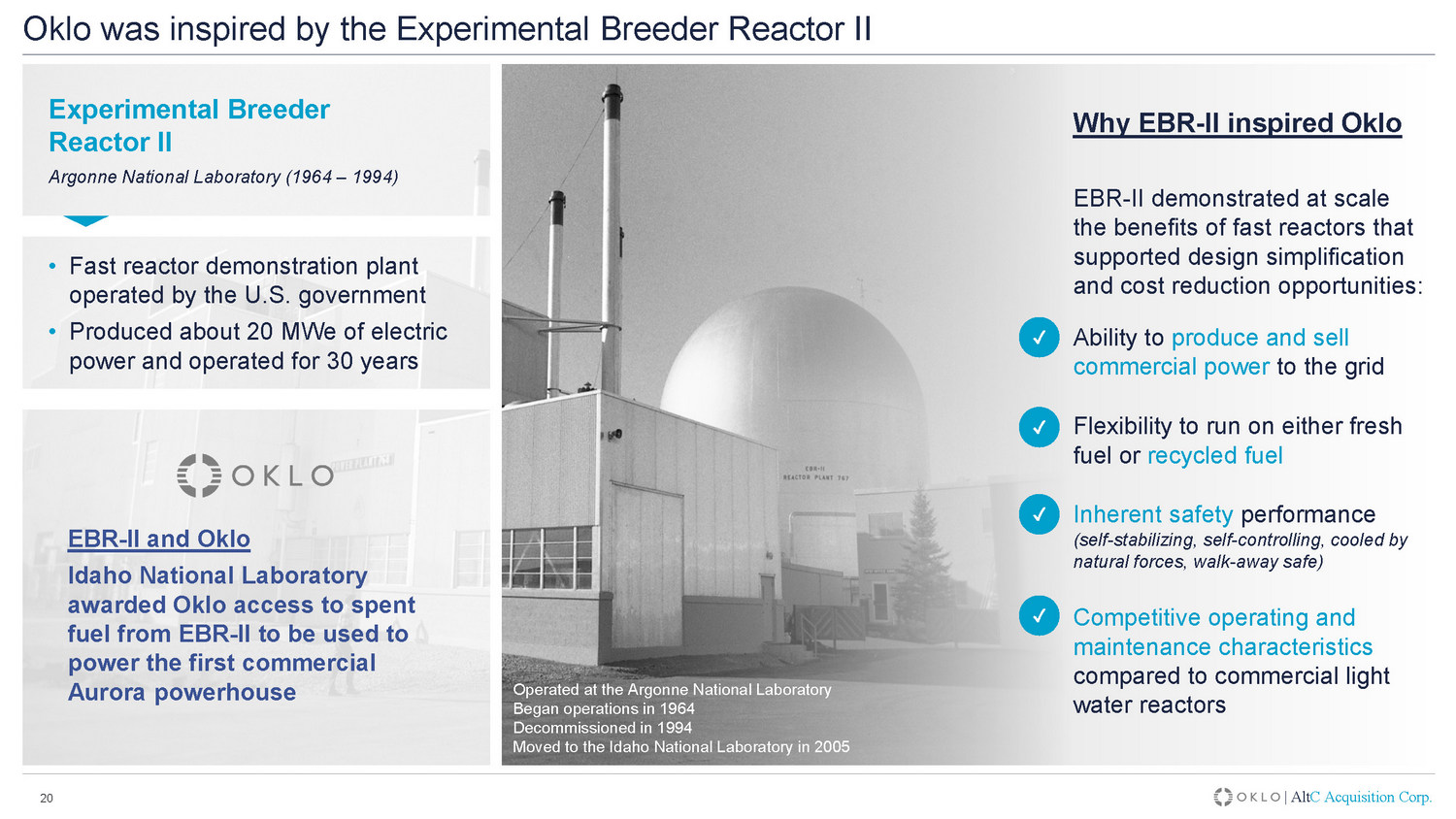

|Alt C收購公司20 Oklo的靈感來自於實驗增殖反應堆II實驗增殖反應堆II阿貢國家實驗室(1964-1994)·由美國政府運營的快堆示範工廠·生產約20兆瓦電力並在阿爾貢國家實驗室運營了30年於1964年開始運營1994年退役2005年轉移到愛達荷州國家實驗室為什麼EBR-II啟發Oklo EBR-II大規模展示了支持設計簡化和降低成本機會的快速反應堆的好處:能夠生產商業電力並向電網出售商業電力燃料或回收燃料固有的安全性能(自穩定,與商用輕水反應堆相比,✓✓✓eBR-II和奧克洛愛達荷州國家實驗室獲得了OKLO獲得eBR-II乏燃料的合同,用於為第一座商用奧羅拉核電站提供動力

|Alt C Acquisition Corp.備註:(1)Oklo最初的重點是設計和部署15兆瓦和50兆瓦的工廠規模。(2)目標工廠成本和建設時間反映了實現第一次部署後的預期運行率操作,並依賴於當前對時間和成本的假設,這些假設可能會在監管過程中發生變化。(3)包括應急規劃區,對於URORA反應堆,預計將被限制在發電廠建築結構內。21簡化、現代化的設計方法,支持簡化部署Aurora Powerhouse設計,旨在降低工廠複雜性、成本和建設時間

|Alt C Acquisition Corp.來源:能源部-商業起飛之路:高級核報告(2023年3月),高級核能系統中心。注:(1)目標工廠成本和建設時間表反映了實現第一次部署後的預期運行率運營,並取決於當前對時間和成本的假設,這些假設可能會在監管過程中發生變化。(2)根據能源部的分析,先進反應堆的隔夜資本成本為3,600美元/千瓦。(3)以AP-1000為基礎的隔夜資金成本。22通過降低產品複雜性和成本實現所有者-運營商模式Oklo打算建造、擁有和運營Aurora發電站-反應堆設計實現了成本、土地、材料和施工時間優勢更低的預期工廠成本更小的佔地面積更低的複雜性快速安裝獨特的商業模式15 MWe工廠產能(技術可能擴展到50 MWe)x

|Alt C Acquisition Corp.備註:(1)本文描述的單位經濟,包括任何潛在的利潤率上升,是前瞻性信息,不應被依賴為一定指示未來結果。實際結果可能會有很大不同。(2)反映截至2023年7月7日來自FactSet的Mark ET資本化。23有吸引力的商業模式預計將產生引人注目的經常性收入Oklo正在全球電力市場追求一種廣泛使用的收入模式,根據長期合同出售電力股東機會收入模型在市場上得到驗證Oklo對股東的價值主張x大型市場機會-Oklo的目標是未解決的分散電網使用案例(例如,數據中心、國防)x預計將反覆出現並隨時間增長的長期合同收入x收入來源不能被競爭對手脱媒x工廠運營第一年的預期盈利單位經濟(1)x高重複性以推動單位增長並推出更高的產出版本(例如,50兆瓦)x燃料回收可以提供潛在的未來利潤率提升和新的收入來源國家重點市場價值(2)丹麥加拿大法國風能多樣化風能/太陽能約400億美元~140億美元~50億美元~50億美元~30億美元~20億美元葡萄牙風能/太陽能約200億美元

|Alt C Acquisition Corp.注:(1)假設所有監管部門都已在預期時間內獲得批准。監管過程,包括NCESary NRC的批准和許可,是一個漫長而複雜的過程,預計的時間表可能與獲得所有必要批准所需的實際時間有很大不同。假設15兆瓦和50兆瓦的e A urora發電站的資本成本分別為2,400萬美元和6,100萬美元,每個發電站的壽命為40年。假設每個都處於NOAK狀態。單位經濟效益是以實值表示的。此外,此處提供的單位經濟性僅用於説明目的。實際結果可能大不相同。有關更多詳細信息,請參閲幻燈片37-40。24具有潛在上升潛力的令人信服的預期機組經濟性説明性機組經濟性:15 Mwe Aurora發電廠(1)累計40年機組經濟性(百萬美元)$288$198$1,452$1,163$966來自電力銷售的收入運營費用工廠利潤資本成本工廠現金流資本成本累積$198 80%5.0x$120$107$508$388$281來自電力銷售的收入營運開支工廠利潤資本成本工廠現金流成本累積$107·初始工廠成本:$24·初始燃料成本:$33·加油成本:$50 75%2.5x説明性機組經濟性:50我們奧羅拉發電廠(1)累積40年機組經濟性經濟學(百萬美元)·初始工廠成本:61美元·初始燃料成本:55美元·加油成本:82 75%2.5倍工廠潛在壽命利潤率潛在現金流與資本成本潛在上行槓桿:x燃料回收x投資税收抵免80%5.0x工廠潛在利潤率潛在工廠現金流與資本成本潛在上行槓桿:x燃料回收x投資税收抵免

|Alt C Acquisition Corp.25優勝價值主張旨在加速客户採用OKLO價值主張旨在加速客户採用超過700兆瓦的非約束性意向潛在客户OKLO目標市場客户希望□購買電力,而不是擁有/運營滿足環境和運營目標的工廠□低資本支出解決方案□獲得負擔得起且可靠的無碳能源□經驗證的技術具有低執行和運營風險OKLO價值主張x潛在的零前期客户成本,加速採用x可靠、負擔得起的長期合同下的零排放能源,全球電力市場經過驗證的標準模式x已在大規模數據中心、國防工廠、工業離網/農村公用事業✓✓✓與潛在客户積極對話的底層技術

|Alt C Acquisition Corp.26向愛達荷州國家實驗室的部署地點推進了三個令人興奮的項目,並確保了15兆瓦核電站的初始燃料負荷。有機會在南俄亥俄州愛達荷州國家實驗室奧羅拉發電站(15兆瓦)1奧克洛與美國能源部簽署一份諒解備忘錄,在愛達荷州國家實驗室向奧克洛發放現場使用許可證愛達荷州國家實驗室向奧克洛2017 2019 2021 2024 2024-26 2026/27 2020奧克洛獲得美國能源部現場使用許可奧羅拉發電站定向申請接受審查(1)預計國家能源局對奧克洛供應鏈發展的審查期,目標是第一個電力生產燃料安全✓場地確定✓x與南俄亥俄州多樣化倡議(SODI)的合作伙伴關係(2)5月18日宣佈2023年x在南俄亥俄州部署兩個商業奧克洛發電廠的非約束性承諾確定了✓·工廠預計將提供清潔電力和供暖,並有機會擴大·這些工廠支持該地區創造就業機會,通過經濟多元化和推進清潔能源解決方案,進一步推動SODI的使命,以改善俄亥俄州南部社區的生活質量·SODI由美國能源部核能辦公室提供資金,以支持部署先進的反應堆技術和使用前俄亥俄州核電站遺址南俄亥俄州多元化倡議兩座Aurora發電站(各15 MWe)2-3注:(1)美國核管理委員會(NRC)。(2)南俄亥俄州多樣化倡議(SODI)的使命是通過經濟多樣化、開發能源部朴茨茅斯(DOE)朴茨茅斯天然氣擴散廠址未得到充分利用的土地和設施,以及繼續支持當地政府,改善傑克遜縣、派克縣、羅斯縣和肖託縣的生活質量。

|Alt C Acquisition Corp.27正在進行密集的監管工作,以支持首次部署Oklo是所有高級、非輕水反應堆公司首次提交的先進反應堆聯合許可證申請x 2016年開始的NRC項目x 2020年3月提交的Cola x在2020年至2022年可樂審查過程中與NRC工作人員的深度接觸x利用寶貴經驗成功提交下一份申請x NRC批准了Oklo的質量保證計劃説明正在緊張的工作中準備下一次申請提交x大幅擴大許可和監管團隊以引入內部前NRC工作人員和監管專家-Oklo現有員工中近10%是前NRC員工x經常參與2022-23-9年度就關鍵許可主題舉行的正式申請前會議-舉行了70多次協調會議-共享了50多份許可文件x Oklo打算在2024年進行申請前審核x 2024年底/2025年初提交申請x Oklo對NRC工作人員的辛勤工作和推進安全核解決方案的承諾深表讚賞·可口可樂是NRC的許可途徑,結合了建設許可和運營許可證·Oklo是歷史上第一家將可口可樂提交NRC審查的先進反應堆公司·2022年,NRC拒絕了Oklo‘s Cola,要求提供更多信息以恢復審查·Oklo在審查過程中獲得了寶貴的經驗,並利用NRC的迴應來增強其監管模式

|ALTC Acquisition Corp.備註:(1)美國能源信息管理局(鈾營銷年度報告-2022年)。(2)能源部(關於乏核燃料的5個快評)。28燃料回收上行機會奧克洛大量乏燃料庫存奧克羅設計優勢獨特的上行機會燃料供應限制美國目前依賴進口新鮮核燃料2022年,美國核電站95%(1)的鈾來自外國來源✗,美國核電站33%(1)的鈾濃縮服務從俄羅斯購買✗美國限制了HALEU的生產,什麼是先進反應堆的燃料有限美國的燃料能力是先進反應堆發展的一個緊迫問題美國擁有大量且不斷增加的乏燃料庫存✗管理成本高昂✗美國反應堆自1950年以來產生了90,000噸乏燃料(2)✗每年產生2,000噸乏燃料(2)✗乏燃料目前儲存在35個州的70個反應堆地點(2)乏燃料管理複雜;隨着新反應堆的部署,需求將會增加,乏燃料保持其能源潛力,可以回收x燃料可以回收,並在其他國家這樣做,例如法國x被現有反應堆使用後,90%以上的潛在能源仍留在乏燃料中(2)✗美國目前沒有回收燃料的機會來解決燃料供應限制和乏燃料庫存的循環快速反應堆可以使用新鮮或回收燃料x ebr-II展示了快堆使用回收燃料的能力x Oklo工廠設計靈活地使用新鮮或回收燃料x第一座以從ebr-ii回收的乏燃料為燃料的極光發電廠燃料回收可以提供未來的利潤率提升和新的收入來源Oklo正在開發燃料回收能力x廢物轉化為清潔能源x選定在與能源部合作開發燃料回收技術的四個項目中,初步計劃是到2030年在美國建立商業規模的燃料回收設施。S·奧克洛有可能在燃料回收領域引領行業

|ALTC Acquisition Corp.美國核電站嚴重依賴進口核燃料核燃料進口|ALTC Acquisition Corp.29美國核電站的鈾來源(氧化鈾,百萬磅)(1)注:(1)美國能源信息管理局(核解釋-我們的鈾來自哪裏)。(2)美國能源情報署(UEA)(鈾營銷年度報告-2022年),(3)Orano(所有關於廢燃料加工和回收的信息)。不斷髮展的地緣政治擔憂2022年,美國核電站95%(2)的鈾來自國外2022年,美國核電站所需的外國鈾濃縮服務的33%(2)從俄羅斯購買0 20 40 60 80 1950 1960 1970 1970 1980 1990 2000 2010 2020國內生產購買進口燃料回收可能會減少美國的進口美國目前不回收乏燃料然而,燃料可以回收,而且在其他國家也可以回收,例如法國近十分之一的燈泡使用回收的核材料(3)

|Alt C Acquisition Corp.30燃料回收可以提供潛在的未來利潤率提升和新的收入來源潛在的機會建立和運營設施,向Aurora發電廠以及第三方客户供應回收燃料乏燃料回收對Oklo來説是一個重要的潛在成本節約機會,可以降低工廠初始資本成本和持續運營成本垂直整合的燃料來源將提供安全和保證Oklo的回收方法使用煙火處理,這是一項成熟的技術通過銷售乏燃料管理服務以及向各種終端市場銷售副產品和特種同位素來增加潛在收入來源燃料回收解決了市場上長期存在的問題,並可以創造可持續的競爭優勢2023年1月,Oklo向核管理委員會提交了一份商業規模的燃料回收設施許可項目計劃燃料回收如何工作通過電化學分離燃料材料在反應堆中產生動力通過鑄造溶解燃料切碎用過的燃料1 2 3 4 5

Alt C Acquisition Corp.31 Oklo有可能在燃料回收方面引領行業。Oklo被能源部選為四項成本分享獎,潛在地將回收技術商業化Oklo的回收技術開發項目技術商業化基金x開發用於關鍵回收過程效率改進的先進傳感器ARPA-E Open x利用機器學習和數字配對來提高回收效率和材料責任ARPA-E從x開始演示回收過程結束-到端並開發商業規模燃料回收裝置ARPA-E Curie x的技術基礎,演示將舊氧化物燃料轉化為金屬,能夠將現有船隊的廢物循環利用為先進的反應堆燃料

32深度和差異化的“硬技術”、核工程和監管專業知識…憑藉經驗豐富的團隊創始人領導的組織和深厚的技術專長以及經驗豐富的團隊x Oklo的團隊來自財富500強和全球公司,以及政府和科學背景x彙集了多個行業的專業知識和經驗,以提供先進的能源產品(例如,核能、航空航天、汽車和科技)Jacob DeWitte聯合創始人兼首席執行官於2013年聯合創立Oklo,Caroline Cochran於2013年聯合創立Oklo·在核技術方面擁有15年以上的經驗·擁有麻省理工學院核工程博士學位·曾供職於GE、Sandia National Labs、Urenco、和美國海軍核實驗室·15年以上核技術經驗·核工程碩士、麻省理工學院·之前在國防部長辦公室和美國能源部核能諮詢委員會創始人領導的組織…工作過51名員工,包括8名博士(16%)和20名工程/科學碩士(39%)自上次許可過程以來,多名工程師和監管專家加入了Oklo團隊6名前NRC工作人員協助下一次申請提交董事會包括領先的硬技術投資者

|ALTC收購公司33在核能迫切需求的推動下提供強有力的政策支持簡化、現代的設計方法應用於展示的技術有吸引力的商業模式,目標是盈利的經常性收入贏利價值主張旨在加快客户採用地點和首次部署獲得的燃料嵌入獨特的燃料回收機會的潛在上行優勢強大的創始人領導的團隊具有深厚的技術專長我們的使命是在全球範圍內提供清潔、可靠、負擔得起的能源我們的使命是在全球範圍內提供清潔、可靠、負擔得起的能源與ALTC的“硬技術”投資重點保持一致為什麼投資1 2 3 4 5 6 7 Oklo的Aurora Powerhouse數字渲染僅用於説明目的

|Alt C Acquisition Corp.Oklo歷史1交易信息Oklo財務信息2 3支持素材數字渲染僅用於説明目的

|Alt C Acquisition Corp.35 Oklo在開發成功的強勁記錄基礎上2013 Oklo成立了2014 Oklo從2015年開始籌集種子輪Oklo從Sam Altman領導的第二輪種子輪和由&2016 Oklo牽頭的首輪A輪與NRC 2017開始正式的預申請程序2017 Oklo展示了使用重力鑄造製造燃料原型的能力2018 Oklo飛行員在桑迪亞國家實驗室進行NRC熱測試2019年能源部向Oklo頒發愛達荷州國家實驗室的現場使用許可證和愛達荷州國家實驗室向Oklo 2020授予燃料材料Oklo向NRC提交新穎的組合許可證申請2021年Oklo獲得位於愛達荷州國家實驗室的Aurora發電廠的現場特定授權2023年Oklo向NRC提交了商業規模的燃料回收設施許可項目計劃Oklo宣佈與南俄亥俄州多樣化倡議(SODI)合作在俄亥俄州建立兩座工廠2024/2025年Oklo計劃向NRC提交更新的組合許可申請2026/2027年Oklo目標是愛達荷州國家實驗室的首次部署和電力生產深入的技術背景,牢固的合作伙伴關係和密集的監管參與

|Alt C Acquisition Corp.Oklo歷史1交易信息Oklo財務信息2 3支持素材數字渲染僅用於説明目的

|Alt C Acquisition Corp.37單位經濟學説明性:Aurora Powerhouse(15 MWe)Oklo認為,預期累計工廠現金流等於預期累計資本成本的2.5倍以上注:(1)基於預期Noak(第n個)工廠的關鍵假設。(2)假設所有監管審批均已在預期時間內完成。監管過程,包括必要的NRC批准和許可,是一個漫長而複雜的過程,預計的時間表可能與獲得所有必要批准所需的實際時間有很大差異。單位經濟學以實際方式列報,截至2023年5月列報。本文所提供的單位經濟性僅供參考。實際結果可能會有很大不同。(3)FOAK(首創)工廠資本支出預計為3400萬美元。(4)代表在92%容量係數下的15兆瓦發電能力。Aurora Powerhouse(15兆瓦)(2)0 50 100 150 2年4年6年8年10年説明性年度部署(單位)低高·40年工廠設計壽命·工廠資本支出:-初始工廠建設成本約2,400萬美元(不包括初始燃料負荷)(3)·燃料資本支出:-初始燃料負荷4,750公斤-在40年工廠設計壽命內每10年燃料負荷2,375公斤-不假設Oklo回收燃料用於內部供應。假設所有燃料都是以7,000美元/公斤的成本從第三方供應商那裏購買的新制造的HALEU·年度電力銷售收入:假設年發電量約為121,000兆瓦時(4),經常性收入約為1300萬美元,平均實際電價為105美元/兆瓦時·運營成本:-年度固定費用240萬美元-年度可變費用5.00美元/兆瓦時T+0 T+1 T+2 T+3 T+4 T+5 T+10 40年工廠壽命(百萬美元)資本支出(57美元)(17美元)(107美元)工廠建設(24美元)(24美元)燃料資本支出($33)($33)燃料資本支出($17)($50)收入$13$13$13$13$13$508電力銷售收入$13$13$13$13$13$13$508費用($3)($3)($3)($3)($3)($3)($3)($120)固定設備($2)($2)($2)($2)($2)($96)可變設備($1)($1)($1)($1)($1)($1)($1)($1)($1)($1)($1)($1)($24)年度工廠現金流($57)$10$10$10$10($7)$281現金利潤率NA 76.4%76.4%76.4%(54.4%)55.4%主要假設(1)(2)Aurora 15 MWe説明性單位經濟學(1)(2)

|Alt C Acquisition Corp.38單位經濟學説明性:Aurora Powerhouse(50 MWe)Oklo認為,預期累計工廠現金流等於預期累計資本成本的5.0倍以上注:(1)基於預期Noak(第n個)工廠的關鍵假設。(2)假設所有監管審批均已在預期時間內完成。監管過程,包括必要的NRC批准和許可,是一個漫長而複雜的過程,預計的時間表可能與獲得所有必要批准所需的實際時間有很大差異。單位經濟學以實際方式列報,截至2023年5月列報。本文所提供的單位經濟性僅供參考。實際結果可能會有很大不同。(3)Foak(首創)工廠資本支出預計為8600萬美元。(4)代表在92%容量係數下的50兆瓦發電能力。·40年工廠設計壽命·工廠資本支出:-初始工廠建設成本約為6,100萬美元(不包括初始燃料負荷)(3)·燃料資本支出:-初始燃料負荷7,800公斤-在40年工廠設計壽命內每10年加油負荷3,900公斤-不假定Oklo回收燃料用於內部供應。假設所有燃料都是新制造的HALEU,以7,000美元/公斤的成本從第三方供應商那裏購買·年度電力銷售收入:假設年發電量約為403,000兆瓦時(4),平均實際電價為90美元/兆瓦時,經常性收入約為3,600萬美元·運營成本:-年度固定費用560萬美元-年度可變費用4.00美元/兆瓦時關鍵假設(1)(2)Aurora 50 MWe説明性機組經濟性(1)(2)T+0 T+1 T+2 T+3 T+4 T+5 T+10 40年工廠壽命(以百萬美元為單位)(116美元)(27美元)(198美元)工廠建設(61美元)(61美元)燃料資本支出(55美元)(55美元)燃料資本支出(27美元)(82美元)收入$36$36$36$36$1,452電力銷售收入$36$36$36$36($36)($7)($7)($7)($7)($7)($7)($7)($7)($7)($7)($7)($7)($7)($7)($8)固定工廠($6)($6)($6)($6)($6)($6)($2)可變工廠($2)($2)($2)($2)($2)($65)年度工廠現金流($116)$29$29$29$29$2$966現金利潤率NA 80.1%80.1%80.1%66.5%Aurora Powerhouse(50兆瓦)(2)0 50 100 150 2年4年6年8年10説明性年度部署(單位)低

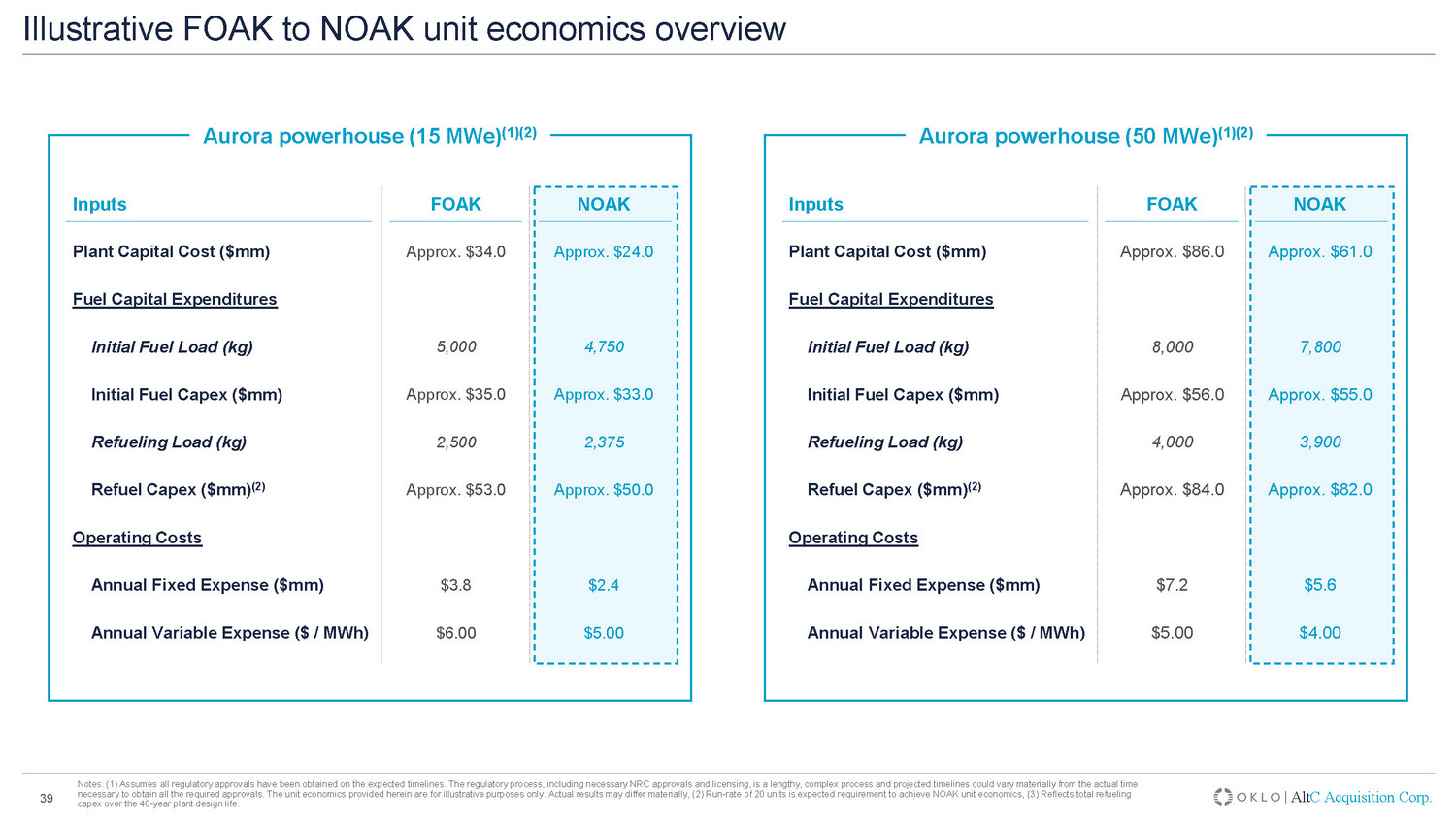

|Alt C Acquisition Corp.投入泡沫Noak工廠資本成本(美元mm)約為。大約34.0美元。24.0美元燃料資本支出初始燃料負荷(公斤)5,000,750初始燃料資本支出(美元)接近。大約35.0美元。$33.0加油負荷(公斤)2,500 2,375加油資本支出(美元mm)(2)接近大約53.0美元。$50.0運營成本年度固定費用(美元mm)$3.8$2.4年度可變費用(美元/兆瓦時)$6.00$5.00注:(1)假設所有監管部門已在預期的時間線上獲得批准。監管過程,包括國家核管理委員會的批准和許可,是一個漫長而複雜的過程,預計的時間表可能與獲得所有必要批准所需的實際時間有很大不同。此處提供的單位經濟性僅用於説明目的。實際結果可能有很大不同,(2)20臺機組的運行率是實現NOAK機組經濟性的預期要求,(3)反映了40年工廠設計壽命內的總加油資本支出。39説明性泡沫到諾克單位經濟學概述奧羅拉發電站(15兆瓦)(1)(2)奧羅拉發電站(50兆瓦)(1)(2)投入泡沫諾克工廠資本成本(美元毫米)接近。大約86.0美元。61.0美元燃料資本支出初始燃料負荷(公斤)8,000 7,800初始燃料資本支出(毫米)接近。大約56.0美元。$55.0加油負荷(公斤)4,000,900加油資本支出($mm)(2)接近大約84.0美元。$82.0運營成本年度固定費用(美元mm)$7.2$5.6年度可變費用(美元/兆瓦時)$5.00$4.00

|Alt C Acquisition Corp.40其他財務信息假設評論一般和行政費用·首次部署前:2024年約1,950萬美元,到2027年增加到約3,450萬美元·長期假設:約佔電力收入的20%製造設施支出·反映Oklo建立製造和製造能力以支持Aurora動力厂部署所需的支出·到2030年工廠製造設施資本支出約4,000萬美元(1)維護支出·約10%的初始工廠資本支出每10年佔用費用·約佔收入營運資金的5.0%·約4.0%的電力收入附註:(1)不包括任何潛在的燃料製造或回收投資。

|Alt C Acquisition Corp.Oklo歷史1交易信息Oklo財務信息2 3支持素材數字渲染僅用於説明目的

|Alt C Acquisition Corp.來源百萬美元516 38%現有Oklo股東850 62%總來源1,366 100%使用百萬美元現金到資產負債表478 35%現有Oklo股東850 62%插圖費用383%總使用1,366 100%注:(1)截至2023年6月30日,ALTC信託現金為515,791,749美元。僅為説明目的,(2)假設ALTC股東並無行使贖回權於交易結束時從信託賬户收取現金,(3)建議交易預付股本價值,但須受業務合併結束前準許公司融資的潛在增長所規限。在業務合併結束時,以每股10美元的價格轉換貨幣前股權價值。不包括潛在溢價股份的影響,(4)ALTC信託現金減去説明性費用和支出,(5)包括所有已發行的ALTC A類股票。包括收盤時未歸屬的625萬股B類方正股票的潛在攤薄影響,以及如果收盤後60天中有20天股價保持在每股10美元或以上,S將被歸屬。不包括312.5萬股B類方正股票(每股12.00美元)和312.5萬股B類方正股票(在交易結束後5年內按比例每股14.00美元和16.00美元)的影響。42交易對Oklo的現金前股權價值為8.5億美元,約為可比清潔能源上市交易估計交易來源的一半,並使用形式上的交易亮點(1)(2)(4)擬議交易概述(3)(3)假設每股10美元(百萬)%所有權現有Oklo股東85 60%ALTC股東58 40%總來源143 100%(3)(1)(5)·貨幣前股權價值8.5億美元,這大約是可比清潔能源上市交易價值的一半·Oklo現有股東可獲得最多1500萬股套利股票,在交易完成後5年內按比例分別以每股12.00美元、14.00美元和16.00美元的價格授予Oklo股東·Oklo股東將100%滾動現有股票·扣除交易費用後籌集的所有收益,將直接進入Oklo的資產負債表,並將用於加速其業務計劃和為Aurora Powerhouse的首次部署提供資金·ALTC贊助商將100%保留的股份進行業績歸屬·Oklo創始人和ALTC贊助商的股票將在業務合併完成後的3年內交錯鎖定

|Alt C Acquisition Corp.附註:(1)不包括溢價股份和允許融資的調整。43公眾投資者、ALTC贊助商和現有Oklo股東之間的長期利益保持一致的簡單交易結構·Oklo股東將獲得合併後公司的8500萬股(1)作為交易的一部分;Oklo股東將不會收到現金收益·在5年內股價升值20%-60%時,最多可獲得1500萬股套現股票;如果股價上漲,通過向Oklo股東提供上行收益,使交易價值能夠被設定在有吸引力的水平·ALTC贊助商將在業務合併結束時放棄100%的方正股票,除非股價升值,否則不會收回其股票·Oklo創始人和ALTC贊助商的股票將在業務合併結束後的3年內交錯鎖定·致力於在強大的上市公司治理下運營·將組建具有相關專業知識的董事會;交易完成後,由奧克羅和奧克洛共同指定的一個董事和另一個由奧克洛和奧克洛共同指定的董事將擁有單一類別的股票,所有股東擁有平等的投票權·簡潔是奧克洛精神的核心-直截了當的公司結構,沒有隻讓奧克洛現有股東受益的特殊協議×投資於奧克洛的所有交易收益淨額。沒有現金給Oklo股東x Oklo股東將100%現有股權滾動x altc發起人將100%保留股份進行業績歸屬x Oklo創始人和altc贊助商長期鎖定x為公開市場上成熟的商業領袖和價值創造者提供支持而組建的董事人才董事會x為所有股東提供平等投票權的單一類別股票x沒有複雜的公司結構或特別股東税收協議Oklo股東將100%現有股權滾動到合併後的公司altc保薦人有資格獲得業績溢價股份的Oklo股東將對100%的保留股份進行業績歸屬對Oklo創始人和altc發起人的長期鎖定董事人才的領先治理和董事會單一類別股票沒有複雜的公司結構或特殊股東税務協議交易結構優先公共投資者利益擬議的交易結構

|Alt C收購公司44風險因素1.我們的商業計劃需要大量投資。如果擬議的業務合併出現重大贖回,我們可能需要對我們的業務計劃進行重大調整或尋求額外資本。根據我們可用的資本資源,我們可能需要推遲或停止預期的短期支出,這可能會限制我們實現某些其他戰略目標的能力和/或減少可用於進一步發展我們的設計、銷售和製造工作的資源,從而對我們的業務前景、財務狀況、運營結果和現金流產生重大影響。2.為了完成我們的業務計劃,除了擬議的業務合併所產生的任何資金外,我們還需要額外的資金。這類資金可能會稀釋我們的投資者,並且不能保證任何此類資金的可用性或條款。任何此類融資和相關條款將高度取決於我們尋求此類融資時的市場狀況和我們業務的進展。我們預計的公司支出和我們實現盈利的能力受到許多風險和不確定因素的影響,包括與通脹影響、不斷變化的監管要求、原材料和核燃料供應、全球衝突、全球供應鏈挑戰和零部件製造和測試的不確定性、當地和國內能源政策、國際能源政策、國際貿易政策、政府合同和採購規則等相關的不確定因素。4.通脹和成本上升可能會對我們造成不成比例的更大影響。雖然材料成本、勞動力或其他通脹或經濟驅動因素的影響將影響整個核能和能源轉型行業(包括可再生能源,如太陽能和風能),但整個行業的相對影響不會相同,行業內的具體影響將取決於許多因素,包括材料使用、技術、設計、供應協議結構、項目管理和其他因素,這些因素可能導致我們技術的競爭力和我們出售動力設備的能力發生重大變化,這可能對我們的業務前景、財務狀況、運營結果和現金流產生實質性的不利影響。5.我們是一家處於早期階段的公司,有財務虧損的歷史(例如g.,負現金流),我們預計至少在我們的動力公司變得商業可行之前,我們將招致鉅額費用和持續的財務損失,而這可能永遠不會發生。6.如果我們不能有效地管理我們的增長,我們可能無法執行我們的業務計劃,這可能會對我們的業務前景、財務狀況、運營結果和現金流產生重大不利影響。7.我們還沒有出售任何發電廠,也沒有與任何客户簽訂任何具有約束力的電力或供熱合同,也不能保證我們將來能夠這樣做。有限的商業運營歷史使我們很難評估我們的前景以及我們可能遇到的風險和挑戰。8.我們的商業計劃包括使用投資税收抵免、生產税收抵免或其他形式的政府資金,為我們的強國的商業發展提供資金,但不能保證我們的項目將有資格獲得這些抵免,也不能保證未來政府資金將可用。9.將我們的動力裝置推向市場所需的時間和資金,可能會大大超過我們的預測。10.由於許多因素,我們對電站的建造和交付時間表的估計可能會增加,包括預製程度、標準化、現場施工、長期採購、承包商業績、工廠資質測試和其他現場具體考慮因素。11.我們目前沒有采用任何風險分擔結構來降低與我們的發電站的交付和業績相關的風險。我們在首次商業交付中可能遇到的任何延誤或挫折,或未能為未來訂單獲得最終投資決定,都可能對我們的業務前景、財務狀況、運營結果和現金流產生重大不利影響,並可能損害我們的聲譽。12.13.我們的業務計劃和實現盈利的能力依賴於我們的兩種動力配置(15兆瓦和50兆瓦)的同時開發,並對這種並行開發方法所導致的學習、效率和監管批准做出某些假設,這種假設可能不準確或不正確。這些假設的任何不利變化都可能對我們的業務前景、財務狀況、經營業績和現金流產生重大不利影響。14.我們的業務計劃和實現盈利的能力也可能依賴於我們的動力裝置(100兆瓦或其他規模)的其他配置的發展,並對這種新的發展方法所產生的學習、效率和監管批准做出某些假設,這可能不準確或不正確。這些假設的任何不利變化都可能對我們的業務前景、財務狀況、經營業績和現金流產生重大不利影響。15.我們的成本預算對更廣泛的經濟因素高度敏感,我們控制或管理成本的能力可能有限。部署像Aurora這樣的首屈一指的發電廠的資本和運營成本很難預測,本質上是可變的,並且會根據各種因素而發生重大變化,這些因素包括現場特定因素、客户承購要求、監管監督、運營協議、供應鏈可用性、供應鏈可用性對反應堆和發電廠性能的影響、通貨膨脹和其他因素。16.後續部署減少費用的機會同樣不確定。如果未能在預期的時間框架或幅度內實現成本降低,Aurora可能無法與替代技術相比具有成本競爭力,這可能會對我們的業務前景、財務狀況、運營結果和現金流產生重大不利影響,並可能損害我們的聲譽。17.將我們的核燃料大規模推向市場所需的時間和資金可能遠遠超出我們的預期。18.先進裂變能源的市場尚未建立,可能無法實現我們預期的增長潛力,或增長速度可能慢於預期,並可能被新技術或現有技術的新應用所取代或淘汰。19.美國的回收核燃料市場尚未建立,可能無法實現我們預期的增長潛力,或者增長速度可能慢於預期,因此我們在回收方面的投資可能錯位。20.我們和我們的客户在一個政治敏感的環境中運營,公眾對裂變能量的看法可能會影響我們的客户和我們。21.我們的技術需要監管批准,而影響監管要求、流程和監管這些技術能力的放射性材料處理和使用方面的政策可能會發生變化,使監管批准無法獲得,從而對我們的業務產生不利影響。

|Alt C Acquisition Corp.45風險因素22.我們的業務計劃涉及與政府和政府附屬實體簽訂合同,合同程序、規則和法規的任何更改或延誤都可能延長我們建造和運營工廠的時間框架,這可能會對我們的業務產生實質性的不利影響。23.涉及美國或全球核能設施的事故,包括事故、恐怖主義行為或其他涉及放射性材料的高調事件,可能會對公眾對核能安全、我們的客户和我們經營的市場的看法產生實質性的不利影響,這些不利影響可能會減少對核能的需求,增加監管要求和成本,或導致可能對我們的業務產生重大不利影響的責任或索賠。24.雖然我們相信我們的成本估計是合理的,但在考慮到供應鏈可用性、製造成本、我們在監管過程中的進展或其他因素(包括特別影響我們的動力設備的意外成本增加)後,隨着設計成熟度的提高,成本可能會大幅增加。25.由於許多因素,包括監管和建設的複雜性,建造一個新的燃料製造設施是具有挑戰性的,而且可能需要更長的時間或比我們預期的更高的成本。26.我們目前還沒有尋求也沒有收到第三方成本估算,但預計未來會這樣做。這樣的第三方成本估計可能大大高於我們目前的估計,這可能會影響我們各大公司的適銷性,以及我們對我們的業務計劃和未來盈利能力的預期27。28.與現有的大型輕水反應堆相比,這種類型、配置和規模的金屬燃料快堆的操作經驗有限。這可能會導致比預期更高的建設成本、部署時間表、維護要求、不同的功率輸出和更大的運營費用。29.與傳統的電力和供熱應用相比,在偏遠環境或工業應用中運營核電站有額外的風險和成本。這樣的部署可能需要額外的成本,包括與許可程序、工廠配置控制、最低操作人員、培訓、安全基礎設施、輻射防護、政府報告和核保險相關的成本,所有這些成本都可能令人望而卻步或降低技術的競爭力。30.來自現有或新競爭對手或技術的競爭可能會導致我們面臨價格下行壓力、客户訂單減少、利潤率下降、無法利用新的商業機會,以及市場份額的喪失。31.新的替代無碳能源發電技術的成功商業化或現有替代無碳能源發電技術的進一步增強,例如在化石燃料發電廠、風能、太陽能或核聚變中增加碳捕獲和封存/儲存機制,可能會被證明更具成本效益或對全球能源市場更具吸引力,因此可能會對市場需求和我們成功將目標發電廠商業化的能力產生不利影響。32.我們發電廠產生的電力和熱能的成本可能不具有其他來源產生的電力和/或熱能的成本競爭力,並且不能保證我們將能夠相對於其他能源收取溢價,這可能對我們的業務前景、財務狀況、運營結果和現金流產生重大和不利的影響。33.石油、天然氣和其他形式能源的供應和成本的變化會受到動盪的市場狀況的影響,這可能會對我們的業務前景、財務狀況、經營業績和現金流產生不利影響。34.我們依賴於有限數量的供應商提供某些材料和供應的部件,其中一些是高度專業化的,正在為我們的發電廠設計的獨一無二或獨家使用。我們和我們的第三方供應商可能無法獲得足夠的材料或供應的組件來滿足我們的製造和運營需求,或無法以優惠的條件獲得此類材料。35歲。S。聯邦和州級政府當局,包括美國。S。核管理委員會(“NRC”)和我們可能在其中設立業務的其他司法管轄區的監管機構。我們的運營和業務計劃可能會受到政府政策和優先事項變化的重大影響。36.我們的業務受到嚴格的美國法律的約束。S。出口管制法律法規。這些法律法規的不利變化或美國。S。政府的許可證政策,我們未能確保及時使用。S。政府根據這些法律和法規的授權,或我們未能遵守這些法律和法規,可能會對我們的全球擴張能力產生重大不利影響,從而影響我們的業務前景、財務狀況、運營結果和現金流。37.政府機構預算的變化以及國家實驗室和其他政府機構的人員短缺可能會延長我們對監管審批和建設的估計時間表。38.我們正在向NRC申請一種新的設計,這將需要NRC批准我們的安全系統設計和其他批准,並可能導致額外的分析和設計更改,包括可能重新設計某些系統,並可能導致成本增加和監管批准方面的延誤。39.我們尚未向NRC提交更新的聯合運營許可證申請,Aurora產品系列中的任何動力裝置尚未獲得NRC或任何其他監管機構的批准或許可在任何地點使用,並且不能保證這些設計的批准或許可以及此類批准或許可的時間(如果有的話)。40.現有的NRC框架尚未應用於許可核燃料回收設施用於商業用途,也不能保證NRC將支持我們擬議的核燃料回收設施按照我們預期的時間表或根本不支持我們的發展。41.我們的燃料製造設施將受到美國的嚴格監管。S。政府,可能包括NRC和美國。S。能源部並不保證這些設施的批准或許可。42.奧羅拉發電站的設計尚未在任何國家獲得批准,在部署發電站之前,必須逐個國家獲得批准。審批可能會被推遲或拒絕,或者可能需要修改我們的設計,這可能會對我們的業務前景、財務狀況、運營結果和現金流產生重大不利影響。43.我們的業務涉及有毒、危險和/或放射性材料的使用、運輸和處置,並可能導致不考慮過失或疏忽的責任。44.與許多先進的裂變反應堆一樣,我們的動力裝置預計將部分依賴於目前無法規模化生產的高純度低濃縮鈾(“HALEU”)。獲得國內供應的HALEU可能需要大量的政府援助、監管批准以及額外的第三方開發和投資,以確保供應。如果我們無法訪問HALEU,或者我們的訪問被延遲,我們製造燃料以及生產電力和/或熱量的能力將受到不利影響,這可能對我們的業務前景、財務狀況、運營結果和現金流產生重大不利影響。45.我們必須獲得政府許可,才能在我們的燃料設施運營中擁有和使用放射性材料,包括鈾的同位素。未能獲得或維持此類牌照,或延遲獲得此類牌照,可能會影響我們為客户發電和/或供熱的能力,並對我們的業務前景、財務狀況、運營業績和現金流產生重大不利影響。

|Alt C收購公司46風險因素46。我們必須獲得監管部門的批准,才能在我們的動力房設計中使用各種材料。這包括長時間的輻照測試和分析,如果結果不令人滿意,可能需要重新設計或使用替代供應商。47.我們可能需要某些材料和部件,這些材料和部件僅限量生產,可能主要在美國以外生產。培養關鍵材料和零部件的供應鏈製造能力取決於供應鏈合作伙伴,可能需要美國或其他政府的合作,如果不在假定的時間表或成本內完成,可能會導致短缺和延誤。48.尚未解決的乏核燃料儲存和處置政策問題以及相關成本可能會對我們回收乏燃料作為我們核電廠潛在燃料來源的計劃產生重大負面影響。此外,U.S。與儲存和處置我們發電廠的廢燃料相關的政策和/或客户對與這些政策相關的風險的負面看法可能會對我們的業務前景、財務狀況、運營結果和現金流產生重大負面影響。49.我們的業務性質要求我們與各種政府實體互動,這使得我們受制於這些政府實體的政策、優先事項、法規、任務和資金水平,任何變化都可能對我們產生負面或積極的影響。50美元。未來的潛在客户可能還會要求我們遵守他們在遵守政策、優先事項、法規、控制和授權方面的獨特要求,包括為環境、社會和治理相關的標準或目標提供數據和相關保證。51.購電協議是我們預期的電力銷售業務模式的關鍵組成部分,在某些情況下,客户可能能夠使這些合同全部或部分無效。我們可能需要尋找替代的客户電力和/或熱轉移,或者可能需要取消與特定客户和站點相關的許可工作,因為客户需求或與客户的合同發生了變化。52.購電協議可能包括未按計劃提供足夠的電力和/或熱能的罰款,這可能導致負債和現金流減少。53.我們可能會因違反環境法或根據環境法承擔責任而招致鉅額成本。54.税法的變化可能會對我們的業務前景和財務業績產生不利影響。55.美國。S。政府的預算赤字和國家債務,以及美國的任何能力。S。如果政府未能完成任何政府財政年度的預算或撥款程序,可能會對我們的業務前景、財務狀況、經營成果和現金流產生不利影響。56.我們依靠知識產權法和保密協議來保護我們的知識產權。我們也可能依賴於我們從第三方獲得許可的知識產權。我們未能保護我們的知識產權、我們對第三方知識產權的侵犯,或者我們無法獲得或續訂使用第三方知識產權的許可證,都可能對我們的業務產生不利影響。57.不確定的全球宏觀經濟和政治狀況可能會對我們的業務前景、財務狀況、經營業績和現金流產生重大不利影響。58.我們依賴主要高管和管理層來執行我們的業務計劃並進行我們的運營。關鍵人員的離職可能會對我們的業務產生實質性的不利影響。59.我們的業務計劃要求我們吸引和留住合格的人員,包括具有高度技術專長的人員。我們未能成功招聘和留住有經驗的合格人員,可能會對我們的業務產生實質性的不利影響。60.能源需求的減少或氣候相關政策的變化可能會改變市場狀況,降低我們產品的競爭力,並影響公司業績。61.我們作為一家持續經營的企業繼續經營的能力存在很大疑問,無論業務合併是否完成,我們都可能需要未來的額外資金。62.從2022年1月開始,像我們這樣的成長型公司的市值急劇下降,特別是與SPAC簽訂業務合併協議的公司。近幾個月來,通脹壓力、利率上升以及其他不利的經濟和市場力量導致了市值的下降。因此,我們的證券面臨潛在的下行壓力,這可能導致信託基金可用現金的大量贖回。如果出現大量贖回,我們已發行普通股的流通股將會減少,這可能會導致我們證券價格的進一步波動,並對我們在業務合併結束後獲得融資的能力產生不利影響。63.通過SPAC合併形成的公司的證券,如擬議的交易,可能會經歷相對於合併前SPAC股價的大幅下跌。

|Alt C Acquisition Corp.數字渲染僅用於説明目的

| AltC Acquisition Corp. Notes: (1) U.S. Energy Information Administration (Uranium Marketing Annual Report – 2022). (2) Department of Energy (5 Fast Fac ts about Spent Nuclear Fuel). 28 Fuel recycling Upside opportunity Oklo Large spent fuel stockpiles Spent fuel potential Oklo design advantage Unique upside opportunity Fuel supply constraints The U.S. currently relies on imports for fresh nuclear fuel ✗ In 2022, 95% (1) of uranium for U.S. nuclear plants was foreign - sourced ✗ In 2022, 33% (1) of uranium enrichment services for U.S. nuclear plants were purchased from Russia ✗ U.S. has limited HALEU production, which is the fuel for advanced reactors Limited U.S. fuel capabilities is a pressing concern for advanced reactor growth The U.S. has large and growing spent fuel stockpiles ✗ Expensive to manage ✗ U.S. reactors have generated 90,000 tons of spent fuel since 1950 (2) ✗ 2,000 tons of spent fuel generated each year (2) ✗ Spent fuel is currently stored at 70 reactor sites across 35 states (2) Spent fuel management is complex; needs will grow with new reactor deployment Spent fuel retains its energy potential and can be recycled x Fuel can be recycled and is done so in other countries, such as France x >90% of potential energy remains in spent fuel after use by current reactors (2) ✗ The U.S. does not currently recycle fuel Opportunity to address fuel supply constraints and spent fuel stockpiles with recycling Fast reactors can use either fresh or recycled fuel x EBR - II demonstrated fast reactor’s ability to use recycled fuel x Oklo plants designed with flexibility to use either fresh or recycled fuel x First Aurora powerhouse to be fueled by spent fuel recovered from EBR - II Fuel recycling could provide future margin uplift and new revenue streams Oklo is developing fuel recycling capabilities x Waste to clean energy x Selected for four projects with the Department of Energy to develop fuel recycling technologies x Initial plans to pursue a commercial - scale fuel recycling facility in the U.S. by 2030’s Oklo has the potential opportunity to lead the industry in fuel recycling

| AltC Acquisition Corp. U.S. nuclear power plants are heavily reliant on imported nuclear fuel Nuclear fuel imports | AltC Acquisition Corp. 29 Source of uranium for U.S. nuclear power plants (Uranium oxide, million pounds) (1) Notes: (1) U.S. Energy Information Administration (Nuclear explained – where our uranium comes from). (2) U.S. Energy Information Administration (Uranium Marketing Annual Report – 2022), (3) Orano (All about used fuel processing and recycling). Evolving geopolitical concerns In 2022, 95% (2) of uranium for U.S. nuclear plants was foreign - sourced In 2022, 33% (2) of foreign uranium enrichment services required by U.S. nuclear plants were purchased from Russia 0 20 40 60 80 1950 1960 1970 1980 1990 2000 2010 2020 Domestic production Purchased imports Fuel recycling could reduce U.S. imports The U.S. does not currently recycle spent fuel However, fuel can be recycled and is done so in other countries, such as France Nearly 1 in 10 light bulbs in France runs on recycled nuclear materials (3)

| Alt C Acquisition Corp. 30 Fuel recycling could provide potential future margin uplift and new revenue streams Potential opportunity to build and operate facilities that could supply recycled fuel to Aurora powerhouses as well as third - par ty customers Spent fuel recycling is a significant potential cost savings opportunity for Oklo that could reduce both initial plant capital costs as well as ongoing operating costs Vertically integrated fuel source will provide security and assurance Oklo’s recycling approach utilizes pyro - processing, which is a mature technology Additional potential revenue streams through the sale of spent fuel management services as well as the sale of byproducts and specialty isotopes to various end markets Fuel recycling solves a longstanding issue in the market and can create a sustainab le competitive advantage In January 2023, Oklo submitted a commercial - scale fuel recycling facility licensing project plan to the Nuclear Regulatory Commission How fuel recycling works Separate fuel material via electrochemistry Produce power in reactor Fabricate fuel by casting Dissolve fuel Chop up used fuel 1 2 3 4 5

| Alt C Acquisition Corp. 31 Oklo has the potential opportunity to lead the industry in fuel recycling Oklo selected by the Department of Energy for four cost - share awards to potentially commercialize recycling technologies Oklo’s recycling technology development projects Technology Commercialization Fund x Develop advanced sensors for key recycling process efficiency improvements ARPA – E Open x Utilize machine learning and digital twinning for recycling efficiency improvements and material accountability ARPA – E Onwards x Demonstrate the recycling process end - to - end and develop the technical basis for commercial - scale fuel recycling facility ARPA – E Curie x Demonstrate the conversion of used oxide fuel into metal, enabling the recycling of waste from the current fleet into advanced reactor fuel

| Alt C Acquisition Corp. 32 Deep and differentiated “hard tech,” nuclear engineering, and regulatory expertise …with a highly experienced team Founder - led organization with deep technical expertise and a highly experienced team x Oklo's team comes from Fortune 500 and global companies, as well as government and science backgrounds x Bringing together expertise and experience from several industries to deliver an advanced energy product (e.g., nuclear power, aerospace, automotive and tech) Jacob DeWitte Co - Founder and CEO Co - Founded Oklo in 2013 Caroline Cochran Co - Founder and COO Co - Founded Oklo in 2013 • 15+ years of experience in nuclear technology • PhD in nuclear engineering, MIT • Prior experiences at GE, Sandia National Labs, Urenco U.S., and the US Naval Nuclear Laboratory • 15+ years of experience in nuclear technology • MS in nuclear engineering, MIT • Prior experiences in the Office of the Secretary of Defense and U.S. Department of Energy Nuclear Energy Advisory Committee Founder - led organization… 51 employees, including 8 PhDs (16%) and 20 Masters in Engineering / Science (39%) Multiple engineers and regulatory experts have joined the Oklo team since the last licensing process Six former NRC staff members to assist with the next application filing Board of Directors includes leading hard tech investors

| AltC Acquisition Corp. 33 Strong policy support driven by critical need for nuclear energy Simplified, modern design approach applied to demonstrated technology Attractive business model targeting profitable recurring revenue Winning value proposition intended to accelerate customer adoption Site and fuel secured for first deployment Embedded potential upside from unique fuel recycling opportunity Strong founder - led team with deep technical expertise Our mission is to provide clean, reliable, affordable energy on a global scale Compelling opportunity aligned with AltC’s “hard tech” investment focus Why invest 1 2 3 4 5 6 7 Oklo’s Aurora powerhouse Digital rendering for illustrative purposes only

| Alt C Acquisition Corp. Oklo history 1 Transaction information Oklo financial information 2 3 Supporting material Digital rendering for illustrative purposes only

| Alt C Acquisition Corp. 35 Oklo is building upon a strong track record of development success 2013 Oklo founded 2014 Oklo raises seed round from 2015 Oklo raises second seed round from led by Sam Altman and a Series A round led by & 2016 Oklo begins formal pre - application process with NRC 2017 Oklo demonstrates ability to fabricate fuel prototypes using gravity casting 2018 Oklo pilots novel application with the NRC Thermal testing at Sandia National Lab 2019 DOE issues Oklo a Site Use Permit at Idaho National Laboratory and Idaho National Laboratory awards fuel material to Oklo 2020 Oklo submits novel combined license application to the NRC NRC approves Oklo’s quality assurance program description 2021 Oklo receives site specific authorization for Aurora powerhouse located at the Idaho National Laboratory 2023 Oklo submitted commercial - scale fuel recycling facility licensing project plan to the NRC Oklo announces partnership with the Southern Ohio Diversification Initiative (SODI) for two plants in Ohio 2024/2025 Oklo plans submission of updated combined license application to the NRC 2026/2027 Oklo targets first deployment and electricity production at Idaho National Laboratory Deep technical background, strong partnerships, and intensive regulatory engagement

| Alt C Acquisition Corp. Oklo history 1 Transaction information Oklo financial information 2 3 Supporting material Digital rendering for illustrative purposes only

| Alt C Acquisition Corp. 37 Illustrative unit economics: Aurora powerhouse (15 MWe) Oklo believes that expected cumulative plant cash flow equals more than 2.5x expected cumulative capital costs Notes: (1) Key assumptions based on expected NOAK (nth of a kind) plant. (2) Assumes all regulatory approvals have been obtai ned on the expected timelines. The regulatory process, including necessary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actual time necessary to obtain all the required approvals. Th e u nit economics are presented in real terms and are presented as of May 2023. The unit economics provided herein are for illust rat ive purposes only. Actual results may differ materially. (3) FOAK (first - of - a - kind) plant capital expenditure expected to be ~$34 mi llion. (4) Represents 15 MWe generating capacity at a 92% capacity factor. Aurora powerhouse (15 MWe) (2) 0 50 100 150 Year 2 Year 4 Year 6 Year 8 Year 10 Illustrative Annual Deployments (Units) Low High • 40 - year plant design life • Plant capital expenditures: ‒ Initial plant construction cost of approximately $24.0 million (excluding initial fuel load) (3) • Fuel capital expenditures: ‒ Initial fuel load of 4,750 kg ‒ Refueling load of 2,375 kg every 10 years over the 40 - year plant design life ‒ Does not assume Oklo recycles fuel for internal supply. Assumes all fuel is newly fabricated HALEU purchased from a third - party supplier at a cost of $7,000 / kg • Revenue from annual power sales : recurring revenue of approximately $13.0 million assuming annual generation of approximately 121,000 MWh (4) and average real power price of $105 / MWh • Operating costs: ‒ Annual fixed expense of $2.4 million ‒ Annual variable expense of $5.00 / MWh T+0 T+1 T+2 T+3 T+4 T+5 T+10 40-Yr Life of Plant ($ in Millions) Capital Expenditures ($57) ($17) ($107) Construction of Plant ($24) ($24) Fuel Capex ($33) ($33) Refueling Capex ($17) ($50) Revenue $13 $13 $13 $13 $13 $13 $508 Revenue from Power Sales $13 $13 $13 $13 $13 $13 $508 Expenses ($3) ($3) ($3) ($3) ($3) ($3) ($120) Fixed Plant ($2) ($2) ($2) ($2) ($2) ($2) ($96) Variable Plant ($1) ($1) ($1) ($1) ($1) ($1) ($24) Annual Plant Cash Flow ($57) $10 $10 $10 $10 $10 ($7) $281 Cash Margin NA 76.4% 76.4% 76.4% 76.4% 76.4% (54.4%) 55.4% Key Assumptions (1)(2) Aurora 15 MWe Illustrative Unit Economics (1)(2)

| Alt C Acquisition Corp. 38 Illustrative unit economics: Aurora powerhouse (50 MWe) Oklo believes that expected cumulative plant cash flow equals more than 5.0x expected cumulative capital costs Notes: (1) Key assumptions based on expected NOAK (nth of a kind) plant. (2) Assumes all regulatory approvals have been obtai ned on the expected timelines. The regulatory process, including necessary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actual time necessary to obtain all the required approvals. Th e u nit economics are presented in real terms and are presented as of May 2023. The unit economics provided herein are for illust rat ive purposes only. Actual results may differ materially. (3) FOAK (first - of - a - kind) plant capital expenditure expected to be ~$86 mi llion. (4) Represents 50 MWe generating capacity at a 92% capacity factor. • 40 - year plant design life • Plant capital expenditures: ‒ Initial plant construction cost of approximately $61.0 million (excluding initial fuel load) (3) • Fuel capital expenditures: ‒ Initial fuel load of 7,800 kg ‒ Refueling load of 3,900 kg every 10 years over the 40 - year plant design life ‒ Does not assume Oklo recycles fuel for internal supply. Assumes all fuel is newly fabricated HALEU purchased from a third - party supplier at a cost of $7,000 / kg • Revenue from annual power sales : recurring revenue of approximately $36.0 million assuming annual generation of approximately 403,000 MWh (4) and average real power price of $90 / MWh • Operating costs: ‒ Annual fixed expense of $5.6 million ‒ Annual variable expense of $4.00 / MWh Key Assumptions (1)(2) Aurora 50 MWe Illustrative Unit Economics (1)(2) T+0 T+1 T+2 T+3 T+4 T+5 T+10 40-Yr Life of Plant ($ in Millions) Capital Expenditures ($116) ($27) ($198) Construction of Plant ($61) ($61) Fuel Capex ($55) ($55) Refueling Capex ($27) ($82) Revenue $36 $36 $36 $36 $36 $36 $1,452 Revenue from Power Sales $36 $36 $36 $36 $36 $36 $1,452 Expenses ($7) ($7) ($7) ($7) ($7) ($7) ($288) Fixed Plant ($6) ($6) ($6) ($6) ($6) ($6) ($224) Variable Plant ($2) ($2) ($2) ($2) ($2) ($2) ($65) Annual Plant Cash Flow ($116) $29 $29 $29 $29 $29 $2 $966 Cash Margin NA 80.1% 80.1% 80.1% 80.1% 80.1% 4.9% 66.5% Aurora powerhouse (50 MWe) (2) 0 50 100 150 Year 2 Year 4 Year 6 Year 8 Year 10 Illustrative Annual Deployments (Units) Low High

| Alt C Acquisition Corp. Inputs FOAK NOAK Plant Capital Cost ($mm) Approx. $34.0 Approx. $24.0 Fuel Capital Expenditures Initial Fuel Load (kg) 5,000 4,750 Initial Fuel Capex ($mm) Approx. $35.0 Approx. $33.0 Refueling Load (kg) 2,500 2,375 Refuel Capex ($mm) (2) Approx. $53.0 Approx. $50.0 Operating Costs Annual Fixed Expense ($mm) $3.8 $2.4 Annual Variable Expense ($ / MWh) $6.00 $5.00 Notes: (1) Assumes all regulatory approvals have been obtained on the expected timelines. The regulatory process, including n ece ssary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actua l t ime necessary to obtain all the required approvals. The unit economics provided herein are for illustrative purposes only. Actual re sults may differ materially, (2) Run - rate of 20 units is expected requirement to achieve NOAK unit economics, (3) Reflects total refueling capex over the 40 - year plant design life. 39 Illustrative FOAK to NOAK unit economics overview Aurora powerhouse (15 MWe) (1)(2) Aurora powerhouse (50 MWe) (1)(2) Inputs FOAK NOAK Plant Capital Cost ($mm) Approx. $86.0 Approx. $61.0 Fuel Capital Expenditures Initial Fuel Load (kg) 8,000 7,800 Initial Fuel Capex ($mm) Approx. $56.0 Approx. $55.0 Refueling Load (kg) 4,000 3,900 Refuel Capex ($mm) (2) Approx. $84.0 Approx. $82.0 Operating Costs Annual Fixed Expense ($mm) $7.2 $5.6 Annual Variable Expense ($ / MWh) $5.00 $4.00

| Alt C Acquisition Corp. 40 Additional financial information Assumption Commentary General and Administrative Expenses • Before first deployment : Approximately $19.5 million in 2024 scaling to approximately $34.5 million by 2027 • Long - term assumption : Approximately 20% of power revenue Manufacturing Facility Expenditures • Reflects the required spend by Oklo to establish manufacturing and fabrication capabilities to support deployment of the Aurora powerhouse • Approximately $40 million in plant manufacturing facility capital expenditures by 2030 (1) Maintenance Expenditures • Approximately 10% maintenance capital expenditures of initial plant capital costs every 10 years Occupancy Expense • Approximately 5.0% of power revenue Working Capital • Approximately 4.0% of power revenue Notes: (1) Does not include any potential fuel fabrication or recycling investment.

| Alt C Acquisition Corp. Oklo history 1 Transaction information Oklo financial information 2 3 Supporting material Digital rendering for illustrative purposes only

| Alt C Acquisition Corp. Sources $ millions % AltC cash-in-trust 516 38% Existing Oklo shareholders 850 62% Total sources 1,366 100% Uses $ millions % Cash to balance sheet 478 35% Existing Oklo shareholders 850 62% Illutrative fees and expenses 38 3% Total uses 1,366 100% Notes: (1) AltC cash - in - trust was $515,791,749 as of June 30, 2023. For illustrative purposes only, (2) Assumes no AltC shareholders exercise their redemption rights to receive cash from the trust account at closing, (3) Proposed transaction pre - m oney equity value, subject to potential increase for permitted company financings prior to close of the business combination. Pre - money equity valu e to convert at $10 per share at close of the business combination. Excludes impact of potential earnout shares, (4) AltC cash - in - trust less illustrative fees and expenses, (5) Includes all outstanding AltC Class A shares. Includes the potential dilutive impact of 6.250 million Class B founder shares that are unvested at close and s ubject to vesting if the post - closing share price remains at or above $10 per share for 20 of 60 days. Excludes the impact of 3.125 million Class B founder shares that vest at $12.00 per share an d 3 .125 million Class B founder shares that vest ratably at $14.00 per share and $16.00 per share within 5 - years of closing. 42 Transaction values Oklo at a pre - money equity value of $850 million, which is roughly half the value of comparable clean energy go public transactions Estimated transaction sources and uses Pro forma ownership Transaction highlights (1)(2) (4) Proposed transaction overview (3) (3) Assumes $10 per share Shares (millions) % Ownership Existing Oklo shareholders 85 60% AltC shareholders 58 40% Total sources 143 100% (3) (1)(5) • Pre - money equity value of $850 million, which is roughly half the value of comparable clean energy go public transactions • Up to 15.0 million earnout shares available for existing Oklo shareholders, vesting ratably at $12.00, $14.00, and $16.00 per share within 5 - years of closing • No cash to Oklo shareholders – will roll 100% of existing shares • All proceeds raised, net of transaction expenses, will go directly to Oklo’s balance sheet and will be used to accelerate its business plan and fund the first deployment of the Aurora powerhouse • AltC sponsor will subject 100% of retained shares to performance vesting • Oklo founders and AltC sponsor shares will be subject to a staggered lock - up over 3 years following closing of the business combination

| Alt C Acquisition Corp. Notes: (1) Excluding earnout shares and adjustments for permitted financings. 43 Simple transaction structure with alignment of long - term interests between public investors, the AltC sponsors, and existing Oklo shareholders • Oklo shareholders will receive 85.0 million shares (1) in the combined company as part of the transaction; no cash proceeds to be received by Oklo shareholders • Up to 15.0 million earnout shares available upon share price appreciation of 20 – 60% within 5 - years; enables transaction value to be set at an attractive level by providing upside to Oklo shareholders if the share price rises • AltC sponsor will un - vest 100% of founder shares at close of the business combination and will not earn back its shares unless the share price appreciates • Oklo founders and AltC sponsor shares will be subject to a staggered lock - up over 3 years following close of the business combination • Committed to operate with strong public company governance • Board with relevant expertise to be assembled; one director nominated by AltC and another director mutually designated by AltC and Oklo • Oklo will have a single class of shares following the transaction with equal voting rights for all shareholders • Simplicity is core to Oklo’s ethos – straightforward corporate structure and no special agreements that only benefit existing Oklo shareholders x All net transaction proceeds invested in Oklo, no cash to Oklo shareholders x Oklo shareholders to roll 100% of existing equity x AltC’s sponsor to subject 100% of retained shares to performance vesting x Long duration lock - up for Oklo founders and AltC’s sponsor x Board of director talent to be assembled to provide support from proven business leaders and value creators in the public markets x Single class of shares with equal voting rights for all shareholders x No complex corporate structure or special shareholder tax agreements Oklo shareholders to roll 100% of existing equity into the combined company Oklo shareholders eligible for performance - based earnout shares AltC sponsor will subject 100% of retained shares to performance vesting Long duration lock - up for Oklo founders and AltC sponsor Leading governance and board of director talent Single class of shares No complex corporate structure or special shareholder tax agreements Transaction structure priorities Public investor benefits Proposed transaction structure

| Alt C Acquisition Corp. 44 Risk Factors 1. Our business plan requires substantial investment . If there are significant redemptions in connection with the proposed Business Combination, we may need to make significant adjustments to our business plan or seek additional capital . Depending on our available capital resources, we may need to delay or discontinue expected near - term expenditures, which could materially impact our business prospects, financial condition, results of operations and cash flows by limiting our ability to pursue some of our other strategic objectives and/or reducing the resources available to further develop our design, sales and manufacturing efforts . 2. In order to fulfill our business plan, we will require additional funding in addition to any funding resulting from the proposed Business Combination . Such funding may be dilutive to our investors and no assurances can be provided as to the availability or terms of any such funding . Any such funding and the associated terms will be highly dependent upon market conditions and the progress of our business at the time we seek such funding . 3. Our projected corporate expenditures and our ability to achieve profitability are subject to numerous risks and uncertainties, including uncertainties related to the impact of inflation, evolving regulatory requirements, raw material and nuclear fuel availability, global conflicts, global supply chain challenges and component manufacturing and testing uncertainties, local and domestic energy policies, international energy policies, international trade policies, government contracting and procurement rules, among other factors . Accordingly, it is possible that our overall expenditures could be higher than the levels we currently estimate, and any increases could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 4. We may experience a disproportionately larger impact from inflation and rising costs . Although the impact of material cost, labor, or other inflationary or economically driven factors will impact the entire nuclear and energy transition industry (including renewable sources of electricity, like solar and wind), the relative impact will not be the same across the industry, and the particular effects within the industry will depend on a number of factors, including material use, technology, design, structure of supply agreements, project management and other factors, which could result in significant changes to the competitiveness of our technology and our ability to sell our powerhouses, which could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 5. We are an early - stage company with a history of financial losses (e . g . , negative cash flows), and we expect to incur significant expenses and continuing financial losses at least until our powerhouses become commercially viable, which may never occur . 6. If we fail to manage our growth effectively, we may be unable to execute our business plan which could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 7. We have not yet sold any powerhouses or entered into any binding contract with any customer to deliver electricity or heat and there is no guarantee that we will be able to do so in the future . This limited commercial operating history makes it difficult to evaluate our prospects and the risks and challenges we may encounter . 8. Our business plan includes the use of investment tax credits, production tax credits or other forms of government funding to finance the commercial development of our powerhouses, and there is no guarantee that our projects will qualify for these credits or that government funding will be available in the future . 9. The amount of time and funding needed to bring our powerhouses to market may greatly exceed our projections . 10. Our construction and delivery timeline estimates for our powerhouses may increase due to a number of factors, including the degree of pre - fabrication, standardization, on - site construction, long - lead procurement, contractor performance, plant qualification testing and other site - specific considerations . 11. We do not currently employ any risk sharing structures to mitigate the risks associated with the delivery and performance of our powerhouses . Any delays or setbacks we may experience for our first commercial delivery or failure to obtain final investment decisions for future orders could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows and could harm our reputation . 12. Any failure to effectively update the design, construction, and operations of our powerhouses to ensure cost competitiveness could reduce the marketability of our powerhouses and adversely impact our expected deployment schedules . 13. Our business plan and our ability to achieve profitability relies on the concurrent development of two configurations of our powerhouses ( 15 MWe and 50 MWe), and makes certain assumptions with respect to learnings, efficiencies and regulatory approvals as a result of this concurrent development approach which may not be accurate or correct . Any adverse change to these assumptions may have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 14. Our business plan and our ability to achieve profitability may also rely on the development of other configurations of our powerhouses ( 100 MWe, or other sizes), and makes certain assumptions with respect to learnings, efficiencies and regulatory approvals as a result of this new development approach which may not be accurate or correct . Any adverse change to these assumptions may have a material adverse effect on our business prospects, financial condition and results of operation and cash flows . 15. Our cost estimates are highly sensitive to broader economic factors, and our ability to control or manage our costs may be limited . Capital and operating costs for the deployment of a first - of - a - kind powerhouse like the Aurora are difficult to project, inherently variable and are subject to significant change based on a variety of factors including site specific factors, customer off - take requirements, regulatory oversight, operating agreements, supply chain availability, supply chain availability effects on reactor and power plant performance, inflation and other factors . 16. Opportunities for cost reductions with subsequent deployments are similarly uncertain . To the extent cost reductions are not achieved within the expected timeframe or magnitude, the Aurora may not be cost competitive with alternative technologies, which may have a material adverse effect on our business prospects, financial condition, results of operations and cash flows and could harm our reputation . 17. The amount of time and funding needed to bring our nuclear fuel to market at scale may significantly exceed our expectations . Any material change to our assumptions or expectations with respect to our timeline and funding needs, or any material overruns or other unexpected increase in costs or delays, which may have a material adverse effect on our business prospects, financial condition, results of operations and cash flows and could harm our reputation . 18. The market for advanced fission power is not yet established and may not achieve the growth potential we expect or may grow more slowly than expected and may be superseded or rendered obsolete by new technology or the novel application of existing technology . 19. The market for recycled nuclear fuel in the United States is not yet established and may not achieve the growth potential we expect or may grow more slowly than expected as a result our investment in recycling may be misplaced . 20. We and our customers operate in a politically sensitive environment, and the public perception of fission energy can affect our customers and us . 21. Our technology requires regulatory approvals, and policies around the handling and use of radioactive materials that affect regulatory requirements, processes and the ability to regulate these technologies may change and make regulatory approvals not attainable, adversely affecting our business .

| Alt C Acquisition Corp. 45 Risk Factors 22. Our business plan involves contracting with the government and government - affiliated entities, and any changes or delays to contracting procedures, rules and regulations could lengthen our timeframes to construct and operate our plants, which could materially and adversely affect our business . 23. Incidents involving nuclear energy facilities in the United States or globally, including accidents, terrorist acts or other high profile events involving radioactive materials, could materially and adversely affect the public perception of the safety of nuclear energy, our customers and the markets in which we operate, and such adverse effects could potentially decrease demand for nuclear energy, increase regulatory requirements and costs or result in liability or claims that could materially and adversely affect our business . 24. While we believe our cost estimates are reasonable, they may increase significantly through design maturity, when accounting for supply chain availability, fabrication costs, as we progress through the regulatory process, or as a result of other factors, including unexpected cost increases that particularly effect our powerhouses . 25. Building a new fuel fabrication facility is challenging as a result of many factors, including regulatory and construction complexity, and may take longer or cost more than we expect . 26. We have not sought nor received third - party cost estimates at this time but expect to do so in the future . Such third - party cost estimates may be significantly higher than our current estimates, which may affect the marketability of our powerhouses and our expectations with respect to our business plan and future profitability 27. There is limited precedent for independent developer construction and operation, or use of power purchase agreements, other behind - the - meter or off - grid business models relating to deployment of fission power plants . 28. There is limited operating experience for metal - fueled fast reactors of this type, configuration and scale, compared to that of the existing fleet of large light water reactors . This may result in greater than expected construction cost, deployment timelines, maintenance requirements, differing power output and greater operating expense . 29. Operating a nuclear power plant in a remote environment or in an industrial application has additional risks and costs compared to conventional electric power and heat applications . Such deployments may require additional costs including costs associated with the licensing process, configuration control of the plant, minimum operating staff, training, security infrastructure, radiation protection, government reporting, and nuclear insurance, all of which may be cost prohibitive or reduce the competitiveness of technology . 30. Competition from existing or new competitors or technologies could cause us to experience downward pressure on prices, fewer customer orders, reduced margins, the inability to take advantage of new business opportunities, and the loss of market share . 31. Successful commercialization of new, or further enhancements to existing, alternative carbon - free energy generation technologies, such as adding carbon capture and sequestration/storage mechanisms to fossil fuel power plants, wind, solar, or fusion, may prove to be more cost effective or appealing to the global energy markets and therefore may adversely affect the market demand for, and our ability to, successfully commercialize our targeted powerhouses . 32. The cost of electricity and heat generated from our powerhouses may not be cost competitive with electricity and/or heat generated from other sources, and there is no guarantee that we will be able to charge a premium relative to other energy sources, which could materially and adversely affect our business prospects, financial condition, results of operations and cash flows . 33. Changes in the availability and cost of oil, natural gas and other forms of energy are subject to volatile market conditions that could adversely affect our business prospects, financial condition, results of operations and cash flows . 34. We rely on a limited number of suppliers for certain materials and supplied components, some of which are highly specialized and are being designed for first - of - a - kind or sole use in our power plants . We and our third party vendors may not be able to obtain sufficient materials or supplied components to meet our manufacturing and operating needs or obtain such materials on favorable terms . 35. The operations of our planned fuel facility in Idaho, planned power plants in Idaho and Ohio, and any future facilities, will be highly regulated by the U . S . federal and state - level governmental authorities, including the U . S . Nuclear Regulatory Commission (“NRC”) and regulatory bodies in other jurisdictions in which we may establish operations . Our operations and business plans could be significantly impacted by changes in government policies and priorities . 36. Our business is subject to stringent U . S . export control laws and regulations . Unfavorable changes in these laws and regulations or U . S . government licensing policies, our failure to secure timely U . S . government authorizations under these laws and regulations, or our failure to comply with these laws and regulations could have a material adverse effect on our ability to expand globally and thereby affect our business prospects, financial condition, results of operations and cash flows . 37. Changes in governmental agency budgets as well as staffing shortages at national laboratories and other governmental agencies may lengthen our estimated timelines for regulatory approval and construction . 38. We are pursuing an application for a novel design with the NRC, which will require NRC approval of our safety system design among other approvals and may result in additional analysis and design changes, including potential redesigns of certain systems, and could lead to increased costs and delays with respect to regulatory approvals . 39. We have not yet submitted our updated combined operating license application to the NRC and no powerhouse in the Aurora product family has yet been approved or licensed for use at any site by the NRC or any other regulatory agency, and approval or licensing of these designs and the timing of such approval or licensing, if any, is not guaranteed . 40. The existing NRC framework has not been applied to license a nuclear fuel recycling facility for commercial use, and there is no guarantee that the NRC will support the development of our proposed nuclear fuel recycling facility on the timeline we anticipate or at all . 41. Our fuel fabrication facilities will be highly regulated by the U . S . government, potentially including both the NRC and the U . S . Department of Energy and approval or licensing of these facilities is not guaranteed . 42. The design of the Aurora powerhouses has not been approved in any country, and approvals must be obtained on a country - by - country basis before the powerhouses can be deployed . Approvals may be delayed or denied or may require modification to our design, which could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 43. Our operations involve the use, transportation and disposal of toxic, hazardous and/or radioactive materials and could result in liability without regard to fault or negligence . 44. Our powerhouses, like many advanced fission reactors, are expected to rely, in part, on high assay low enriched uranium (“ HALEU ”) which is not currently available at scale . Access to a domestic supply of HALEU may require significant government assistance, regulatory approval, and additional third - party development and investment to ensure availability . If we are unable to access HALEU , or our access is delayed, our ability to manufacture fuel and to produce electricity and/or heat will be adversely affected, which could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 45. We must obtain governmental licenses to possess and use radioactive materials, including isotopes of uranium, in our fuel facility operations . Failure to obtain or maintain, or delays in obtaining, such licenses could impact our ability to generate electricity and/or heat for our customers and have a material adverse effect on our business prospects, financial condition, results of operations and cash flows .

| Alt C Acquisition Corp. 46 Risk Factors 46. We must obtain regulatory approvals for the use of various materials in our powerhouse designs . This includes long lead time irradiation testing and analysis, which may require redesign or use of alternative suppliers if results are unsatisfactory . 47. We may require certain materials and components which are only produced in limited quantity and may be predominantly produced outside of the United States . Cultivating supply chain manufacturing capacity for key materials and components depends on supply chain partners and may require cooperation from the United States or other governments and may result in shortages and delays if not accomplished within assumed timelines or costs . 48. Unresolved spent nuclear fuel storage and disposal policy issues and associated costs could have a significant negative impact on our plans to recycle spent fuel as a potential fuel source for our powerhouses . Additionally, U . S . policy related to storage and disposal of used fuel from our power plant and/or negative customer perception of risks relating to these policies could have a significant negative impact on our business prospects, financial condition, results of operations and cash flows . 49. The nature of our business requires us to interact with various governmental entities, making us subject to the policies, priorities, regulations, mandates and funding levels of such governmental entities and we may be negatively or positively impacted by any change thereto . 50. Prospective future customers may also require that we comply with their own unique requirements relating to their compliance with policies, priorities, regulations, controls and mandates, including provision of data and related assurance for environmental, social, and governance related standards or goals . 51. Power purchase agreements are a key component to our anticipated business model for sales of power, and customers may be able to void all or part of these contracts under certain circumstances . We may need to find substitute customer power and/or heat offtake, or may need to cancel licensing work related to particular customers and sites as a result of changes in customer demand or contracts with customers . 52. Power purchase agreements may include penalties for not delivering sufficient electric and/or heat energy on schedule, which may result in liabilities and reductions in cash flow . 53. We could incur substantial costs as a result of violations of, or liabilities under, environmental laws . 54. Changes in tax laws could adversely affect our business prospects and financial results . 55. The U . S . government’s budget deficit and the national debt, as well as any inability of the U . S . government to complete its budget or appropriations process for any government fiscal year could have an adverse impact on our business prospects, financial condition, results of operations and cash flows . 56. We rely on intellectual property law and confidentiality agreements to protect our intellectual property . We may also rely on intellectual property we license from third parties . Our failure to protect our intellectual property rights, our infringement of third - party intellectual property or our inability to obtain or renew licenses to use intellectual property of third parties, could adversely affect our business . 57. Uncertain global macro - economic and political conditions could materially adversely affect our business prospects, financial condition, results of operations and cash flows . 58. We depend on key executives and management to execute our business plan and conduct our operations . A departure of key personnel could have a material adverse effect on our business . 59. Our business plan requires us to attract and retain qualified personnel including personnel with highly technical expertise . Our failure to successfully recruit and retain experienced and qualified personnel could have a material adverse effect on our business . 60. Reduction in energy demand or changes in climate - related policies may change market conditions, reducing our product’s competitiveness and affecting company performance . 61. There is substantial doubt about our ability to continue as a going concern, and we may require additional future funding whether or not the Business Combination is consummated . 62. Beginning in January 2022 , there has been a precipitous drop in the market values of growth - oriented companies like ours, particularly companies that entered into business combination agreements with SPACs . In recent months, inflationary pressures, increases in interest rates and other adverse economic and market forces have contributed to these drops in market value . As a result, our securities are subject to potential downward pressures, which may result in high redemptions of the cash available from the trust fund . If there are substantial redemptions, there will be a lower float of our common stock outstanding, which may cause further volatility in the price of our securities and adversely impact our ability to secure financing following the closing of the Business Combination . 63. Securities of companies formed through SPAC mergers such as the proposed transaction may experience a material decline in price relative to the share price of the SPAC prior to the merger .

| Alt C Acquisition Corp. Digital rendering for illustrative purposes only