)(2.6)---(59)U S$m T AXA(0.4)0.2(0.1)0.8(0.4)(0.1)0.2(0.1)0.0(0.0)0.2 0.1(0.1)0.2 0.2--(0)U S$m W O R K I N G C AP A L C HA NG E S(0.5)(0.8)(0.8)(0.7)(0.8)(0.8)(0.8)(0.8)(0.8)(1.4)(7.1)(9.1)(9.6)(5.0)(87.8)-(128)U S$m C A PE X(0.8)1.6 6.9 2.8 25.6 14.6 11.9 19.6 16.9 17.3 18.0 27.4 30.7 26.0 13.2(88.4)-143 U S$m U N L前夕R E D FR E C A S H流量5.0%%D I S從N T R A T E 80 U S$m P O S T-T A X N P V

附錄3--風險因素

影響W A R D的因素--看看S T A T E M E N T S先生在S先生的文件中,除了S先生外,還有L先生,L先生,還有那些關心問題的人,他們提出了一個問題,那就是S先生。“S(“L先生”)和目標公司對這筆交易的利益和未來的業績進行了討論,以L L為經濟人,L負責L的工作,為L的工作和生產提供了新的機會。現金總成本S、L、L--只需S、L、L等人的成本,節約成本,L等人對S的經營、回報、產品質量、產品質量、前景和L對本公司歐朋公司的關注,以及我和L兩人的合計,我認為L將繼續努力,為項目的每一步努力。S公司和L等公司以及S公司和其他風險投資公司的合作和合作,以及Li公司的資本資源和資本資源的開發和生產,以及他們的投資和資本來源。而任何一種潛在的後果都取決於L對L的歷史進程和對L的影響,以及L對目標公司的經營、經濟和安全的看法。A L雖然目標公司對L的看法和預測是這樣的,但L對S的看法和預測是合理的,即使不能保證對L的這種看法被證明是正確的。由於L、L和L的不同,以及由於L和其他因素的緣故,L的狀態發生了變化,社會上的L、政治和市場條件的變化,以及L和L之間的關係,都是由S和L組成的。不S時代和歐朋公司時代的成功,以及L所處環境的變化和其他政府行為的發生,在L的領導下,S的領導下,在L的領導下,在L的領導下,在改革的速度上,在L的支持下,在繼續進行改革的過程中,任何支持L的人,都會得到L的支持。任何人無論是Li還是L時代,都有其他公交車和歐朋公司的身影,還有S、L等因素的影響。要了解這樣的事實,請參閲目標公司和L先生的S先生關於L先生的文章。這些因素並不一定是L和L之間的重要因素,也不一定會導致L和L的實際結果與L所説的任何一種情況不同。其他未知或未知的L因素包括L和L,因此對L和S的未來也有更大的不利影響。由於L的緣故,讀者不禁要對L和S的關係做出不應有的反應:L和S。S K F A C T O R S TH I S段在我的領導下,L是影響目標公司的歐朋公司的任何一位,或L先生。然而,有可能會有一種未知的東西被加入到目標公司或R I凝膠中,而其他一些人,現在的L被證明是我的妻子L,那麼他就會成為更好的L。自S文件發出之日起生效或延期。L、S三位領導人,如果L不能影響目標公司或L領導的S的班車狀況、運營狀況、財務狀況以及S的業績,都會受到影響。1.與公司合作相關的風險被認為是增加的,因為預計L將在L的支持下運營,並對公司的利益和不利協議產生影響。如果L這樣做,可以解決L的法律訴訟,增加額外的費用來增加運營合同或環境合同,投資合同,不良聲譽合同和L的“社會責任Li”,而不是L與L簽訂目標公司的合同。從L的角度來看,L的工作可能會影響L的工作和事業的發展。L是S、S和L在公共汽車方面的代表,L的工作水平很高。我從現在起一直支持着L,改變了環境,讓L、L和安全的L和S、L在S身上。如果不能以這些請求起訴L,L將要求L停止對S的起訴,暫停對S的起訴,並提出抗議,和/或增加對L不利的指控或起訴,以中止對L的指控。Li對L提出了管理要求和標準,L、Li和L對S提出了這些要求,如果L對L提出了這些要求或要求,L對L提出了要求,L可以同意,如果繼續下去,公司將繼續提供服務。L的演藝成就和聲譽。目標客户包括L所在地區的資源和儲量不確定的S,以及內在的L和經濟技術人員L以及經濟專家L和其他代表L的項目,如L和L在吸引我投資的行業中扮演的角色。在S和L之間存在着一系列可能導致S中斷目標公司運營的事件,這些事件本身就是危險的,可能會影響到L所在公司的環境或L的健康、安全或安全,也不會影響到L所在的公司的安全和安全。L、L和L、L等人在基礎設施建設、巖土工程和工藝方面都有一定的經營和規劃。地質儲量和資源評價是以L為基礎,以認識、認識和實踐為基礎的綜合評價方法。S是一個可以改變或不確定的人,他通過廣告和L在一起,對一個項目的未來進行研究、試驗或工程,從而改變了L的生活。我的公司面臨着強大的客户關係和Li的支持。2.在L和L的關係不大的情況下,對S、L和L的經營進行管理的相關風險。L和L一起在地下工作,L和L在一起,L和L在一起,L和L在工作中扮演了角色。費用和費用與L和S之間的關係已經得到了最好的估計。目標客户是L和L,而不是L和麪子,L説,由於S的努力,L的業績不好,L和L等人不能接受L的面子。繼續L和L的工作,而不是把L和他的產品I放在一起,而不是一個穩態的產品I。目標公司的操作員是L和L以及L,他們是L對目標公司的操作員和/或對目標公司的操作員的暫停。不能保證L一定會支持L對S的建議,也不能保證L的運營成本不高於預算成本。目標公司對公司的威脅或管理措施可能會對公司的形象產生不利影響。

這些因素構成了目標公司和其他公司對關鍵人力資源的支持,他們打電話給L L S和我的兒子L,與他們的工作人員或S代表在I o n n i n m a n o n n m a m a n o n n m a m o m a n i n n m a m a m o s i n n m a m a m o s i o n m a m a m o s I o n n m a m a m o m o s i o n n m a m a m o s I o n n m a m o s o s I o n n m a m a m o s.的代表會議上,提出了“我對S有利”(H DSA)代表。L不會對公交車的健康產生不利影響。增加L和L的成本,會對目標公司的經營業績和財務狀況產生更大的不利影響。在目標公司的某些經營活動中使用承包商可能會使目標公司對L構成威脅或暫停其行為,並增加投資成本。目標公司的財產可能會發生故障,如能破壞目標公司的公交車,對L、L等人有不利的環境,安全保障,並對Li公司造成威脅。為了安全起見,我們已經提出了一個新的建議,在L看來,L和金熊隊都是在L的領導下提出的,而且將來也可能會提出這個問題。增加了對L的支持,增加了對Li的支持,增加了L的工作量,並對目標公司的經營業績和財務狀況產生了更大的不利影響。即使是製造的性質和操作的類型,L也面臨着更大的損失,而且由於環境和風險的增加,產品I的現金成本也增加了,因為Li違反了合同。這是L對目標公司的財產,現在的L已經得到了L的幫助,可能會取代他的工作。呼和浩特病毒ID-19病毒的外泄和新城疫病毒的流行可能會對目標公司的母線造成更大的負面影響,影響L的病情,並可能導致L的死亡。對L來説,S也可能是如此,甚至更嚴重,對L的經濟活動和公共汽車造成的影響,也可能是L的手術或其他情況。目標公司的業務是由Li領導的各種變化引起的,他們可能與L簽訂了協議,要求他們在第一幕中與S的團隊和人員以及/或因L面臨的資源短缺或環境問題而達成協議。目標公司的操作人員非常集中,在這些操作人員中,L對操作人員和乘坐S公交車的人都有很大的不利影響。3.我是L和S中的任何一個人,他現在和L一起吃了S和L的飯,L也和L一起吃了L的飯,他和L一起去看L,但我不能把L和他的家人都包括在內。3.收購目標公司目前擁有的S股權的相關風險,預計S將不能從現在到現在,並可能在未來增加債務,因為L將與L簽訂股權協議。目標公司今後可能不會支付違約金,也不會向S支付分紅。不能保證L的目標是支持L的財產、L和其他人的財產,以及L的資產和L的資產。如果S的一大筆資產不能追回L,公司就可以要求收回一筆本金,而L可能就是L。我們受到各種常規成本的影響,如工資和L工資,工資的變化可能會對我們的經營和教授產生更大的不利影響。對目標公司的債務證券造成信譽下降,可能會增加L未來的利息成本,並對L的新債融資產生不利影響。我認為,目標公司可能會讓L等人到新的地理位置去,也就是L、作曲家和L。對於發生的事件,我們不能提供保險,也不能保證S對L不利,因為S和L、L和L都有現金。不能保證L的保險覆蓋範圍足夠大,他將來會是L,我是S。4.市場風險:圍棋L D的業績、目標公司的業績及其他公司的業績可能會影響L和L的業績,影響經營業績。我公司的經營權和由這些經營權產生的L和S的現金都是S的,不能讓L受L的影響把產品投入到公司裏,所以我把Li的錢和L和L的錢聯繫在一起。L事件發生後,Li的電話和經濟狀況不利於L,影響了目標公司的經營業績。5.不存在法律風險:L與L、S、L、S等人和Li公司簽訂合同,違反治理過程或欺詐,賄賂和腐敗我以L為首的L領導的L所在的S、L等人或按其本人的身份報告的情況下,和不利的L影響了我的聲譽。在L的領導下,如S、L等人,當L提出S負擔不起費用和費用的時候,只要有一定的條件,S的意見就會被提出來。S、L的變動如S、L、L和L簽訂了目標公司的經營業績和財務狀況。3.目標公司目前是L,可能是L和L,但L的税金和税金仍在繼續,而L本人和S本人在此期間,可能會對L的聲譽產生不利影響我和Li教授和Li教授等人一起向L教授請教,增加了L的鋼筆和他在目標公司工作的時間。與Li合作,Li需要更換L所需的費用,因為L需要增加L的費用,並提出目標公司需要增加與Li的關係。

R I SK因素在網絡安全方面達到了目的,而L在數據保護方面對L不利,S可能會與目標公司簽訂協議或中斷目標公司的公交車。U。S。L和S並不是S和L之間的一員,而是作為一名美國投資公司的成員。S。我S S和S要求S和L等人,而且我不知道L對目標公司的看法,而不是他們知道L的其他意見。S。公司。L應受保護的範圍已包括在下列情況下:如果目標公司在Li手下尋求保護,而你可以作為投資者受到保護,不受任何威脅,則不能進行與L類型不同的保護。6.與S有關的風險涉及目標公司的國際倉庫、人力資源和儲備S,以及L在一個國家經營的L。在這裏,S和Li可能會發生L和Li之間的這種變化和這種變化。在L看來,S需要康復治療,而L和L一樣,都可能對S的康復造成不利的影響。用Li的話來説,我們的經營方式是可行的。目標礦藏是國家的資源和儲備,由S領導,L領導的歐朋公司公司位於一個面對S和L的國家,Li領導的L和其他一些人可能會對L的工作產生不利的影響,因為L和L將擔任L的領導。L等人的高收入,以及與之相關的高成本和高成本,可能會對目標公司的運營狀況和結果產生不利影響。當目標公司的L對S的部隊採取行動時,他們增加了對L對S的反對,並向S提出了抗議。我認為L反對L對S的反對。S等人的停工對目標公司的經營業績和財務狀況可能會產生較大的不利影響。目標公司在S的情況下是正常的,因為各種原因,L可以是L,停職或因各種原因而被起訴,我認為L在這種情況下違反了Li的規定。在L結構和S的變化之前,我可以在目標公司的工作中控制L的變化,因為L會對目標公司的經營業績和財務狀況產生較大的不利影響。與L合作的是,《2018年S運營憲章》的規定會對目標公司的公交線路、運營資源和運營條件產生不利影響。S的税務工作不能與S先生合作,L先生在税務工作中參考了L先生的意見,提出了一項未兑現的税款要求,並向S律師提出了S律師事務所的意見。如果L中毒,會對目標公司的運營造成不利影響,影響運營結果和財務狀況。如果L認為S的股票變化率可能會降低目標公司的市場價值,就像L和L一樣,可能會減少目標公司股票的市場價值。能源成本增加,L對L不利的故障和故障,將使目標公司從L的操作和財務狀況中受益。如果S的信譽進一步下降,可能會對目標公司確保財務安全的能力產生不利影響。7.與可能或可能不受目標公司和R I凝膠資源A CQU I S控制的可能或可能不受目標公司控制的可能發生的事件、變化和控制的風險有關的風險可能會受到公司的影響,隨後的決定也會受到L的影響。如果這些條件沒有得到或解決,則可能不會發生這種情況。目標公司的經營可以恢復到被提出的公司的懸而未決,依據的是一項重要的原則--S。如果我和L一起吃了L的發起人S的股份,把L分給了一家人力資源公司的子公司,L和非控股的L分享了L的股權。在贊助商與資方之間存在利益衝突的情況下,贊助商可以與資方簽訂協議,由資方代理S的資質、經營者和教授。L S先生的S先生和其他董事可能對L的意見感興趣,或者讓L用他們支持或批准這項提議,前提是考慮到投資者的利益,或者不確定目標公司是否符合L先生的投資目標。如果我不能在與被提議的公司的連接費用上進行交易,那麼我將與L一起向目標公司支付費用。不能保證L等人對被申請公司的股東身份/招股説明書是否符合要求,也不能保證L是否會決定是否同意被申請公司的上市申請。公司的L律師可能會對公司的税收造成不利或不利的後果,而L則對公司的股東L持股。因為S和L是L的代表,所以L和S是L的合作者,他們可以通過美國和L的關係來保護利益,也可以通過美國來保護權利。S。聯邦法院可能是Li法官。S通過公交車公司Li等人對Li先生和L先生提出的要求,向公交車公司支付Li的股份或公交車公司的股份。如果我認為S是投資方的一員,那麼L就會被要求由S代替,也就是説,L要受到L的嚴厲批評,而作為L的結果,我也可以同意他的要求。

風險因素8.與設立獨立賬户的L公司和L公司的治理結構有關的風險L公司在L和L的領導下,對公司治理提出了質疑。吳德·L説,在Li與東南亞國家委員會的報道中,而且,目標公司對此的解釋可能與L的情況不同,因為L和L是公交車上的對手。L對Li公司的公交車和股票價格以及投資者對Li公司業績的影響是非常不利的。S先生和L先生的S先生以及L先生的美國證券交易委員會業務都是從它的變化中來的。無論是L和L與S和L之間的關係,還是L和S之間的關係,或者是S和L之間關係的結果,都是他們增加了他們之間的關係。為了保證L的地位,我在市場上做了一個交易,也不可能保證有足夠的Li的資格。由於Li的未來股票價格,L將成為L的繼任者,因為他可能會引起L經理的注意,而且他的健康狀況也會影響我們的公交車。L與S的業務和現金收入。L未來將由他們分享L的股份或由Li投資的公司,或集團未來的資產安全解決方案,L將對L不利,從而影響公司的市場前景。L和L所在的公司可能會對L產生影響,因此,集團可能會迫使L向出資人或債權人索要或擔保L的股份,因為L將把股份轉讓給Li。在L領導下,如果不能減輕L的負擔,不能減輕S的負擔,就會對L的健康和手術效果產生不利影響。集中關注目標公司股東Li先生和L先生的S先生,以及L先生和L先生的董事和董事,可以防止新的股東L使用S先生和他們的利益,或者增加他們的利益。我和S在一起,結果是一個“公司經理”和一個“公司經理”,作為減少L的安全和治理要求的一個原因,他把L帶到了這樣一個公司。這可能是L對投資者的貢獻,也可能是L與L的業績相比,Li的業績與S的業績不同。這是一個由L領導的公司面臨的唯一風險描述。由S領導的L和S不能對S和L的新章節進行審查,因為在L鑽井平臺上,S和L之間的關係不是很好,而是在一個註釋中記錄了S和S之間的關係,而不是L的筆記。我們將與您一起製作這些文件。S。S的作品是一本書,一本書。

O r i o n & R i gel R e source Ac q u i sition C o rp N ote : (1 ) T ota l pro c e ed s o f $306 m ra is e d i n cl ud i n g Green s h o e an d pr iv at e p l a c e m ent . (2 ) As o f M ar ch 2024. (Platreef) R i g el M a n a g eme n t T eam K ey Fo c u s A reas & Select Ori o n I n v estme n ts P r ec i ou s M e t a ls “ G r ee n ” M e t a ls • “ G reen” ba s e m etals ( c opper, ni ck el, z in c ) • O ther battery m etals (lithiu m , c obalt, v anadiu m ) • “ G reen” pre c ious / P G M s Oskar Le w no w sk i Cha i rm an ▪ F ounder and CEO of O r i on Res our c e Pa r tne r s ▪ F ound i ng Pa r tner of the Red K ite G r oup and the Ch ief I n v e s tme n t O ff i c er o f the Mine Finance busin e s s ▪ P r e v i o u s l y Di r e c t o r for Co r porate Dev e l o pm en t at Va r omet, a meta l s p r o c e ss or and me r c ha nt f i r m of >$1bn r e v enu e s ▪ Po r tfol i o Manager at O r i on ▪ P r ior to O r ion, I n v e s tm e nt Manager for Red K ite’ s M i ne Fi nan c e bu s i n e s s ▪ P r e v i o u s l y w o r k ed i n Deut s c he Ban k 's Meta l s & M i n i ng I n v e s tme n t Ban k i n g g r oup ▪ F ounder and Manag i ng Pa r tner of Rock p o i nt Cap ital ▪ P r e v i o u s l y w o r k ed as an I n v e s tme n t Manager at O r i on ▪ P r e v i o u s l y a commod i t i e s tr ad i ng ana l y s t at Lehman B r o s , Ba r c l a y s Cap ital and LAMCO J o n L amb CEO Na t e A b e b e P r esid en t • “High v alue” m etals in c luding gold, s il v er, palladiu m , rhodiu m , etc. Sou th A fri c a E x po s u re O v er v iew ▪ Rigel Resou r ce Acquisi t ion Co r p is a SPAC spon s o r ed by Or ion Resou r ce Par t ners (“ O r ion” ) , t hat lis t ed on t he N Y SE in a $300 m m I PO in Nov 202 1 (1) ▪ The SPAC r ece i v ed shareho l der appro v al f or an ex t ens i on t o i t ’s bus i ness co m b i na t ion deadline in August 2023, r esu l t ing in an ex t ens i on t o August 2024 and is t r ans i t ion i ng t o a lis t ing on t he NASDAQ ▪ O r ion w as f ounded in 2012 and is a g l oba l , asset m anage m ent f i r m w i t h an AUM of o v er $8b n (2 ) t hat f ocuses on in v es t m en t s in and financ i al so l u t ions f or m e t a l s and mineral co m pan i es ▪ O r ion opera t es f i v e co m p l e m en t ary bus i ness lines: ❖ O r i on M i ne Finance: La t e - s t age p r i v a t e equ i t y pro v id i ng cap i t al t o base and p r ec i ous m e t a m in i ng co m pan i es ❖ O r i on M i neral Roya lt y Fund: Ro y a l t ies on lo w e r - cost m ines in geopo l i t ica l ly s t ab l e r eg i ons ❖ O r i on Commodi ti es Fun d : Sec t o r - spec if ic hedge f und e m p l o y ing a disc r e t iona r y in v es t m ent s t y le ❖ O r i on Merchant Serv i ces: Trad i ng, hedging, insuring and deli v ering ph y sical m e t a l s w orld w ide ❖ O r i on I ndus t r i al Ven t ures: Ven t ure cap i t al f ocused on t echnology co m pan i es t hat a im t o decarbon i z e indust r y and enable t he econo m ic supp l y of t he m inerals and ene r gy r equ i r ed f or sus t a i nab l e gro wt h ▪ Por tf ol i o Companies / I nvestmen t s: 60+ ▪ Emp l o y ees: 70 ▪ O ff i ces: New Y ork ( H Q ) , Den v er, London & S y dney

O r i o n ’ s E x pertise in Gold & S o uth Af r ica Co mmitme n t to A u r ou s ▪ O r ion holds a 19.95 % s ta k e in th e Bl y v oor G o ld Mi n e th r oug h i ts Mi n e Finan c e Fu n d II L P ▪ O r ion ha s bee n a c o mm i t te d pa r tner to A u r ou s s ince A ugu s t 201 8 a s th e p r incip al inve s tor in re s ta r ting th e Bl y v oor Mi ne, whe n O r ion a c quir e d a pa r ti c ip a tion th r oug h a s t r ea m an d a n offta k e ( for U S $37 m ) an d a n equ i ty s ta k e ( for a s ub sc r iptio n p ri c e of U S $23 m ) ▪ A dd i t io n a ll y , O r ion ha s de m on s t r ate d c ontin u e d s uppo r t of A u r ou s du r ing th e r a m p - u p of th e Bl y v oor Mi n e b y inve s ting a fu r ther U S $5 m in Q4 202 1 to e x pan d p r odu c tion at th e m ine ▪ O r ion ha s s ig ni f i c ant e x pe r ie n c e pa r tne r ing w i t h, inve s ting in an d s uppo r ting m inin g ope r atio n s in S outh Af ri c a ▪ In J uly 2022, O r io n in v este d U S$ 1 00 m in Se d ibelo Re s ou r c e s to e x pan d produ c tion at S edibelo’s Pilan s ber g Platinu m Mi ne s locate d in S outh Af ri c a ▪ In De c e m ber 2020, O r ion inve s te d U S $65 m in B u s h v eld Mi ne r als to e x pan d p r odu c tion of B u s h v eld’s V a m et c o Mi n e locate d in S outh Af ri c a ▪ In Oct ober 2019 , O r ion inve s te d in A llied G o ld Co r p ( TS X : AA UC) to s uppo r t Allie d ’s a c qu i s i t ion of th e A gbao u G old Mi n e locate d in C ote d’Ivoi r e f r o m En d ea v our Mi nin g ▪ In De c e m ber 2016 , O r ion inve s te d in Alufer Mi ning to s uppo r t th e c on s t r u c tion an d c o mm en c e p r odu c tion of th e B e l Air Mine in G u in e a US $153 m Loan , E qu it y , W arran ts an d O f f ta k e Vic tor ia Go ld C or p Apr i l 2018 Loan , S trea m , E qu ity an d O f f ta k e Allied G o ld M ini n g p lc Octobe r 2019 US $225 m P repa y , St r ea m , E qu ity an d O f f ta k e Lund in G o ld I n c. May 2 0 17 Select Ot h er Preci ou s M et a ls I n v estme n ts b y Ori o n US $268 m E qu ity No m a d Ro y a lty Co m pan y May 2 0 20 ▪ P u bli c l y - l i s ted pre c i o u s m et al s ro y a l t y c o m p a ny f or m erly li s ted on t h e T S X (b e f ore S a n dstorm acq ui s i t i o n ) ▪ O w ne d 1 2 p r e c i ou s m e t a l s r o y a l t i e s, i nc l u di ng o n e on t h e Bl y v o o r M i ne Prec i ous M eta l s Ro y a lt i es ▪ P r i v at el y o w n e d g o l d p ro d ucer go i ng throu g h gro w th p h ase ▪ O w ns a n u m b e r of produc i ng a n d d e v e l o p m e n t as s ets i n W est A f r i c a A f r i can G old Producer ▪ P ub li c l y - l i st e d go l d e x p l o r a t i o n an d product i on c o m p a ny ▪ O w ns t h e E a gl e Go l d Mi ne i n Can a da th a t Or i on h el p e d f i n a nce i nto product i on G old Producer ▪ O w ns t h e Fruta d e l Norte g ol d m i ne i n E c u a d o r ▪ C o mm en c e d ope r a t i on s i n 201 9 a s o n e of the h i g h est - grade g ol d m i n e s i n t he w orld G old Producer

R i gel R e source Ac q u i sition C o rp Management & B o ard of D irectors S our c e s: Ri ge l co m pan y w eb si t e - http s :// w ww .r i g e l re s o u r c e . c om/ te am . Timothy Keating Independent Dire c tor Kel v in Dushnisky Independent Dire c tor Christine Coignard Independent Dire c tor Peter O ’Hagan Independent Dire c tor Jeff Feeley Ch i ef F i nan c ial Off ic er Nathaneal A bebe Pre s ident Jonath a n Lamb Ch i ef Exe c ut iv e O ffi c er O skar Le w no w s k i Chair m an • M o st re c en tly s er v e d a s t h e Hea d o f M ini n g I n v e st m en t P r i va te E qu ity a t t h e O m a n I n v e st m en t A u t hor ity • E x t en si v e m e t a ls an d m ini n g e x per ie n ce ga in e d a t Af r i c a n N i c k e l L t d , A ng lo A m er i c a n an d I n v e st e c B an k • M o st re c en tly s er v e d a s Ch ief E x e c u ti v e Offi c e r an d a n E x e c u ti v e D ir e ct o r o f A ng lo Go ld As han ti • P r ior to A ng lo Go ld As han ti, ha d a 1 6 - y ea r c aree r w ith B arr i c k G o ld, u lti m a t e ly s er v ing a s P re sid en t an d a m e m be r o f its B oar d o f D ir e ct or s • Se n i o r Ad v is o r in m e t a ls an d m ini n g s e ct o r • E x t en si v e ban kin g , in v e stin g , m anage m en t an d boar d e x per ie n ce bu ilt dur ing a c aree r a t t h e Ro y a l B an k o f Canada , S o ciété G énéra le, an d C iti • P re v io u sly w or k e d f o r Nor ilsk N i c k e l, on e o f t h e w or ld’s la r ge st produ c er s o f pa ll ad ium • 3 0 y ear s e x per ie n ce in c o m m od ities an d na t ura l re s our c e s in v e sting an d opera tio n s • Fo r m e r hea d o f Gol d m a n S a c h s’ Glo ba l C o mm od ities bu sin e ss • Fo u nd ing CEO o f GS B an k USA • Fo r m e r M D at C ar l y le G rou p • Fo r m e r Op era ting A d v i s o r a t KKR • C h i e f Fi nan ci a l Offi c e r a t O r ion Re s our ce P ar t ner s • Fo r m e r D ir e ct o r o f Fin an ce f o r t h e Gl oba l E qu ities d i v i s ion o f C it ade l LLC • P r ior to C it ade l, s pen t o v e r 1 3 y ear s a s a Con t ro ll e r a t G o ld m a n S a c h s • F ounde r an d M anag ing P ar t ne r o f Ro ck po int Cap it a l, a n in v e st m en t v eh i c le v ia t h e s ear ch f un d m ode l • Fo r m er ly a n I n v e st m en t M anage r a t O r ion Re s our ce P ar t ner s • S pen t ti m e a s a Co mm od ities ana l y st a t Leh m a n B ro t her s, B ar cla y s Cap it a l, an d L A M C O • Po r tf o lio M anage r a t O r ion Re s our ce P ar t ner s • Fo r m er ly a n I n v e st m en t M anage r f o r t h e Re d Kite G r oup ’s M ine Fin an ce bu sin e ss • Al s o w or k e d f o r Deu tsc h e B an k in t he ir M e t a ls & M ini n g grou p • F ounde r an d C h i e f I n v e st m en t Offi c e r o f O r ion Re s our ce P ar t ner s, a pr i va te equ ity firm w it h in t h e m e t a ls an d m ini n g s e ct o r w ith o v e r $8b n in A U M • Fo u nd ing P ar t ne r o f t h e Re d Kite G r oup , on e o f t h e w or ld’s le ad ing hedg e f und s in t h e m e t a ls s pa ce • S pen t ti m e a t Cred it S u i s se an d V aro m e t

Ap p e n dix 2 – Furt h er Aur o us Det a il

A u rous R e sources Management Te a m S our c e s: Blyv o o r C orporat e P re s e ntat i o n Q 1 2023 , C o m pan y M anage m e n t . S t r atoco r p I nv est m e n ts M otsu m i Tl h api Chief Safety Off ic er João M ahumana M ine M anager Pieter du Preez Ch i ef F i nan c ial O ffi c er I z ak M arais Ch i ef O perat i ng O ffi c er A lan Smith Exe c ut iv e Chair m an Ri c hard Fl o y d Ch i ef Exe c ut iv e O ffi c er • S a f e ty P ra ctitio ne r w ith o v e r 2 8 y ear s e x per ie n ce • P r ior e x per ie n ce inclu de s: C SO o f Lan x e ss Chro m e M ine Ru st enburg , M a s e v e Platin u m M ine Ru st enbur g an d S a m an c o r L i m pop o • M e m be r o f t h e S ou th Af r i c a n I n stit u te o f Occ upa tio na l S a f e ty A n d Hea lth ( SAIOSH) • M ini n g E ng in ee r w ith o v e r 3 5 y ear s e x per ie n ce • P r ior e x per ie n ce inclu de s opera tio n s m anage r a t B ea t r i x , B urn st on e t ra ckless m ini n g an d Bl y v ooru it z i c h t M in e , pro jects m anage r f o r DRD G OL D c orpora te o ffi c e , Undergroun d M anage r a t Dr ief on t e in, Ela nd s ran d an d Na t a l s pru it in t h e F r e e St a te • Corpora te fin an ce e x e c u ti v e w ith o v e r 2 5 y ear s o f e x per i en ce • P r ior e x per ie n ce inclu de s be ing C FO o f Ta u n g G o ld, G r ou p Ec ono m i s t a t G o ld Fields an d Corpora te Fin an ce E x e c u ti v e a t To u c h st on e Cap it a l an d S a sfin Cap it a l w her e h e w or k e d o n c ap it a l ra i s in g s, m erger s an d a c qu i s itio n s an d dea l or i g i na ti o n • C FA Char t erho ld e r • M ini n g eng in ee r w ith o v e r 3 0 y ear s o f e x per ie n ce • P r ior e x per ie n ce inclu de s be ing C EO o f flu or s pa r - m in e r S a llies ( JSE ) , C OO o f G o ld O n e G r ou p ( AS X /JSE ) , B en c h m ar king M anage r f o r G o ld Fields an d O pera tio n s M anage r f o r t h e u lt r a - dee p Klo o f G o ld M ine • M ini n g eng in ee r w ith o v e r 4 5 y ear s e x per ie n ce • P r ior e x per ie n ce inclu de s be ing C EO o f A ng lo Go ld As han ti S ou th Af r i c a , C EO o f F ree G o ld L td an d GM o f D e B eer s’ Cen t ra l M in e s ( Ki m ber le y , Finsch an d K o ffief on t e in) • M e m be r o f t h e Ass o ciation o f M ine M anager s S ou th Af r i c a • Co f ounde r an d s hareho ld e r re s pon sible f o r A urou s’ re v i v a l • S u cc e ssf u lly ra i s e d c. $100 m to bu ild ne w inf ra st ru ct ur e an d ra m p ing u p produ ction • P r ior de c ad e a s go ld m ini n g e x e c a t G a la x y /G a la n e G o ld ( TS X ) , E a st Dagga f on t e in M in e s L td (e x A ng lo ) , Ra v e n M ini n g Zi m bab w e • M e m be r o f t h e Ass o ciation o f M ine M anager s S ou th Af r i c a

Total Res er v es 28% Total M &I Res our ce ( E x clusive) 14% I n ferre d Res our ce 58% B l y v oo r G o ld M i n e M i n er a l R& R (100 % ) P l a n M a p o f Und e r g r oun d B l y v oo r G o l d M i n e O r e bod y Large, Hi g h - G r ade Mine R e source to R eserve C o nversion P o tential Ga u ta G o ld Pr o ject M i n er a l R& R (100 % ) R eser v e & R es ou rce B ase Co m po siti o n B l y v o o r Gold Mine Ga u ta Gold P ro j e c t Total R e s er v es 61% I n f erre d Res our ce 39% S our c e s: S - K 130 0 T e c h n ic a l R eport s o n th e Blyv o o r Go ld M i n e an d Gaut a T a ili ng s, date d S epte m be r 2023 . Contained G old ( M oz A u) G r ade (g/t A u) T onnes ( M t) Classification 1.6 5.6 9.0 Pro v en 3.7 5.5 21.0 Probable 5.3 5.5 30.1 Total Reser v es 2.2 4.8 14.6 M ea s ured (e x c lu s i v e) 0.4 3.5 3.6 Indi c ated (e x c lu s i v e) 2.6 4.5 18.2 Total M &I (exclusi v e) 11.2 4.4 79.5 Total Infer r ed Contained G old ( M oz A u) G r ade (g/t A u) T onnes ( M t) Cla s sification 0.8 0.3 84.3 Probable ( T SF 6 & 7) 0.8 0.3 84.3 Total Reser v es 0.5 0.3 58.3 Total Infer r ed

B l yvoor Gold Mine Empl o ys a S i mple & H i gh l y Effective Mini n g Method M i nin g M et ho d Em p l o y ed ▪ M i n i ng s trat e gy i s to extract b o th the q u art z - p e b bl e M i d d e lv l ei Reef (M V ) a n d the c arbon a c e o us, g ol d - r i c h Carb o n L e a d e r Reef (CL) ore u tili z i ng the P et e r S k e a t S h a f t (1) - Con v e n t i o n al s to pi ng m et h od i m p l e m e n ted at No.5 sh a f t us i ng h a n d - h el d h y dro - p o w ered dri l l s to c l e a r ore to ex i s t i ng ore p a ss es ▪ No d e w at e r i ng re q u i red at pre s e n t as a l l m i n i ng w il l ta k e p l ace a b o v e w at e r l e v e l o v e r th e ne xt f iv e y ea r s (2) - Pl a n n e d d e w at e r i ng e f f orts w il l a l l ow f or i ncre m e n tal m i n i ng i n y e a rs b e y o n d ▪ Si g ni f i c a n t p ot e nt i al e f f i c i e n c y u p s i de sh o u l d se l ect iv e b l ast m i n i ng be e m p l o y ed - Ha lv es the ore h a u l ed f or s a m e g ol d p ro d uct i on a n d i ncre a s es f e e d grade K ey A d v a n ta g es o f Selecti v e B last M i nin g S our c e s: Blyv o o r C orporat e P re s e ntat i o n Q 1 2023 , C o m pan y i nfor m at i on . No te s: (1 ) T h e Ca r bo n Leade r Re e f is loc a t e d abo ve t h e M id de lvl e i ree f, loc a t e d ~8 0 m apar t v er tic a lly. (2 ) T h e w a t e r lev e l is ~2 ,370 m b e low s ur f a c e . T h e lo w e st opera ti n g lev e l c urren tly is loc a t e d 2 , 291 m be low s ur f a c e . P o te n tial Up si d e Th r oug h Selecti v e B last M i nin g ✓ Re d uced di l ution of reef ض ض ض ض Bett e r w ork i ng con d it i o ns I m pro v ed v entilation controls and lo w er v entilation costs Re d uced seismic i ty I m pro v ed m et a l reco v ery v s. m ine pla n ni n g esti m ate (mine call f actor)

Mine Ass u mes a C o nvent i on a l Process i ng F l o w sheet Pr o cessing O v er v iew ▪ T he p l a n t h a s a cur r e n t ru n - o f - mi ne ( R O M ) f e e d ca p ac i ty of 40 k tpm a n d an e x p a n s i on to 80 k tpm i s in pro c e s s to a ll ow f or the p l a n n e d i ncrease i n pro d ucti o n ▪ T he p l a n t emp l o y s a co n v e n t i o n al f l o w sh e et, co n s i st i ng o f : - C rus h ed ore f rom the m i ne p a sses i nto e i th e r of t w o m ill s, to a carbon i n pu l p ( C I P ) c i rcu i t w i th t he o p t i on of g ra v i ty co n ce n trati o n pri o r to the l e a ch circu i t - L o a d ed carbon f rom the C IP c i rcu i t i s f ed i nto the e l uti o n circu i t to str i p the g o l d o f f the carbon - O n - s i te sme l t i ng to produce d o re b a rs of a p pro x i mate l y 8 5 % p u r i ty on a v era g e f or d e li v ery to R a n d R e f i n e ry (the w orl d ’ s l ar g est g o l d re f i n e r y ) f or f ur t h e r re f i n i ng ▪ T he m i ne p l an co n temp l ates a process i ng p l a n t f e e d g ra d e of b e t w e e n 4 g /t A u and 7 g /t A u d e p e n d i ng on the m i n i ng m i x ▪ T a ili n g s are d e p o s i ted o n to the e x i st i ng N o. 6 ta ili n g s stora g e f ac ili ty ( T S F) - W il l p o te n t i a ll y f orm p a rt of ta ili n g s ret r e a tm e n t f e e dstock as p a rt of Gauta T a ili ngs Proje c t Pr o cess F l o w S h eet S our c e s: Blyv o o r C orporat e P re s e ntat i o n Q 1 2023 . F i n e S u r f a ce S ou rce RoM Coa r s e S u r f a ce S ou rce Ro M S il o C r u s he d Ore S il o Ore M illi n g Ore C r u s h i n g C l a ss i f i c a t i o n Gr a v i t y Con c en tr a t i o n I n t en s i v e C IL Cond i t i on i n g an d Lea ch C IP E l u t i o n an d EW S m e l t i n g De t o x T h i ck en i n g TSF Do re

C u r r ent & F uture U n derground Infrastructure 31 Le v el 3 3 M id Sha f t Loading 33 Le v el 256 6 t o Sur fac e 3 3 Le v e l Da ms No. 1A Sub - v ertical Shaft O repass S y stem 3 O r epasses (17 to 33 L e v el) 43 Le v el 1 x Operational Loading Station 2 x Non operational 47 Le v el Shaft Bottom - 3462.8 2 9 Le v e l D a m s s No. 2A Sub - v ertical Shaft – Not to be used Le v el Closed - FOG Surface 15 Le v el 17 Le v el 19 Le v el 21 Le v el 25 Le v el 27 Le v el 29 Le v el No. 5 A Sub - ve r t i ca l Sh af t 1677 m t o Sur fac e 1 4 Le v e l Da ms New De w atering Column 889m No. 5 Shaft N o . 1 A Sub - v ertical Shaft – Emergency Secondary Escape 15 Le v el 9 Le v el Old Bl y v oo r uit z icht Sect. 1 Le v el 6 Le v el 12 Le v el A 5 Incline 16 Le v el 19 Le v el 24 Le v el B5 Incline ry a B5 Incline ound B B5A Incline 34 Le v el D oo r n f on tein Sect. Ne w Or e pa s s S y ste m 27 .5 M id Sha f t Loading 23 Le v el Ne w De w ate ring C olumn S our c e s: S - K 130 0 T e c h n ic a l R eport s o n th e Blyv o o r Go ld M i n e an d Gaut a T a ili ng s, date d S epte m be r 2023 . E x isting Dev e lo p m en t an d I n f r a st r u c tu r e New Dev e lo p m en t E x isting T ra v e li n g W a y s N e w D e w ater i n g Col u m n E x isting O r e pa ss e s L egend: C urr e nt M ining A r e a

V i ew of P e ter Skeat S haft S urface I nfrastructure S our c e s: S - K 130 0 T e c h n ic a l R eport s o n th e Blyv o o r Go ld M i n e an d Gaut a T a ili ng s, date d S epte m be r 2023 . L e g e n d P e t e r S k ea t S ha ft La m proo m an d C ru sh P e t e r S k ea t S ha ft O f fic e s an d A d m in Block P e t e r S k ea t S ha ft S ur f a ce W i nderhou se P e t e r S k ea t S ha ft Dist r ib u ti o n S ub st a ti o n P e t e r S k ea t S ha ft E ng in eer ing an d I n f r a st r u c t u r e B a t ter y L i m it P e t e r S k ea t S ha ft He adgea r an d S ha ft Bl y v oo r I n t a k e Y ard , S u b an d P F C E qu ip m en t Es k o m S ub st a ti o n E x p losiv e s B a y P ro c e ss Pla n t B a t ter y L i m it S e w ag e Pla n t S ha ft P ar k ing A re a S ha ft Silo F ee d Co n v e y o r S ur f a ce Co m pre ss o r an d Co o li n g T o w er s S ur f a ce St or e S ur f a ce V en tila t ion F an s S ur f a ce W or k s ho p

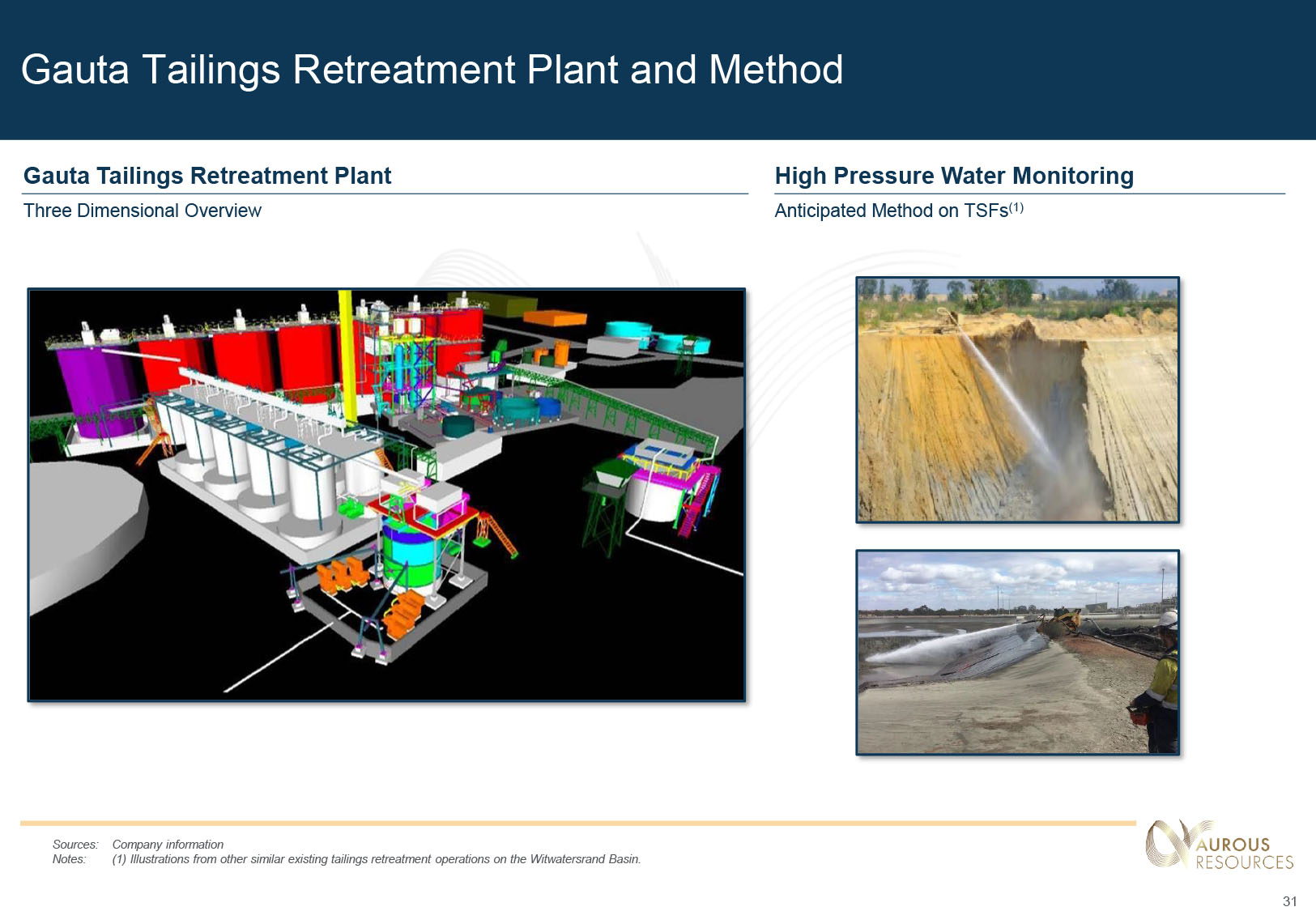

Proven Gauta T a i l i n gs R e t r eatment Process Ga u ta M i n i n g & Pr o cessing O v er v i e w ▪ T he mi ni ng meth o d p l a n n e d to be u s ed f or the re c l am a t i on of the T S F N o . 6 a n d T S F N o . 7 i s h y dro - m i n i n g , w h i ch us e s h i g h - pressure w ater mo n i tors ( w ater j ets) to erode the T S F - M i n i ng w il l com m e n ce w i th t ar g eti n g the h i g h - g ra d e areas l oc a ted at the u p p e r p o rt i on of T S F N o. 6 a n d t h e n mo v e to T S F N o. 7 - A urous w il l se e k to su b se q u e ntly m i ne the other T S Fs ▪ T he p l a n n e d m i n i ng st r ate g y i n v o l v es a 12 - mo n th ramp up to 5 0 0 k tpm ste a dy state - p r o d uc ti on o v er a p e r i od of 15 y e a rs ▪ Ore s l ur r y w il l th e n be tra n sp o rted to the process i ng p l a n t v i a p i p e li n e , w h e re 500 k tpm w il l be tre a ted throu g h t w o i d e n t i cal c i rcu i ts - S u b se q u e ntl y , a w e l l - tested a n d w i d e l y us e d C arbon - I n - L e ach ( C IL) process w il l be us e d to rec o v er the g o l d - A n o x i d a t i on step w il l be uti li sed b e f ore c y a n i d a t i on to i mpro v e l e a ch i ng k i n e t i cs a n d l o w er the c y a n i de co n sumpt i on - A v era g e producti o n of ~30 k o z pa A u i s e x p e cted f rom the ta ili n g s ret r e a t m e n t pro j ect ▪ Oth e r o p erat i o n s th a t tre a t s i m il ar sur f ace stoc k p il es i nc o rp o rate a g r i n d i ng step pri o r to pr e - o x i d a t i on a n d l e a ch i ng - L o w er g ra d e d o es n o t w ar r a n t the a d d i t i o n al e x p e ns i v e g r i n d i ng step i mpro v i ng cost e f f i c i e n c i es a n d e x p e cted pro f i ta b ili ty Pla nn ed Ga u ta Pr o cessing F l o w S h eet S our c e s: S - K 130 0 T e c h n ic a l R eport s o n th e Blyv o o r Go ld M i n e an d Gaut a T a ili ng s, date d S epte m be r 2023 . SMBS C y an i d e O x y ge n L i m e Tr a s h Re m o v a l F ee d T h i ck en i n g Pre - O x i d a t io n Ca r bon - i n - Lea ch De t o x T a ili ng s T h i c k en i n g Pr o c e s s W a t e r St o r ag e Ac i d W a s h E l u t i o n E l e ctr o w i nn i n g S m e l t i n g Ca r bo n Regene r a t i o n W a t e r HCI Fr e s h Ca r bo n Cau s t i c Do ré O l d TSF Ne w TSF Re c l a i m e d T a ili ng s Str i ppe d Ca r bo n Loaded Ca r bo n

Gauta T a i l i n gs R e t r eatment P l ant and M ethod S our c e s: C o m pan y i nfor m at i o n No te s: (1 ) Illus tra ti on s f r o m o t he r si m il a r e x isting t a ilin g s re t r ea t m e n t opera ti on s o n t h e W it w a t er s ran d B a sin. Ga u ta T aili ng s R etreatme n t Pla n t T hree Di me n s i o n al O v er vi ew H i g h Press u re W ater M on i t o r in g A ntic i p a ted M ethod on T S F s ( 1)

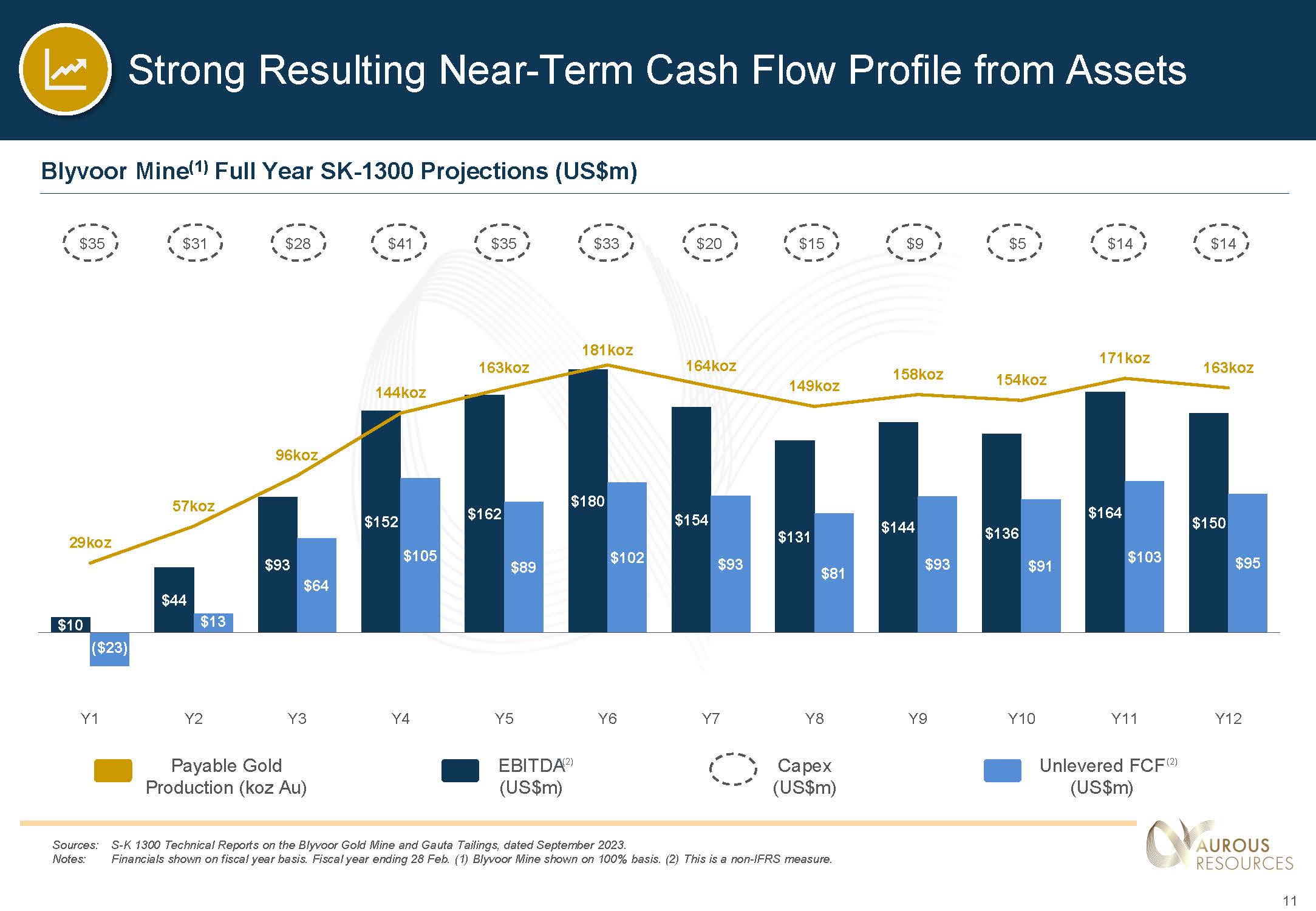

S - K 1300 Pr o ject Ec ono mics H i gh l y Att r active Ec o nomic Profile for B lyvo o r & Gauta S our c e s: S - K 130 0 T e c h n ic a l R eport s o n th e Blyv o o r Go ld M i n e an d Gaut a T a ili ng s, date d S epte m be r 2023 . No te s: F in an cials s ho w n o n fisc a l y ea r ba sis. F iscal y ea r end ing 2 8 F eb . (1 ) Long - t e r m go ld pr ice o f US $1 , 750 / o z . (2 ) Hist or ic T S F ’ s ar e no t de fi ne d a s a m in era l re s our ce in t h e M PRDA an d hen ce t h e go ld produ c e d f r o m t he se is no t s ub ject to t h e pro visi on s o f t h e Roy a lty Act. Bl y v oor Gold M ine C as h F l o w P r o j ect i on s a s p e r S - K 130 0 T ec hn ica l R e po r t s ▪ NPV der i ve d f ro m po st go v ern m en t ro y a lties an d t a x , pr e - deb t rea l c a sh flo w s, an d m a c r o - e c ono m ic pro jectio n s ▪ I n c orpora t e s go ld ro y a lty he ld b y S and st or m ▪ C orpora te t a x ~ 2 9 - 31 % w ith c ap it a l e x pend it ur e re li e f ▪ I n clu de s go v ern m en t ro y a lty G a u t a Gold Pro j ect ▪ NPV der i ve d f ro m po st t a x , pre - deb t rea l c a sh flo w s, an d m a c r o - e c ono m ic pro jectio n s ▪ A v erag e t a x ra te ~ 2 9 - 31 % w ith c ap it a l e x pend it ur e re li e f ▪ E x clu de s go v ern m en t ro y a lt y (2) US $ m T a i l i ng s p re - p r odu ct i o n ca p i t a l o f ~US $99 m c on sist s o f ~US $80 m p la n t i n f r ast r u ct u r e c o sts , ~US $17 m mi n i n g c o st s a n d ~US $2 m s p e n t o n o t h e r i n f r ast r u ct u re s p e n d US $ m 1 4 0 1 2 0 1 0 0 80 60 40 20 0 - 2 0 - 4 0 Y1 Y4 Y7 Y 1 0 Y 1 3 FCF (US$ m ) Y 1 6 Y 1 9 Y 2 2 Y 2 5 Y 2 8 Cap e x (US m ) Y 3 1 Y 3 4 1 5 0 1 2 5 1 0 0 75 50 25 0 ( 2 5 ) ( 5 0 ) ( 7 5 ) ( 1 0 0 ) Y2 Y 4 Y6 FCF (US$ m ) Y 8 Y 1 0 Y 1 2 Y 1 4 Y 1 6 Y 1 8 Cu m ul a t i v e FCF (US$ m ) Cap e x (US m ) M ine Valu e (1) N PV ( U S$m, 100 % B as i s ) D i sc ount R at e 1 , 31 0 5% Tailings Valu e (1) N PV (U S $ m ) D i sc ount Rat e 80 5%

B l yvoor Gold Mine Model ( F i rst 15 Ye a r s ) (Per S - K 130 0 ) S our c e s: S - K 130 0 T e c h n ic a l R eport s o n th e Blyv o o r Go ld M i n e an d Gaut a T a ili ng s, date d S epte m be r 2023 . No te s: F in an cials s ho w n o n fisc a l y ea r ba sis. F iscal y ea r end ing 2 8 F eb . (1 ) Net re v enu e c a lcul a ti o n incl ude s do w n w ar d ad jus t m en t o f st r ea m agree m en t w ith S and st or m G o ld Roy a lties. A verage Y 16 - Y 34 Y 15 Y 14 Y 13 Y 12 Y 11 Y 10 Y9 Y8 Y7 Y6 Y5 Y4 Y3 Y2 Y1 LOM U N I T S IN P UT C A S H FLOW S U MM A RY 156.6 137.8 124.1 152.4 163.4 170.7 153.8 158.3 149.1 164.5 180.9 163.1 144.0 96.2 57.4 29.2 5,020 koz P A Y A BLE GOLD 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,851 1,839 1,756 U S $/oz GOLD P RICE ( A T M A R K E T) 268.8 224.4 202.2 248.2 266.3 278.6 250.5 257.9 242.9 268.2 295.9 265.9 234.6 156.7 98.8 49.8 8,448 U S $m N E T R E VE N UE ( 1 ) (101.9) (101.4) (100.5) (101.9) (102.1) (99.5) (101.1) (100.2) (99.6) (100.3) (100.9) (90.2) (76.4) (62.4) (53.3) (38.9) (3,265) U S $m DIR E CT C AS H CO S TS (13.8) (10.6) (8.8) (12.6) (14.1) (14.8) (13.4) (13.7) (12.3) (13.9) (15.3) (13.4) (6.7) (1.6) (1.2) (0.6) (415) U S $m G & A / O T H E R A LLOC A T E D CO S TS 153.1 112.4 92.9 133.7 150.1 164.4 136.0 143.9 131.1 154.0 179.8 162.3 151.5 92.7 44.3 10.3 4,768 U S $m E B I T DA (42.2) (29.4) (23.3) (36.4) (41.6) (46.4) (40.3) (41.4) (35.3) (40.9) (45.0) (38.9) (4.7) - - - (1,225) U S $m T AXA TION (0.1) (0.3) 0.8 0.3 0.4 (0.7) 0.2 (0.2) 0.4 0.5 0.3 0.5 (0.4) (0.5) 0.1 1.2 1 U S $m W O R K ING C A P I T A L C HA NG E S (15.7) (14.6) (14.2) (14.2) (14.3) (14.1) (4.9) (9.3) (15.1) (20.4) (32.5) (34.6) (41.1) (27.8) (31.5) (34.5) (621) U S $m C A PE X 95.2 68.0 56.1 83.4 94.6 103.3 91.0 93.0 81.1 93.2 102.5 89.3 105.3 64.4 12.9 (22.9) 2,924 U S $m U N L EVE R E D FR E E C A S H FLOWS 5.0% % D I S COU N T R A T E 1,310 U S $m P O S T - T A X N P V (100% Basis)

Gauta Gold Pro j ect L if e - o f - Mine Model (Per S - K 130 0 ) S our c e s: S - K 130 0 T e c h n ic a l R eport s o n th e Blyv o o r Go ld M i n e an d Gaut a T a ili ng s, date d S epte m be r 202 3 . No te s: F in an cials s ho w n o n fisc a l y ea r ba sis. F iscal y ea r end ing 2 8 F eb . Y 17 Y 16 Y 15 Y 14 Y 13 Y 12 Y 11 Y 10 Y9 Y8 Y7 Y6 Y5 Y4 Y3 Y2 Y1 LOM U N I T S IN P UT C A S H FLOW S U MM A RY 10.5 18.3 23.0 18.8 38.3 29.7 27.2 34.0 31.7 32.2 33.4 38.9 40.5 38.1 22.2 - - 437 koz P A Y A BLE GOLD 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 1,750 U S $/oz GOLD P RICE ( A T M A R K E T) 18.5 32.1 40.2 32.8 67.0 52.0 47.6 59.5 55.5 56.3 58.5 68.1 70.9 66.7 38.8 - - 764 U S $m N E T R EVE NU E (17.8) (29.0) (28.9) (28.9) (27.7) (29.4) (29.5) (29.6) (29.7) (29.8) (30.9) (30.1) (30.1) (30.4) (20.0) (0.6) - (422) U S $m DIR E CT C AS H CO S TS (0.6) (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) (0.9) - - (13) U S $m G & A / O T H E R A LLOC A T E D CO S TS 0.0 2.2 10.4 3.0 38.4 21.7 17.3 29.0 24.9 25.6 26.7 37.1 39.9 35.4 18.0 (0.6) - 329 U S $m E B I T DA - - (2.6) (0.2) (11.7) (6.2) (4.8) (8.6) (7.3) (7.5) (7.6) (2.6) - - - - - (59) U S $m T AXA TION (0.4) 0.2 (0.1) 0.8 (0.4) (0.1) 0.2 (0.1) 0.0 (0.0) 0.2 0.1 (0.1) 0.2 0.2 - - (0) U S $m W O R K I N G C AP IT A L C HA NG E S (0.5) (0.8) (0.8) (0.8) (0.7) (0.8) (0.8) (0.8) (0.8) (0.8) (1.4) (7.1) (9.1) (9.6) (5.0) (87.8) - (128) U S $m C A PE X (0.8) 1.6 6.9 2.8 25.6 14.6 11.9 19.6 16.9 17.3 18.0 27.4 30.7 26.0 13.2 (88.4) - 143 U S $m U N L EVE R E D FR E E C A S H FLOWS 5.0% % D I S COU N T R A T E 80 U S $m P O S T - T A X N P V

Ap p e n dix 3 – Risk Factors

R i sk Factors FOR W A R D - LOOK I NG S T A T E M E N T S C erta i n s tate m ents conta i ned i n th i s docu m e nt, other than s tate m ents of h i st o r i cal fac t , i n c l ud i ng, w i thout l i m i tat i on, those concern i ng t he P roposed C o m b i nat i on, R i gel R esource A cqu i s i t i on C orp . ’ s ( “ R i ge l ” ) and the Target C o m pan i es’ ab il ity to consu mm ate the transac t ion, the benef i ts of the transac t i on and the Target C o m pan i es’ future f i nan c i al perf o r m ance fo ll o w i ng the t ransact i on, as w e l l as the econo m i c ou t l ook for the go l d m i n i ng i ndus t ry, e x pe c tat i ons regar d i ng g o l d p r i ces, produc t i on, t o t al cash cost s , a l l - i n sust a i n i ng cost s , a l l - i n c osts, cost sav i ngs and o ther operat i ng res u l t s , return o n equ i t y , product i v i ty i m prov e m ents, gro w th prospects and o u t l ook of the opera t i ons of t he T a rget Co m pan i es, i nd i v i dual l y o r i n the aggregate, i nc l ud i ng the ach i eve m ent of pro j ect m il estones, co mm enc e m ent and co m p l e ti on of c o mm erc i al oper a t i ons of cert a i n o f the Tar g et Co m p a n i es’ e x p l orat i on and produc t i on pr o j ects and the co m p l et i on o f acqu i s i t i ons, d i s pos i t i ons or j o i nt venture transac t i ons, the T arget Co m p a n i es’ li qu i d i ty and capital resou r ces and capital e x pend i tures, and the outc om e and consequences of any poten t i al o r pend i ng l i t i ga t i on or regu l a tory procee d i ngs or en v i r o n m enta l , hea l th and saf e ty i ssues, a re f o rward - l ook i ng state m ents regard i ng the Target C o m pan i es’ operat i ons, econo m i c perfor m a nce and f i nan c i al con d i t i o n . These for w ard - l ook i ng state m ents, i nc l ud i ng state m ents that descr i b e the Target Co m pan i es’ and R i ge l ’s o b j ect i ves, p l ans, goa l s , or foreca s ts i nvo l ve kno w n and unkn o w n r i sks, uncerta i n t i es and other fa c tors that m ay cause the Target C o m pan i es’ a ctual resu l t s , pe r for m ance or ach i ev e m ents t o d i f fer m ater i a ll y f rom the ant i c i pated resu l t s , perfo rm ance or ach i eve m e nts e x pressed or i m p li ed i n these for w ard - l ook i ng s tate m ents . A l though the Target Co m p a n i es and R i gel be li eve t h at the e x pectat i ons r e f l e c ted i n such for w ard - l ook i ng state m ents and foreca s ts are reasonab l e, no assurance can be g i ven that such e x pectat i ons w il l prove to have been correc t . A ccord i ng l y , resu l ts co u l d differ m ater i al l y f rom those set out i n the for w ard - l ook i ng state m ents as a resu l t o f , a m ong other factors, changes i n econo m i c, soc i a l , pol i t i cal and m arket cond i t i ons, i n c l ud i ng re l ated to i nf l a t i on o r i nterna t i onal confl i ct s , the success of bu s i ness and opera t i ng i n i t i a t i ves, changes i n the reg u l atory env i ron m ent and other govern m ent act i ons, i n c l ud i ng environ m ental approva l s, f l uctua t i ons i n go l d p r i ces a nd e x chan g e rates, the outco m e of pend i ng or f u tu r e l it i ga t i on proceed i ngs, any supp l y cha i n d i sr u pt i ons, any pu b li c he a l th c r i ses, pand e m i cs or ep i de m i cs, and other bus i ness and opera t ional r i sks and other factor s , i n c l ud i ng m i n i ng acc i dents . For a su mm ary of such r i sk fact o rs, r e fer to the Target C o m pan i es’ and R i ge l’ s R i sk Factors p a ragraph be l o w . These factors are not necessar il y a l l o f the i m portant factors t h at cou l d cause the T a rget Co m p an i es’ actual resu l ts to differ m ater i al l y f rom those e x pre s sed i n any for w ar d - l ook i ng state m ents . Other unkn o w n or unpred i ctab l e factors co u l d a l so have m ater i al adverse e f fects on future res u l t s . Consequent l y, readers are ca u t i oned not to p l a c e undue re li ance on for w ard - l ook i ng state m e nt s . The T a rget Co m pan i es or R i gel underta k e no ob li gat i on to update pub li c l y or re l ease any rev i s i ons to these for w ard - l ook i ng st a te m ents to ref l ect events or c i rcu m stances after the date hereof or to ref l ect the occurrence of unant i c i pated events, e x cept to the e x tent requ i red by app li cab l e l a w . R I S K F A C T O R S Th i s sect i on su m m ar i ses m any of the r i sks t h at cou l d a f fect the opera t i ons of the Target C o m pan i es or R i ge l . There m ay, h o w ever, be add i t i onal r i sks unkno w n to the Target Co m p an i es or R i gel and other r i sks, curren t l y bel i e ved to be i m m ater i a l , th a t cou l d turn out to be m ater i al . A dd i t i onal r i sks m ay ar i se or beco m e m ater i al subsequent to the date of th i s docu m ent . These r i sks, e i ther i nd i v i dua ll y or s i m u l taneous l y, cou l d s i gn i f i cant l y affect the Target Co m pan i es’ or R i ge l ’s bus i ness, operat i onal and f i nanc i al resu l ts and the pr i ce of the i r secur i t i e s . 1. Risks Related to t h e T a r get Co m pa n ies’ I n d u st r y M i n i ng co m pan i es are i ncreas i ng l y e x pected to operate i n a susta i na b l e m an n er and to p r ov i de benef i ts and m i t i gate adverse i m pacts to affe c ted co mm un i t i es. Fai l ure to do so can resu l t i n l egal suits, add i t i onal costs to add r ess soc i al or env i ron m ental i m pacts of operat i ons, i nvestor d i vest m ent, adverse reputat i onal i m pacts and l oss of “soc i al li cence to operate”, and cou l d adverse l y i m pact the Target Co m pan i es’ f i nanc i al cond i t i o n . M i n i ng c o m pan i es are su b j ect to m any r i sks re l ated to the deve l op m ent of e x i st i ng and n e w m i n i ng pr o j ects that m ay adverse l y affect the i r res u l ts o f operat i ons and pro f i ta b i l i t y . Resource e x p l orat i on and deve l o p m ent i s a s p ecu l at i ve bus i ness and i nv o l ves a h i gh degree of r i sk. M i n i ng c o m pan i es are su b j ect to e x tens i ve and rap i d l y chang i ng environ m enta l , hea l th and safety l a w s and regu l at i on s . F a il ure to co m p l y w i th these requ i re m ents cou l d resu l t i n enforce m ent proceed i ngs, c l a i m s, suspens i on o f operat i on s , co mm un i ty protest and / o r add i t i onal cap i tal or operat i ng e x pend i tures that cou l d adverse l y i m pact the Target Co m pan i es’ f i nanc i al cond i t i on or reputat i o n . C o m p li ance w i th t a i l i ngs m anag e m ent requ i r e m ents and standards, and pote n t i a l li abi l it i e s i n the event of a f a il ure to t i m e l y co m p l y w i th these requ i re m ents or an i n c i dent i nvo l v i n g a t a i l i ngs storage faci l ity, cou l d advers e l y i m pact the T a rget Co m pan i es’ f i nanc i al cond i t i on, resu l ts of operat i ons and reputat i o n . The Target C o m pan i es’ ab ili ty to re p l ace th e ir m i neral resources and reserves i s sub j ect to uncerta i nty and r i sks i nherent i n e x p l orat i o n, techn i c a l and econo m i c pre - feas i bi l ity and feas i bi l ity s tud i es and other pro j ect eva l uat i o n act i v i t i es, as w e l l as co m pet i t i on w i th i n the i ndustry for attract i ve m i n i ng propert i es. M i n i ng i s i nherent l y hazardous and the r e l at e d r i sks o f events that cause d i s rupt i ons to the Target Co m pan i es’ m i n i ng operat i ons m ay a d verse l y i m pact the env i ron m ent or the hea l t h , safety or secu r i ty of the co m pan y ’s w orkers or the l oc a l co mm un i ty, produc t i on, cash f l o w s and overa l l prof i tab ili t y . M i n i ng operat i ons and pro j ects are vu l nerable to supp l y cha i n d i s rup t i ons such that opera t i ons and deve l o p m ent pr o j ects cou l d be adverse l y a f fected by shortages o f, as w e l l as e x tended l ead t i m es to de li ver, s trate g i c spares, c r i t i cal consu m ab l es, m i n i ng equ i p m ent or m eta ll urg i cal p l ant. M i n i ng operat i ons and pro j ects are vu l nerab l e to i nfrastructure constra i nts, as w e l l as m i n i ng, geotechn i cal and process i ng r i sks. M i neral reserve and resource est i m ates are e x press i ons of j udg e m ent based on kno w l edge, e x per i ence and i ndus t ry prac t i ce. E s t i m a t es m ay change or beco m e uncerta i n w hen n e w i nfor m at i on beco m es ava il ab l e on the te n e m ents through ad d i t i onal e x p l orat i on, i nvest i gat i ons, research, test i ng or eng i neer i ng over the li fe of a pro j ect. M i n i ng co m pan i es face strong co m pet i t i on and i ndustry conso li dat i o n . 2. Risks Related to t h e T a r get Co m pa n ies’ O p e r ati o n s a n d B u si n ess The T a rget C o m pan i es’ operat i ons are vu l nerab l e to i n f rastru c ture constr a i nt s , i n c l ud i ng i n cage ho i st i ng and p l ant capac i ty. D e l ays or fa i l ures i n de w ater i ng of f l ooded underground w ork i ng areas w il l i m pact negat i ve l y on the acces s i b i l i t y , as w e l l as the re - equ i pp i n g and re - estab li sh m ent of the w ork i ngs. The t i m e and costs assoc i ated w i th access i ng w ork i ng p l aces i s based on assu m pt i ons and cou l d have been under - est i m ated. The Target C o m pan i es’ operat i ons are vu l n e rab l e to m i n i ng r i sk, i n c l ud i ng not ach i ev i ng p l anned face advance, de l ays i n produ c t i on as a result of se i s m i c i ty, under - perf o r m i ng a ga i nst the m i ne p l an, not ach i e v i ng p l anned se l ect i ve b l ast m i n i ng eff i c i enc i es w i th regards to face advance, go l d l oss and d il ut i on, and not ach i ev i ng p l anned product i on ra m p - up and not m a i nta i n i ng steady - state product i o n . The Target Co m pan i es’ operat i ons are vu l nerab l e to process i ng r i sk, i nc l ud i ng not ach i ev i ng p l anned product i on throughput and recover i es, as w e l l as i nsuff i c i ent ta ili ngs storage fac ili ty capac i ty. The Target Co m pan i es’ operat i ons are v u l ne r ab l e to f i nanc i al and l egal r i sks, w h i ch m ay l ead to d i srup t i on or suspens i on of the Target C o m p a n i es’ operat i ons and / or i m pos i t i on of f i nes. There can be no assurance that there w il l be su f f i c i ent ca p i t a l pro v i s i on o r that operat i ng costs w il l not e x ceed budgeted costs. The Target Co m pan i es’ i nab ili ty to reta i n i ts sen i or m anage m ent m ay have an adverse effect on the i r bus i ness.

R i sk Factors C ont’d The Target Co m pan i es c o m p ete w i th m i n i ng and other co m p a n i es for key hu m an resources w i th cr i t i cal ski l l s and i ts i nabi l i ty to r e ta i n k e y personnel or s u f f i c i ent “H i st o r i c a ll y D i sadvantaged S outh A fr i cans” (H DSA ) representat i o n i n m anag e m ent pos i t i ons cou l d have an adverse effect on the i r bus i ness. Increased l abour costs cou l d have a m ater i al adverse effect on the Target Co m pan i es’ resu l ts of operat i ons and f i nanc i al cond i t i o n . The use of contractors at certa i n of the Target Co m pan i es’ operat i ons m ay e x pose the Target Co m pan i es to de l ays or suspens i ons i n m i n i ng act i v i t i es and i ncreased m i n i ng costs. A rt i sanal and ill egal m i n i ng m ay occur on the Target Co m pan i es’ propert i es, w h i ch can d i srupt the Target Co m pan i es’ bus i ness, have adverse env i ron m enta l , hea l th, safety and secur i ty i m pacts, and e x pose the Target Co m pan i es to li ab ili t y . The T a rget Co m p a n i es have been e x posed t o secur i ty r i sks, i n c l ud i ng the f t of g o l d and gold - bear i ng m ater i a l , and m ay cont i nue to be e x posed i n the future. Increased secu r i ty - re l a t ed e x p end i tures or m ater i a li za t i on of secu r i ty r i sks m ay l ead to i ncreased operat i onal e x penses and have a m ater i al adverse effect on the Target Co m pan i es’ resu l ts of operat i ons and f i nanc i al cond i t i o n . G i ven the nature of m i n i ng and the type of m i nes w e operate, w e face a m ater i al r i sk of li ab ili ty, de l ays and i ncreased cash costs of product i on from env i ron m ental and i ndustr i al acc i dents and po ll ut i on co m p li ance breaches. Fa il ure to m odern i se operat i ons m ay have a m ater i al adverse effect on the Target Co m pan i es’ bus i ness. T i t l e to the Target Co m pan i es’ propert i es, w h il st current l y secured i n l a w , m ay be sub j ect to cha ll eng e . The out b reak of the CO V ID - 19 pande m i c and the preva l ence o f HI V / A IDS has had and m ay cont i nue to have a m ater i al adverse effe c t on the Target Co m p a n i es’ bus i ness, f i nanc i a l cond i t i on, and res u l ts of operat i on s . A ny fut u re ep i de m i cs m ay a l so have s i m il ar, or m ore severe, effects on g l obal econo m i c act i v i ty and on the i r bus i ness, resu l ts of operat i ons or f i nanc i al cond i t i o n . The Target Co m pan i es’ operat i ons are sub j ect to var i ous c li m ate change - re l ated phys i cal r i sks w h i ch m ay adverse l y i m pact i ts product i on act i v i t i es, m i ne s i tes and personnel and/or resu l t i n resource shortages or env i ron m ental da m ages. The Target Co m pan i es’ operat i ons are reg i ona ll y concentrated, d i srupt i ons i n these reg i ons cou l d have a m ater i al adverse i m pact on the operat i ons and f i nanc i al cond i t i on of the bus i nes s . M any of the f i nanc i a l and operat i onal f i gures i nc l uded i n th i s present a t i on re l ate s o l e l y to t he ta i l i ngs bus i ness of Gauta Tai l i ngs and t h e m i n i ng bus i ness of B l yvoor Go l d and m ay not be ref l e c t i ve o f the f i nanc i al and operat i o nal pro j ect i ons of the Targ e t C o m pan i es overa ll . 3. Risks Related to t h e T a r get Co m pa n ies’ O p e r ati o n s a n d B u si n ess The Target Co m pan i es have at present and e x pect to have s i gn i f i cant f i nanc i ng requ i re m ents from t i m e to t i m e and m ay i ncur substant i al add i t i onal i ndebtedness i n the future, w h i ch cou l d adverse l y i m pact the i r bus i ness. S a l es of l arge quantit i es of the Targ e t Co m p an i es ord i n a ry shares or s i m il ar secu r i t i es, o r the percep t i on th a t these sa l es m ay occur or other di l u t i on of the Target C o m pan i es’ equ i ty, cou l d adverse l y affe c t the prev a i l i ng m arket p r i ce o f the Target Co m pan i es’ secur i t i es. The Target Co m pan i es m ay not pay d i v i dends or m ake s i m il ar pay m ents to shareho l ders i n the future. There can be no assurance that the Target C o m p a n i es w il l be ab l e to support the carr y ing a m ount of the i r prope r ty, p l ant and equ i pm ent, i ntang i b l e assets and good w il l on the ba l ance sheet. I f the ca r ry i ng a m ount of their assets i s n o t recoverab l e , the Targ e t Co m pan i es m ay be requ i red to recogn i se an i m pa i r m ent charge, w h i ch cou l d be m ater i a l . W e are sub j ect to the i m pos i t i on of var i ous regu l atory costs, such as m i n i ng ta x es and roya l t i es, changes to w h i ch m ay have a m ater i al adverse effect on our operat i ons and prof i ts. A ny do w ngrade of cred i t rat i ngs ass i gned to the Target Co m pan i es’ debt secur i t i es cou l d i ncrease future i nterest costs and adverse l y affect the ava il ab ili ty of new debt f i nanc i n g . A ny acqu i s i t i on or acqu i s i t i ons that the Target Co m pan i es m ay co m p l ete m ay e x pose them to new geograph i c, po li t i ca l , l ega l , soc i a l , operat i ng, f i nanc i al and geo l og i cal r i sks. The occu r rence o f events for w h i ch the Targ e t Co m pan i es are not i nsured or f o r w h i ch th e ir i nsurance i s i nadequate m ay adverse l y a ff e ct cash f l o w s and overa l l pr o fitabi l ity. There c an be no assurance that the T a rget C o m pan i es’ i nsurance coverage w il l adequately sat i sfy a l l potent i al c l a i m s i n the future. 4. M a r ket Risks The pr i ce of go l d, the Target Co m pan i es’ pr i nc i pal product, and other co mm od i ty m arket pr i ce f l uctuat i ons cou l d adverse l y affect the prof i tab ili t y of operat i ons. The prof i tab ili ty of m i n i ng co m pan i es’ operat i ons and the cash f l o w s generated by these operat i ons are s i gn i f i cant l y affected by f l uctuat i ons i n i nput product i on pr i ces, so m e of w h i ch are li nked to the pr i ces of o i l and stee l . G l obal po li t i cal and econo m i c cond i t i ons cou l d adverse l y affect the Target Co m pan i es’ prof i tab ili ty of operat i ons. Inf l at i on m ay have a m ater i al adverse effect on resu l ts of operat i ons. 5. Ot h er Re g u lato r y a n d Legal Risks Fai l ure to co m p l y w i th l a w s, regu l a t i ons, s t a ndards and contractual ob li g a t i ons, breaches i n governance processes or fraud, b r i bery a nd corrupt i on m ay l ead to regu l atory pena l t ie s , l oss o f li cences or per m i ts, negat i ve e ff e cts on the Targ e t C o m pan i es’ reported f i nanc i al resu l ts, and adverse l y affect the i r reputat i o n . The m i neral r i ghts are sub j ect to l eg i s l a t i on, wh i ch cou l d i m pose s i gn i f i ca n t costs and bu r dens and w h i ch i m pose certa i n o w n ersh i p r e qu i re m ents, the i nter p reta t i on of w h i ch i s the sub j ect of d i sput e . Changes to th i s l eg i s l a t ion cou l d adverse l y i m pact the Target Co m pan i es’ resu l ts of operat i ons and f i nanc i al cond i t i o n . The Target Co m pan i es have been, are curr e nt l y, and m ay fr o m t i m e to t i m e be i nvo l ved i n l ega l , tax or regu l a tory proceed i ngs o r d i s p utes and to he i g h tened r i sk of c l a i m s aga i nst the m , w h i ch cou l d have an adverse i m pact on the T a rget Co m p a n i es’ reputat i on, prof i tab ili ty and conso li dated f i nanc i al pos i t i on and l ead to i ncreased l egal e x penses and a w ards aga i nst the Target Co m pan i e s . Co m p li ance w i th e m erg i ng c li m ate change - re l ated requ i re m ents cou l d resu l t i n add i t i onal costs and e x pose the Target Co m pan i es to add i t i onal li ab ili ties. Increas i ng s c rut i ny and chang i ng e x pectat i o n s from the Target C o m pan i es’ stakeho l ders, inc l ud i ng co mm un i t i es, govern m ents and NGOs as w e l l as i nvest o rs, l enders and other m arket pa r t i c i pants, w i th respect to the Target C o m p a n i es’ E nv i ro n m enta l , S oc i al and Governance perfor m ance and po li c i es m ay i m pact the Target Co m pan i es’ reputat i on, resu l t i n add i t i onal costs to m eet the e x pectat i ons of stakeho l ders, h i nder access to cap i tal or e x pose the Target Co m pan i es to add i t i onal r i sks, i nc l ud i ng d i s i nvest m ent and li t i gat i o n .

R i sk Factors C ont’d B reaches i n cybersecur i ty and v i o l at i ons of data protect i on l a w s m ay adverse l y i m pact or d i srupt the Target Co m pan i es’ bus i ness . U . S . secur i t i es l a w s do not requ i re the Tar g et C o m pan i es to d i s c l ose as m uch i nfor m at i on to i nvestors as a U . S . i s s u e r i s req u i red to d i s c l os e , and i nvestors m ay rece i ve l ess infor m at i on about the Target C o m p an i es than they m i ght other w i se rece i ve from a co m parab l e U . S . co m pany . The scope of due d i l i gence R i gel has cond u cted i n con j unct i on w i th the P roposed C o m b i nat i on m ay be d i fferent than w ou l d typ i ca ll y be conducted i n the event the Target Co m p a n i es pursued an under w r i tten pub li c off e r i ng, and you m ay be l ess protected as an i nvestor from any m ater i al i ssues w i th respect to the Target Co m pan i es’ bus i ness. 6. Risks Related to S o u th A f r ica The Target Co m pan i es’ m i neral depos i ts, m i neral resources and reserve s , and m i n i ng operat i ons are l ocated i n a country w here po li t i cal, tax and econ o m i c la w s and po li c i es m ay ch a nge rap i d l y and unpred i c tab l y and such changes and po li c i es, i n c l ud i ng w i th respect to f i nanc i al prov i s i on i ng for rehab ili tat i on, m ay adverse l y affect both the ter m s of the i r m i n i ng r i ghts and concess i ons, as w e l l as the i r ab ili ty to conduct operat i ons. The T a rget Co m pan i es’ operat i ons are su b j e ct to w ater use li cences . A lthough the Target C o m p a n i es are operat i ng i n accordance w i th gover n m ent depar t m ental rec o mm endat i ons and has app li ed for a new water use li cense, they are curren t l y operat i ng w i thout a va li d w ater use l i cense, w h i ch cou l d res u l t i n f i nes, sanct i ons and penalt i es f rom the co m petent autho r i t i es or suspen s i on of the Targ e t Co m pan i es’ operat i ons and have a m ater i al adverse e ffect on the Targ e t Co m pan i es’ b u s i ness, oper a t i ng results and f i nanc i al cond i t i o n . The Target C o m pan i es’ m i neral resources a n d reserves, depo s i ts and m i n i ng opera t i ons a r e l ocated i n a coun t ry that faces i n s tabi l ity, p u b li c he a l th and secu r i ty r i sks that m ay adverse l y a f fect b o th the ter m s of their m i n i ng r i ghts and concess i ons, as w e l l as the i r abi l ity to conduct operat i ons. The preva l ence of occupat i onal hea l th d i seases and other d i seases and the potent i al costs and li ab ili t i es re l ated thereto m ay have an adverse effect on the bus i ness and resu l ts of operat i ons of the Target C o m pan i es . S i nce the Target Co m pan i es’ l abour force h a s substan t i al t rade un i on pa r t i c i pat i o n , they f a ce i ncreased r i sk o f d i srup t i on from l abour d i s putes and a m en d m ents to S outh A f r i can l ab o ur l a w s. Labour unrest, u n i on ac t i vity, ac t i v i s m and d i srupt i ons ( i n c l ud i ng protra c ted stoppages) have had and cou l d have a m ater i al adverse effect on the Target Co m pan i es’ resu l ts of operat i ons and f i nanc i al cond i t i o n . The Target Co m pan i es’ m i neral r i ghts i n S outh A fr i ca cou l d be a l tered, suspended or cance ll ed for a var i ety of reasons, i nc l ud i ng breaches i n the i r ob li gat i ons i n respect of such m i n i ng r i ghts . Fore i gn e x change f l uctuat i ons and S outh A fr i can control e x change regu l at i ons m ay constra i n the Target Co m pan i es’ f i nanc i al f l e x i b ili ty, w h i ch cou l d have a m ater i al adverse effect on the Target Co m pan i es’ resu l ts of operat i ons and f i nanc i al cond i t i o n . Fa il ure to co m p l y w i th the requ i re m ents of the B roa d - based S oc i o - econo m i c E m po w er m e nt Charter 2018 cou l d have an adverse effect on the Target Co m pan i es’ bus i ness, operat i ng resu l ts and f i nanc i al cond i t i on of the i r operat i ons. The tax fra m e work i n S outh A fr i ca i s co m p le x w i th respect to m i neral a c t i v i t i es, i n c l ud i ng i n w i th reference to m i n i ng royalt i es, r i ng - fen c i n g of unredee m ed cap i tal e x pend i ture, re - ass e s s m ent of unredee m ed cap i tal e x pend i ture by the SA R S , and poten t i al tax ref o rm or draft a m end m ents to the I T A , w h i ch cou l d have an adverse effect on the bus i ness, operat i ng resu l ts and f i nanc i al cond i t i on of the Target Co m pan i es’ operat i ons. F l uctuat i ons i n the e x change rate of the S outh A fr i can currency m ay reduce the m arket va l ue of the Target Co m pan i es’ secur i t i es, as w e l l as the m arket va l ue of any d i v i dends or d i str i but i ons pa i d by the Target Co m pan i es. E nergy cost i ncreases, and po w er f l uctuat i ons and stoppages cou l d adverse l y i m pact the Target Co m pan i es’ resu l ts of operat i ons and f i nanc i al cond i t i o n . A further do w ngrade of S outh A fr i ca’s cred i t rat i ng m ay have an adverse effect on the Target Co m pan i es’ ab ili ty to secure f i nanc i n g . 7. R isks R elated to t h e Pr oposed C o m bi n ation E vents, changes and c i rcu m stances w h i ch are or m ay be beyond the control of the Target Co m pan i es’ and R i gel Resource A cqu i s i t i on Corp m ay g i ve r i se to the ter m i nat i on of negot i at i ons and subsequent def i n i t i ve agree m ents re l ated to the P roposed Co m b i nat i o n . The consu mm at i on of the P roposed Co m b in at i on i s e x pected to be sub j ect to a nu m ber of cond i t i ons, so m e of wh i ch w il l beyond the control of the Targ e t Co m p a n i es and R i gel Resource A cqu i s i t i on Corp, i nc l ud i ng the a p proval of the sh a reho l ders and v a r i ous regu l atory author i t i es. If those cond i t i ons are not m et or w a i ved, the P roposed Co m b i nat i on m ay not occu r . The Target Co m pan i es’ operat i ons m ay be restr i cted dur i ng the pendency of the P roposed Co m b i nat i on pursuant to ter m s of the B us i ness Co m b i nat i on A gree m ent . A n aff i l i ate of R i g e l ’s sponsor m a i nta i ns i nte r ests re l ated to a subs i d i ary of A urous Resources, i n c l ud i ng a non - control l i ng shareho l d i n g i nteres t . In case of a con f li c t of i n terest be t ween the sponsor and A urous Res o urces, the sponsor m ay g i ve pr i or i ty to i ts o w n i nterests, w h i ch m ay i n turn i m pact the f i nanc i al cond i t i on, operat i ons and prof i tab ili t y of A urous Resources and i ts subs i d i ar i e s . S o m e of R i ge l ’s e x ecut i ve o f f i cers and direc t ors m ay have conf li c ts of i n terest that m ay i n f l uence or have i n f l uenced them to support o r approve the P roposed Co m b i nat i on w i thout regard to i nvestors’ i n terests or i n deter m i n i ng w hether the Target C o m pan i es are appropr i ate targets for R i ge l ’s i n i t i al bus i ness co m b i nat i o n . B oth R i gel and the Target Co m pan i es w il l i ncur s i gn i f i cant transact i on costs i n connect i on w i th the P roposed Co m b i nat i o n . There can be no assurance as to the t i m i ng of the co mm ence m ent or co m p l et i on of the SE C rev i ew of the pro x y state m ent/prospectus re l at i ng to the P roposed Co m b i nat i on, w h i ch i n turn w il l deter m i ne the t i m i ng of the c l os i ng of the P roposed Co m b i nat i o n . The l egal arch i tecture of the P roposed C o m b i nat i on m ay g i ve r i se to unant i c i pated or adverse tax consequences, i nc l ud i ng to R i gel R esource A cqu i s i t i on C orp’s shareho l ders . The ab ili ty of R i ge l ’s pub li c shareho l ders to e x erc i se rede m pt i on r i ghts w i th respect to a s i gn i f i cant port i on of i ts C l ass A shares cou l d i ncrease the probab ili ty that the P roposed Co m b i nat i on w il l be unsuccessfu l . B ecause R i gel i s, and the resu l t i ng pub li c ent i ty w il l be, i ncorporated under the l a w s of the Cay m an Is l ands i nvestors m ay face d i ff i cu l ties i n protect i ng the i r i nterests, and the i r ab ili ty to protect the i r r i ghts through the U . S . federal courts m ay be li m i ted. S ecur i t i es of co m pan i es for m ed through bus i ness co m b i nat i ons such as the resu l t i ng pub li c ent i ty m ay e x per i ence a m ater i al dec li ne i n pr i ce re l at i ve to the share pr i ce of the i r pub li c shares pr i or to the bus i ness co m b i nat i o n . If R i gel i s dee m ed to be an i nve s t m ent c o m p any for p u rposes of the Invest m ent C o m p any A ct, i t w ou l d be requ i red to i n s titute burdens om e c o m p li ance requ i re m ents and i ts a c t i v i t i es w ou l d be severe l y res t r i c ted and, as a resu l t , i t m ay be requ i red to w i nd up, redeem and li qu i dat e .

R i sk Factors C ont’d 8. Risks Related to Bei n g a P u blic Co m pa n y The T a rget C o m pan i es’ appo i n t m ent of a n e w reg i stered i ndependent account i ng firm cou l d resu l t i n add i t i onal costs and dif f i cu l t i es i n co m p l y i ng w i th regu l at i ons govern i ng pub l i c c o m pany corporate governance i nc l ud i ng repor t i ng de l ays i n the fi li ng of i ts reports w i th the SE C, and the Target Co m pan i es’ reg i stered i ndependent account i ng f i rm m ay i nterpret account i ng ru l es d i fferent l y from i ts for m er f i r m , w h i ch cou l d adverse l y i m pact i ts bus i ness. Fai l ure to co m p l y w i th requ i re m ents to des i gn, i m p le m ent and m a i nta i n effe c t i ve i ntern a l control over f i nan c i al repo r t i n g , i n c l ud i ng S ect i o n 404(a) of the S arbanes - O x l ey A ct, cou l d h a ve a m ater i al adverse effe c t on the result i ng pub li c en t i ty’s bus i ness and stock pri c e and i nvestors’ conf i dence on the re li ab ili ty of i ts f i nanc i al state m ents. N Y S E m ay de li st R i ge l ’s o r the resu l t i ng pub l ic en t i ty’s sec u rit i es f rom trad i ng on its e x cha n ge, w h i ch cou l d l i m i t i nve s tors’ abi l i ty to m ake t ransact i ons i n R i ge l ’s or the result i ng publ i c ent i ty’s securit i es and sub j ect R i gel or the re s u l t i ng publ i c e n tity to add i t i onal t rad i n g restr i ct i ons. A n act i ve trad i ng m arket for the equ i ty secur i t i es m ay not deve l op or m ay not be susta i ned to prov i de adequate li qu i d i t y . The resu l t i ng pub li c ent i ty cou l d be the sub j ect of secur i t i es c l ass act i on li t i gat i on due to future stock pr i ce vo l at ili ty, w h i ch cou l d d i vert m anage m ent’s attent i on and m ater i a ll y and adverse l y affect our bus i ness, f i nanc i al pos i t i on, resu l ts of operat i ons and cash f l o w s. Future sa l es of equ i ty secur i t i es by e x i st i ng shareho l ders or by the resu l t i ng pub li c ent i ty, or future d il ut i ve i ssuances of equ i ty secur i t i es by the group, cou l d adverse l y affect preva ili ng m arket pr i ces for the equ i ty secur i t i es. The quarter l y resu l ts of operat i ons m ay f l uctuate and as a resu l t, the group m ay fa i l to m eet or e x ceed the e x pectat i ons of i nvestors or secur i t i es ana l ysts, w h i ch cou l d cause the share pr i ce to dec li n e . Fol l o w i ng the cons u m m at i on of the P ropos e d C o m b i nat i on, the resu l t i ng publ i c en t i ty w il l i ncur s i gnif i cant i n c reased e x penses and a d m i n i strat i ve burdens as a publ i c co m pany, wh i ch cou l d have an adverse e ffe c t on its bu s iness, f i nanc i al con d i t i on and results of operat i ons. Concentrat i on of o w nersh i p of the result i ng pub li c entity a m ong m e m bers of the Target C o m pan i es’ and R i ge l ’s sen i or m a n ag e m ent, e x i st i ng directors and p r i nc i p a l s tockho l ders m ay prevent new i nvestors from i nf l uenc i ng s i gn i f i cant corporate dec i s i ons and their i nterests m ay be d i fferent fro m , or i n add i t i on to, i nvestors’ i nterests. R i gel i s , and the result i ng publ i c en t i ty w i ll be, an “e m erg i ng gro w th c o m pany” and a “fore i gn pr i vate i ssuer” and, as a resu l t of the reduced d i sc l osure and governance requ i re m ents app li cab l e to such co m pan i es, i ts secu r i t i es m ay be l ess attrac t i ve to i nvestors and it m ay be m ore d i ff i cu l t to co m pare the resu l t i ng pub li c ent i ty’s perfor m ance to the perfor m ance of other pub li c co m pan i e s . T h e r isks desc r i b e d ab o v e a r e n ot t h e o n ly r isks fac e d by t h e Ta r get Co m pa n ies a n d Rige l . Y ou s h o u l d al s o ca r ef u lly r e v iew t h e sect i o n s e n ti t l e d “Ris k F a c t o r s ” a n d “Ca u t i o n a r y Note Re g a r di n g F o r wa r d - L oo k i n g S t a t e m e n t s ” in t h e f i li n gs t h at Rig e l h as m ade a n d will m ake a n d ot h er fili n gs t h at will be m ade with t h e U . S . S ec ur ities a n d E xc h a n ge Co mm issi o n .