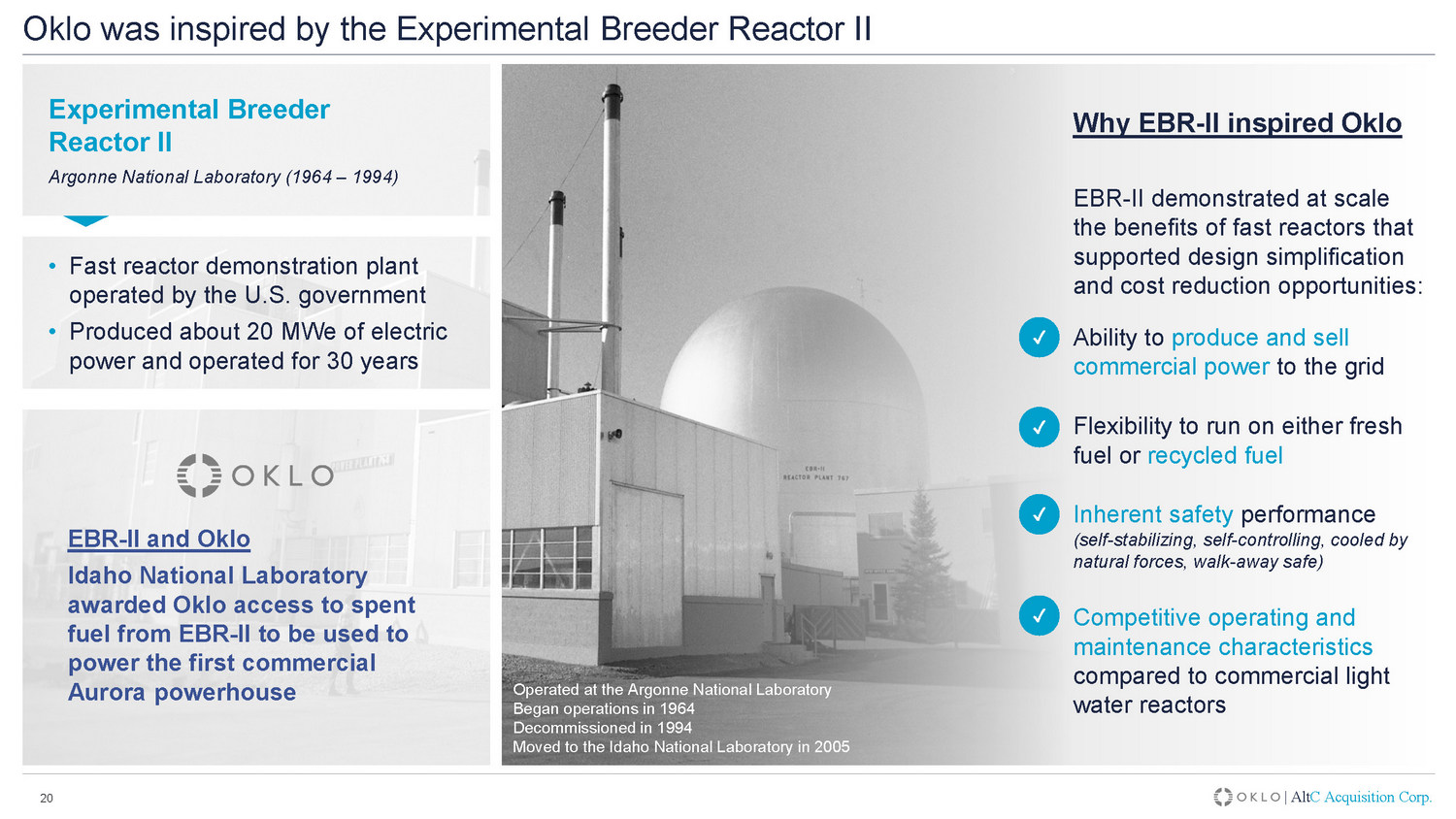

|Alt C買収20 Okloのインスピレーションは、実験増殖炉II実験増殖炉IIアゴン国立実験室(1964-1994)·米国政府が運営する高速炉モデル工場·約20メガワット電力を生産し、アルゴン国立実験室で30年運営して1964年に運営開始1994年に引退して2005年にアイダホ州国立実験室に移転した理由EBR-II啓発Oklo EBR-IIは、設計の簡略化とコスト低減機会を支援する迅速な原子炉の利点を大規模に示した:商業電力を生産し、電力網に販売電力を出荷することができる燃料や回収燃料固有の安全性能(自己安定性、EBR-IIとオクロアイダホ州国立実験室は、商用軽水炉と比較して、OKLOがeBR-II使用済み燃料の契約を取得し、最初の商用オーロラ原発に動力を供給するための契約を取得した

|Alt C Acquisition Corp.備考:(1)Okloは、15メガワットおよび50メガワットの工場規模の設計と導入に最初の重点を置いています。(2)目標プラントコストおよび建設時間は、1回目の導入を達成した後の予想稼働率操作を反映し、規制中に変化する可能性がある現在の時間およびコストの仮定に依存する。(3)緊急計画区域を含み、URORA原子炉については、発電所建築構造内に制限される予定である。21簡略化、近代的な設計方法は、工場の複雑さ、コスト、および建設時間 を低減するために、配備Aurora Powerhouse設計の簡略化をサポートします

|Alt C Acquisition Corp.ソース:エネルギー省-商業離陸の道:高度核報告書(2023年3月)、高度原子力システムセンター。注:(1)目標工場コストと建設スケジュールは、1回目の配備を実現した後の予想稼働率運営を反映し、現在の時間とコストの仮定に依存し、これらの仮定は規制過程で変化する可能性がある。(2)エネルギー省の分析によると、先進原子炉の隔夜資本コストは3,600ドル/キロワット。(3)AP-1000に基づく隔夜資金コスト。22製品の複雑さとコストを低減することによって所有者を実現-事業者モデルOkloは、Aurora発電所を建設、所有、運営しようとしている-原子炉設計は、コスト、土地、材料、および施工時間の優位性がより低いと予想される工場コストがより小さい敷地面積の複雑さを実現し、独特のビジネスモデル15 MWe工場生産能力(技術が50 MWeに拡張される可能性がある)x を迅速に設置する

|Alt C Acquisition Corp.備考:(1)本明細書に記載された単位経済は、任意の潜在的利益率上昇を含み、前向き情報であり、一定の未来の結果を示すことに依存すべきではない。実際の結果は大きく異なるかもしれない。(2)2023年7月7日までFactSetからのMark ET資本化を反映する.23魅力的なビジネスモデルは、注目される経常的収入Okloが世界の電力市場で広く使用されている収入モデルを追求していることが予想され、長期契約に基づいて電力株主機会収入モデルが市場で検証され、Okloの株主価値主張x大規模市場機会-Okloの目標は、未解決の分散電力網使用例(例えば、データセンター、国防)x繰り返し出現し、時間とともに増加すると予想される長期契約収入x収入源は、競争相手の脱媒x工場運営1年目の予想利益単位経済(1)x高再現性で単位成長を推進し、より高い生産バージョンを発売することが予想される(例えば、50メガワット)x燃料回収は、潜在的な将来の利益率向上と新たな収入源国家重点市場価値を提供することができる(2)デンマークカナダフランス風力エネルギー多様化風力/太陽エネルギー約400億ドル~140億ドル~50億ドル~50億ドル~30億ドル~20億ドルポルトガル風力/太陽エネルギー約200億ドル

|Alt C Acquisition Corp.注:(1)すべての規制部門が予想される時間内に承認されたと仮定する。NCESary NRCの承認と許可を含む規制プロセスは、長く複雑なプロセスであり、予想されるスケジュールは、すべての必要な承認を得るのに要する実際の時間とは大きく異なる可能性がある。15メガワットと50メガワットのe A urora発電所の資本コストをそれぞれ2,400万ドルと6,100万ドルとし,1発電所当たりの寿命を40年とする。いずれもNOAK状態にあると仮定する.単位経済効果は実数値で表される.なお,ここで提供する単位経済性は説明目的にのみ用いられている。実際の結果は大きく異なるかもしれない。詳細については、スライド37−40を参照されたい。24潜在的な上昇の可能性を有する納得できる予想ユニット経済性説明ユニット経済性:15 Mwe Aurora発電所(1)累計40年ユニット経済性(百万ドル)$288$198$1,452$1,163$966電力販売からの収入運用費用工場利益資本コスト工場利益資本コスト工場キャッシュフロー資本コスト累積$198 80%5.0 x$120$107$107$388$281電力販売からの収入運営費工場利益資本コストプラントキャッシュフローコスト累積$107·初期工場コスト:$24·初期燃料コスト:$33·給油コスト:$50%75.5 x説明的経済性:50我々オーロラ発電所(1)累積40年間の経済性経済学(百万ドル)·初期工場コスト:61ドル·初期燃料コスト:55ドル·給油コスト:82 75%2.5倍工場潜在寿命利益率潜在キャッシュフローと資本コスト潜在上りレバー:x燃料回収x投資税収控除80%5.0 x工場潜在利益率潜在工場キャッシュフローと資本コスト潜在上りレバー:x燃料回収x投資税控除

|Alt C Acquisition Corep.25優勝価値主張OKLO価値主張を加速させるためのOKLO価値主張700メガワットを超える非拘束性志向潜在顧客OKLOターゲット市場顧客希望-環境および運営目標を満たす工場を所有/運営するのではなく電力購入-低資本支出ソリューション-負担可能で信頼できる無炭素エネルギーの獲得-検証された技術は低実行および運営リスクOKLO価値はxの潜在的なゼロ前期顧客コストを主張し、xの信頼性が高く、負担のかかる長期契約でのゼロ排出エネルギーの採用を加速し、グローバル電力市場で検証された標準モデルxすでに大規模データセンター、国防工場、工業離網/農村公共事業が潜在顧客と積極的に対話する底技術

|Alt C Acquisition Corp.26はアイダホ州国立実験室の配備先に3つのエキサイティングなプロジェクトを進め、15メガワット原子力発電所の初期燃料負荷を確保した。南オハイオ州アイダホ州国立実験室オーロラ発電所(15メガワット)1オクロと米国エネルギー省と了解覚書に調印する機会があり、アイダホ州国立実験室でアウトローに現場使用許可証を発行し、アイダホ州国立実験室はアウトロ2017 2019 2021 2024-26 2026/27 2020オクロに米国エネルギー省の現場使用許可オーロラ発電所の配向審査申請を得て審査を受けた(1)国家エネルギー局によるオクロサプライチェーン発展の審査期間を予定しており、最初の電力生産燃料安全場xと南オハイオ州多様化イニシアティブ(SODI)のパートナー関係の決定を目指している(2)5月18日発表2023年x南オハイオ州に2つの商業オクロ発電所を配備する非拘束的約束が決定した·工場はクリーン電力と暖房を提供する予定であり、拡大する機会がある·これらの工場は地域の雇用創出を支援している。経済多元化とクリーンエネルギー解決策の推進を通じて、オハイオ州南部コミュニティの生活の質·SODIを改善するためにSODIの使命をさらに推進し、先進的な原子炉技術の導入と使用前オハイオ州原発遺跡南オハイオ州多元化イニシアティブの2つのAurora発電所(各15 MWe)2-3注:(1)米国核管理委員会(NRC)を支援するために、米国エネルギー省原子力事務室から資金を提供している。(2)南オハイオ州多様化イニシアティブ(SODI)の使命は,経済多様化,開発エネルギー省ポーツマス(DOE)ポーツマス天然ガス拡散工場跡地が十分に利用されていない土地や施設,および現地政府を支援し続けることにより,ジャクソン県,パーク県,ロス県,ショトー県の生活の質を改善することである。

|Alt C Acquisition Corep.27は、Okloの初配備がすべての高度であることを支援するために、密な規制を行っています。非軽水炉会社が初めて提出した先進原子炉共同許可証申請x 2016年に開始されたNRCプロジェクトx 2020年3月に提出されたCola xは、2020年から2022年までのコーラ審査中にNRCスタッフとの深い接触x貴重な経験を利用して次の申請x NRCがOkloの品質保証計画を承認することに成功したことは、緊張している作業中に次の申請を提出する準備ができていることを示しており、xの大幅な拡大許可と監督チームは、内部導入前のNRCスタッフと監督専門家-Oklo既存従業員の10%近くが元NRC従業員xがよく参加していることを示している。2022-23-9年度重要な許可テーマについて開催された正式な申請前会議-70回以上の調整会議が開催された-50件以上の許可文書を共有したx Okloは2024年までに申請審査x 2024年末/2025年初めに申請x Okloを提出してNRCスタッフの勤勉な仕事と安全核解決策を推進する約束を深く賞賛·コカ·コーラはNRCの許可経路であり、建設許可と運営許可証を組み合わせた·OkloはNRC審査を提出した史上初めての先進原子炉会社·2022年、NRCはOklo‘s Colaを拒否し、審査·Okloが審査中に貴重な経験を得たことを回復するためにより多くの情報を提供することを要求し、NRCの応答を利用して規制パターンを強化する

|ALTC Acquisition Corp.備考:(1)米国エネルギー情報管理局(ウランマーケティング年度報告-2022年)。(2)エネルギー省(使用済み核燃料に関する5つの快評価)。28燃料回収上り機会オクロ大量の使用済み燃料在庫オクロ設計優位性独特の上り機会燃料供給制限米国は現在新鮮な核燃料の輸入に依存しており、2022年には米国の原発95%(1)のウランは外国由来であり、米国原発の33%(1)のウラン濃縮サービスはロシアから米国を購入してHALEUの生産を制限している。先進原子炉の燃料有限米国の燃料能力は先進原子炉発展の喫緊の問題であり、米国は大量かつ増加している使用済み燃料在庫管理コストが高い米国の原子炉は1950年以来90,000トンの使用済み燃料を生産している(2)毎年2,000トンの使用済み燃料が発生している(2)使用済み燃料は現在35州の70原子炉地点に貯蔵されている(2)使用済み燃料管理が複雑である。新しい原子炉の配備に伴い、需要が増加し、使用済み燃料はそのエネルギー潜在力を維持し、x燃料を回収して回収することができ、他の国でそうすることができる。例えばフランスxが既存の原子炉で使用された後、潜在エネルギーの90%以上が使用済み燃料に残っている(2)米国では燃料供給制限および使用済み燃料在庫を解決するための燃料を回収する機会がない循環高速炉は、新鮮または回収燃料x ebr-IIを使用して、高速炉が回収燃料を使用する能力を示しているx Oklo工場は、新鮮または回収燃料x ebr-iiから回収した使用済み燃料を燃料とする最初のオーロラ発電所燃料回収を柔軟に使用するように設計されており、将来の利益率の向上と新しい収入源Okloを開発している燃料回収能力x廃棄物をクリーンエネルギーx選択エネルギーに変換する。エネルギー省と協力して燃料回収技術を開発する4つのプロジェクトのうち、2030年までに米国に商業規模の燃料回収施設を設立することが初歩的な計画である。S·オクロは燃料回収分野で業界をリードする可能性がある

|ALTC Acquisition Corp.米国原子力発電所は輸入核燃料核燃料輸入に大きく依存している|ALTC Acquisition Corep.29米国原子力発電所のウラン源(酸化ウラン,百万ポンド)(1)注:(1)米国エネルギー情報管理局(核解釈-我々のウランはどこから来たのか)。(2)米国エネルギー情報庁(UEA)(ウランマーケティング年度報告-2022年),(3)Orano(廃燃料加工·回収に関するすべての情報)。発展し続ける地政学的懸念2022年、米国原発95%(2)ウラン海外から2022年、米国原発に必要な外国ウラン濃縮サービスの33%(2)ロシアから0 20 40 60 80 1950 1960 1970 1980 1990 2000 2010 2020国内生産購入輸入燃料回収は米国の輸入燃料回収を減少させる可能性がある米国は現在使用済み燃料を回収しないが、燃料は回収でき、また他の国でも回収可能であり、例えばフランスの10分の1近くの電球を使用して回収された核材料(3)

|Alt C Acquisition Corep.30燃料回収は、潜在的な将来の利益率向上と新たな収入源の潜在的な機会を提供し、施設を設立·運営することができ、Aurora発電所および第三者顧客に回収燃料使用済み燃料回収を供給することは、Okloにとって重要な潜在的コスト節約機会であり、工場の初期資本コストを低減し、持続運転コストを垂直に統合することができる燃料源は、Okloの回収方法を提供し、花火処理を使用する。使用済み燃料管理サービスの販売と各種端末市場への副産物や特殊同位体の販売により潜在収入源燃料回収を増加させることで市場の長期的な問題を解決し、持続可能な競争優位性を創出することができる成熟した技術であり、Okloは2023年1月に核管理委員会に商業規模の燃料回収施設許可プロジェクトを提出し、燃料回収が電気化学的に燃料材料を分離して原子炉内で動力を発生させ、溶解燃料破砕用燃料1 2 3 4 5 5を鋳造することにより燃料回収を計画する

Alt C Acquisition Corp.31 Okloは、燃料回収の面で業界をリードする可能性がある。Okloはエネルギー省に4つのコスト共有賞に選ばれ、回収技術を潜在的に商業化するOkloの回収技術開発プロジェクト技術商業化基金xキー回収プロセスの効率改善のための先進的なセンサARPA-E Open xを開発し、機械学習とデジタルペアを利用して回収効率と材料責任を向上させるARPA-E xから回収プロセスの終了を実演する。-端まで行って、旧酸化物燃料を金属に変換することを示す商業規模燃料回収装置ARPA-E Curie xの技術基盤を開発し、既存の船団の廃棄物を先進的な原子炉燃料にリサイクルできる

32深さと差別化された“ハードテクノロジー”、核工学、規制専門知識…経験豊富なチーム創始者が率いる組織と深い技術専門知識と経験豊富なチームx Okloのチームはフォーチュン500強とグローバル会社から来ており、政府と科学背景xは多くの業界の専門知識と経験を集めて、先進的なエネルギー製品(例えば、原子力、航空宇宙、自動車と科学技術)Jacob DeWitte共同創業者兼最高経営責任者は2013年にOkloを共同創立し、Caroline Cochranは2013年にOkloを共同創立した·核技術面で15年以上の経験を持つ·マサチューセッツ工科大学核工学博士号を持つ·GE、Sandia National Labs、Urenco、Urenco、米国海軍核実験室·15年以上の核技術経験·核工学修士、マサチューセッツ工科大学·前国防長官室と米エネルギー省原子力諮問委員会創始者率いる組織…8人の博士(16%)と20人の工学/科学修士(39%)を含む51人の従業員が、前回の許可プロセス以来、複数のエンジニアと監督の専門家がOkloチームに参加し、6人の元NRCスタッフがリードしたハード技術投資家を含む取締役会への次の申請提出に協力した

|ALTC買収会社33は、原子力の切実な需要に後押しされて、強力な政策支援を提供し、簡略化された現代的な設計方法を展示された技術的に魅力的なビジネスモデルに適用し、利益の経常的収入の利益価値を主張し、顧客の採用場所と初配備で得られた燃料埋め込み独自の燃料回収機会を加速させるための潜在的な上り優位性の強い創業者チームの深い技術専門長を主張しており、私たちの使命は、世界的にクリーンで信頼性の高いエネルギーを提供することであり、私たちの使命は、世界的にクリーンで信頼性の高いエネルギーを提供することであり、ALTCの“ハード技術”投資の重点が一致している理由を説明するために、なぜ1 2 3 4 5 6 7 OkloのAurora houseデジタルレンダリングを投資するのかを説明するために、

|Alt C Acquisition Corp.Oklo履歴1取引情報Oklo財務情報2 3サポート素材デジタルレンダリングは説明目的のみ

|Alt C Acquisition Corp.35 Oklo開発成功の強力な記録に基づいて2013 Oklo設立2014 Oklo 2015年からシードラウンドOklo Sam Altman率いる第2ラウンドシードラウンドと&2016 Okloが先頭に立った最初のAラウンドとNRC 2017から正式な事前申請プログラム2017 Okloは、重力鋳造を用いて燃料プロトタイプを製造する能力2018 Okloパイロットがサンディア国立実験室でNRC熱テストを行って2019年にエネルギー省がOkloにエダホ国家実験室の現場使用許可証を発行し、エダホ州国立実験室にOklo燃料材料2020 OkloをNRCに提出する新規な組み合わせ組み合わせ許可証承認Oklo品質保証許可証をNRCに発行した。2021年にOkloはアイダホ州国立研究所にあるAurora発電所の現場特定許可を取得し、2023年にOkloはNRCに商業規模の燃料回収施設許可プロジェクト計画Okloを提出し、Okloは南オハイオ州多様化イニシアティブ(SODI)と協力してオハイオ州に2つの工場を設立することを発表し、2024/2025年OkloはNRCに更新された組合せ許可申請をNRCに提出する計画であり、2026/2027年Oklo目標はアイダホ州国立実験室の初の配備と電力生産の深い技術的背景である。強固なパートナー関係と密集した規制参加

|Alt C Acquisition Corp.Oklo履歴1取引情報Oklo財務情報2 3サポート素材デジタルレンダリングは説明目的のみ

|Alt C Acquisition Corp.37単位経済学的説明:Aurora Powerhouse(15 MWe)Okloは、予想累積工場キャッシュフローは予想累積資本コストの2.5倍以上に等しいとしている:(1)予想Noak(n番目)工場の重要な仮定に基づいている。(2)すべての規制承認が予想時間内に完了したと仮定する。必要なNRC承認および許可を含む規制プロセスは、長く複雑なプロセスであり、予想されるスケジュールは、すべての必要な承認を得るのに要する実際の時間と大きく異なる可能性がある。単位経済学は実際の方式で新聞を列報し,2023年5月までに新聞を列記する.本稿で提供する単位経済性は参考にするだけである。実際の結果は大きく異なるかもしれない。(3)FOAK(初回)工場資本支出は3400万ドルと予想される。(4)は92%容量係数での15メガワット発電能力を表す。Aurora Powerhouse(15メガワット)(2)0 50 100 150 2年4年6年8年10年説明的年度導入(単位)低高·40年工場設計寿命·工場資本支出:−初期工場建設コスト約2,400万ドル(初期燃料負荷を除く)(3)·燃料資本支出:−初期燃料負荷4,750 kg−40年工場設計寿命内に10年当たり燃料負荷2,375 kg−Oklo回収燃料を内部供給に使用しないと仮定しない。すべての燃料が7,000ドル/kgのコストで第三者サプライヤーから購入した新規製造HALEU·年間電力販売収入を仮定する:年間発電量を約121,000メガワット時(4),経常収入を約1300万ドル,平均実電力価格を105ドル/メガワット時·運営コスト:−年間固定費用240万ドル−年間可変費用5.00ドル/メガワット時T+0 T+1 T+2 T+3 T+4 T+5 T+10 40年工場寿命(百万ドル)資本支出(57ドル)(17ドル)(107ドル)工場建設(24ドル)(24ドル)燃料資本支出($33)($33)燃料資本支出($17)($50)収入$13$13$13$13$13$508電力販売収入$13$13$13$13$13$508費用($3)($3)($3)($3)($3)($3)($3)($120)固定設備($2)($2)($2)($2)($96)可変設備($1)($1)($1)($1)($1)($1)($1)($1)($1)($1)($1)($1)($1)($1)($1)($1)$1)($24)年間工場キャッシュフロー($57)$10$10$10($7)$281現金利益率NA 76.4%76.4%76.4%(54.4%)55.4%主な仮定(1)(2)オーロラ15 MWe説明的経済学(1)(2)

|Alt C Acquisition Corp.38単位経済学的説明:Aurora Powerhouse(50 MWe)Okloは、予想累積工場キャッシュフローは予想累積資本コストの5.0倍以上に等しいとしている:(1)予想Noak(n番目)工場の重要な仮定に基づいている。(2)すべての規制承認が予想時間内に完了したと仮定する。必要なNRC承認および許可を含む規制プロセスは、長く複雑なプロセスであり、予想されるスケジュールは、すべての必要な承認を得るのに要する実際の時間と大きく異なる可能性がある。単位経済学は実際の方式で新聞を列報し,2023年5月までに新聞を列記する.本稿で提供する単位経済性は参考にするだけである。実際の結果は大きく異なるかもしれない。(3)Foak(スタートアップ)工場資本支出は8600万ドルと予想される。(4)は92%容量係数での50メガワット発電能力を表す。·40年工場設計寿命·工場資本支出:−初期工場建設コストは約6,100万ドル(初期燃料負荷を除く)(3)·燃料資本支出:−初期燃料負荷7,800 kg−40年工場設計寿命では10年ごとの給油負荷3,900 kg−Oklo回収燃料の内部供給は想定していない。すべての燃料を新たに製造したHALEUを想定し,7,000ドル/kgのコストで第三者サプライヤーから購入·年間電力販売収入:年間発電量を約403,000メガワット(4),平均実電力価格を90ドル/メガワットとした場合,経常収入は約3,600万ドル·運転コスト:−年間固定費用560万ドル−年間可変費用4.00ドル/メガワット時仮説(1)(2)Aurora 50 MWe説明経済性(1)(2)T+0 T+1 T+2 T+3 T+4 T+5 T+10 40年工場寿命(百万ドル単位)(116ドル)(27ドル)(198ドル)工場建設(61ドル)(61ドル)燃料資本支出(55ドル)(55ドル)燃料資本支出(27ドル)(82ドル)収入$36$36$36$1,452電力販売収入$36$36$36($36)($7)($7)($7)($7)($7)($7)($7)($7)($7)($7)($7)($7)($7)($8)固定工場($6)($6)($6)(6)$(6)(6)$(6)$(6)$(6)(6)$2($2)($2)($2)($2)($2)($65)年間工場キャッシュフロー($116)$29$29$29$2$966現金利益率NA 80.1%80.1%66.5%オーロラPowerhouse(50メガワット)(2)0 50 100 150 2年4年6年8年10年度説明的配置(単位)低い

|Alt C Acquisition Corp.バブルNoak工場への投入資本コスト(ドルmm)は約0.5%。約34.0ドルです。24.0ドルの燃料資本支出初期燃料負荷(Kg)5,000,750初期燃料資本支出(ドル)に近い。約35.0ドルです。$33.0給油負荷(Kg)2,500 2,375給油資本支出(ドル)(2)に近い約53.0ドルです。$50.0運用コスト年間固定料金(ドル)$3.8$2.4年間可変料金(ドル/メガワット時)$6.00$5.00注:(1)すべての規制部門が予想されるタイムラインで承認されたと仮定します。国家核管理委員会の承認·許可を含む規制プロセスは、長く複雑なプロセスであり、必要なすべての承認を得るのに要する実際の時間とは大きく異なる可能性が予想される。ここで提供する単位経済性は説明目的のみに用いられる。実際の結果は大きく異なる可能性があり,(2)20台ユニットの運転率はNOAKユニットの経済性実現の期待要求であり,(3)40年の工場設計寿命内の総給油資本支出を反映している。39説明的発泡ノックユニット経済学的概要オーロラ発電所(15メガワット)(1)(2)オーロラ発電所(50メガワット)(1)(2)バブルノーク工場への投入資本コスト(ドルmm)に近い。約86.0ドルです61.0ドルの燃料資本支出は初期燃料負荷(Kg)8,000 7,800初期燃料資本支出(Mm)に近い。約56.0ドルです$55.0給油負荷(Kg)4,000,900給油資本支出($mm)(2)に近い約84.0ドルです。$82.0運用コスト年間固定料金(ドル)$7.2$5.6年間可変料金(ドル/メガワット時)$5.00$4.00

|Alt C Acquisition Corp.40その他財務情報仮説コメント一般と行政費用·初回導入前:2024年には約1,950万ドル、2027年には約3,450万ドルに増加·長期仮定:電力収入の約20%を占める製造施設支出·Okloの製造·製造能力を反映してAuroraパワープラント配備を支援するために必要な支出·2030年までの工場製造施設資本支出約4,000万ドル(1)維持支出·約10%の初期工場資本支出10年あたり占有費用·収入運営資金の約5.0%·約4.0%の電力収入付記:(1)潜在的な燃料製造または回収投資は含まれていない。

|Alt C Acquisition Corp.Oklo履歴1取引情報Oklo財務情報2 3サポート素材デジタルレンダリングは説明目的のみ

|Alt C Acquisition Corp.ソース百万ドル516 38%既存Oklo株主850 62%総ソース1,366 100%百万ドル現金を貸借対照表478 35%既存Oklo株主850 62%イラスト費用383%総使用1,366 100%注:(1)2023年6月30日現在、ALTC信託現金は515,791,749ドルである。説明目的だけでは,(2)ALTC株主が償還権を行使していないと仮定して取引終了時に信託口座から現金を受け取る,(3)取引前払い持分価値を提案するが,業務合併終了前に会社融資を許可する潜在的成長に制限されなければならない。業務合併終了時には、1株10ドルの価格で貨幣前株式価値を転換する。潜在的プレミアム株式の影響は含まれておらず、(4)ALTC信託現金から例示的な費用および支出が減算され、(5)発行されたすべてのALTC A株が含まれる。終値時に帰属していない625万株のB類方正株の潜在的な希薄化影響と、終値後60日のうち20日間株価が1株10ドル以上に維持されている場合、Sは帰属される。B類方正株312.5万株(1株12.00ドル)と312.5万株B類方正株(取引終了後5年以内に1株当たり14.00ドルと16.00ドル)の影響は含まれていない。42取引Okloに対する現金前株式価値は8.5億ドルであり、クリーンエネルギー上場取引よりも取引源の半分を推定でき、形式的な取引ハイライト(1)(2)(4)提案取引概要(3)(3)1株当たり10ドル(百万)%所有権既存Oklo株主85 60%ALTC株主58 40%総供給源143 100%(3)(1)(5)·貨幣前株式価値8.5億ドルとする。これはクリーンエネルギー上場取引価値の約半分·Oklo既存株主が最大1500万株の利株を獲得でき、取引完了後5年間にそれぞれ1株12.00ドル、14.00ドル、16.00ドルの価格でOklo株主·Oklo株主に既存株を100%転がし·取引費用を差し引いて調達したすべての収益である。Okloの貸借対照表に直接進出し、その業務計画の加速とAurora Powerhouseの初配備に資金を提供する·ALTCスポンサーが100%保有する株式を業績帰属·Oklo創業者とALTCスポンサーの株を業務合併完了後3年以内に交互にロックする

|Alt C Acquisition Corp.付記:(1)プレミアム株式および融資許可の調整は含まれていません。43公衆投資家、ALTCスポンサーと既存のOklo株主との間の長期利益が一致する簡単な取引構造·Oklo株主は、合併後の会社の8500万株(1)を取引の一部として獲得し、Oklo株主は現金収益を受け取ることができない·5年間で株価が20%~60%上昇した場合、最大1500万株の現金現金株を得ることができる。株価が上昇すれば、Oklo株主に上り収益を提供することで、取引価値を魅力的なレベルに設定できるようにする·ALTCスポンサーは、業務合併終了時に100%の方正株を放棄し、株価が上昇しない限り、その株を回収しない·Oklo創業者とALTCスポンサーの株は、業務合併終了後3年以内に互い違いにロック·強力な上場企業統治下での運営に取り組む·専門知識のある取締役会を結成する。取引完了後、オクロとオクロが共同で指定した一方の取締役と、オクロとオクロが共同で指定したもう1つの取締役は単一種類の株を持ち、すべての株主は平等な投票権を持つ·簡潔はオクロ精神の核心である端的な会社構造であり、オクロの既存株主だけに利益を与える特殊な合意なし×オクロに投資されたすべての取引収益純額である。Oklo株主x Oklo株主にキャッシュされていない100%既存株式スクロールx altc発起人は、100%保留株式を業績帰属x Oklo創始者とaltcスポンサー長期ロックx公開市場で成熟したビジネスリーダーと価値創造者を支援するために設立された取締役人材取締役会xすべての株主に平等な投票権を提供する単一カテゴリ株x複雑な会社構造や特別株主税協定Oklo株主が100%既存株式を合併後の会社altc保証人にスクロールして業績プレミアム株式を取得する資格のあるOklo株主は100%保留株式を行う。業績帰属Oklo創始者とaltc発起人の長期ロック取締役人材のリード管理と取締役会単一カテゴリ株式の複雑な会社構造や特殊な株主税務プロトコル取引構造優先公共投資家の利益提案の取引構造

|Alt C買収会社44リスク要因1.当社のビジネス計画には大量の投資が必要です。提案された業務合併に重大な償還が生じた場合、私たちは私たちの業務計画を重大に調整したり、追加資本を求めたりする必要があるかもしれません。私たちが利用可能な資本資源によると、私たちは予想される短期支出を延期または停止する必要があるかもしれません。これは、私たちのいくつかの他の戦略目標を達成する能力を制限し、および/または、私たちの設計、販売、および製造作業をさらに発展させるために使用できる資源を減少させ、それによって、私たちの業務の見通し、財務状況、運営結果、およびキャッシュフローに大きな影響を与えるかもしれません。2.私たちの業務計画を達成するためには、提案された業務統合によって生成された任意の資金に加えて、追加の資金が必要です。このような資金は私たちの投資家を希釈するかもしれないし、そのような資金の利用可能性や条項を保証することはできない。どのような融資や関連条項も、このような融資を求める際の市場状況と私たちの業務の進展に高く依存するだろう。私たちが予想する会社の支出と私たちの利益を実現する能力は、インフレの影響、変化する規制要求、原材料と核燃料供給、世界的な衝突、グローバルサプライチェーンの挑戦と部品製造とテストの不確定性、現地と国内のエネルギー政策、国際エネルギー政策、国際貿易政策、政府契約と調達ルールなどに関する不確実性を含む多くのリスクと不確定要素の影響を受ける。4.インフレおよびコスト上昇は、私たちに比例しないより大きな影響を与える可能性があります。材料コスト、労働力或いはその他のインフレ或いは経済駆動要素の影響は原子力とエネルギー転換業界全体(太陽と風力のような再生可能エネルギーを含む)に影響を与えるが、業界全体の相対的な影響は同じではなく、業界内の具体的な影響は多くの要素に依存し、材料使用、技術、設計、供給プロトコル構造、プロジェクト管理とその他の要素を含み、これらの要素は私たちの技術の競争力と私たちの動力設備を販売する能力に重大な変化をもたらす可能性があり、これは私たちの業務の将来性、財務状況、運営結果とキャッシュフローに実質的な不利な影響を与える可能性がある。5.私たちは初期段階の会社で、財務赤字の歴史があります(例えばg。負のキャッシュフロー)は、少なくとも私たちの動力会社がビジネスが可能になる前に、巨額の費用と持続的な財務損失を招くことが予想されますが、これは決して起こらないかもしれません。6.成長を効果的に管理できない場合、ビジネス計画を実行できない可能性があり、ビジネスの見通し、財務状況、運営結果、およびキャッシュフローに大きな悪影響を及ぼす可能性があります。7.私たちはまだ発電所を販売していませんし、いかなる顧客とも拘束力のある電力または熱供給契約を締結していませんし、将来そうできる保証もありません。限られたビジネス運営の歴史は、私たちの将来性と私たちが直面する可能性のあるリスクと挑戦を評価することを困難にする。8.私たちのビジネス計画には、投資税控除、生産税収控除、または他の形態の政府資金を使用して、私たちの強国の商業発展に資金を提供することが含まれていますが、私たちのプロジェクトがこれらの免除を受ける資格があることは保証されていませんし、将来の政府資金が利用できる保証もありません。9.我々の動力装置を市場に投入するのに要する時間と資金は、私たちの予測を大幅に超える可能性がある。10.多くの要因により、プレハブ程度、標準化、現場施工、長期調達、請負業者の業績、工場資質テスト、および他の現場の具体的な考慮要因を含む、発電所の建設および交付スケジュールの推定が増加する可能性がある。11.我々は現在、発電所の交付および業績に関連するリスクを低減するために、リスク分担構造を採用していない。私たちが初めての商業配信で遭遇する可能性のあるいかなる遅延や挫折、あるいは未来の注文のための最終投資決定を得ることができなかったことは、私たちの業務の将来性、財務状況、運営結果、キャッシュフローに重大な悪影響を与え、私たちの名声を損なう可能性があります。12.13.我々のビジネス計画および収益性を達成する能力は、私たちの2つの動力構成(15メガワットおよび50メガワット)の同時開発に依存し、このような並列開発方法によって引き起こされる学習、効率、および規制承認についていくつかの仮定がなされており、この仮定は不正確または不正確である可能性がある。これらの仮定のいかなる不利な変化も、私たちの業務の見通し、財務状況、経営業績、キャッシュフローに重大な悪影響を及ぼす可能性があります。14.我々のビジネス計画および収益性を達成する能力は、当社の動力装置(100メガワットまたは他の規模)の他の構成の発展にも依存し、このような新しい開発方法によって生じる学習、効率、および規制承認について何らかの仮定をすることができ、これは不正確または不正確である可能性がある。これらの仮定のいかなる不利な変化も、私たちの業務の見通し、財務状況、経営業績、キャッシュフローに重大な悪影響を及ぼす可能性があります。15.私たちのコスト予算は、より広い経済的要因に非常に敏感であり、コストをコントロールまたは管理する能力が限られている可能性があります。Auroraのような随一の発電所を配備する資本と運営コストは予測が困難であり、本質的に可変であり、現場の特定の要素、顧客の購入要求、監督監督、運営協定、サプライチェーンの可用性、サプライチェーンの可用性が原子炉と発電所の性能に与える影響、インフレ、その他の要素を含む様々な要素によって大きく変化する。16.後続の配備が費用を削減する機会もまた不確定です。予想される時間枠または振幅でコスト低減を達成できない場合、Auroraは代替技術と比較してコスト競争力を有することができない可能性があり、これは、私たちの業務の将来性、財務状況、運営結果、およびキャッシュフローに大きな悪影響を与え、私たちの名声を損なう可能性がある。17.我々の核燃料を市場に大規模に投入するのに要する時間および資金は、私たちの予想をはるかに超えている可能性がある。18.先進的な核分裂エネルギーの市場はまだ確立されておらず、私たちの予想される成長潜在力を達成できない可能性があり、または成長速度が予想よりも遅く、新しい技術または既存技術の新しい応用によって代替または淘汰される可能性がある。19.米国の回収核燃料市場はまだ確立されておらず、予想される成長潜在力を達成できない可能性があるか、または成長速度が予想よりも遅い可能性があるため、回収への投資がずれている可能性がある。20.私たちと私たちの顧客は政治的に敏感な環境で運営されており、核分裂エネルギーに対する大衆の見方は私たちの顧客と私たちに影響を与える可能性がある。二十一私たちの技術は規制承認が必要であり、規制要求、プロセス、およびこれらの技術能力を監督する放射性材料の処理と使用に影響を与える政策は変化する可能性があり、規制承認が得られないようにし、それによって私たちの業務に不利な影響を与える。

|Alt C Acquisition Corep.45リスクファクター22。私たちの業務計画は、政府と政府の付属実体との契約に関連しており、契約手続き、規則、法規のいかなる変更や遅延も、私たちの工場の建設と運営の時間枠を延長する可能性があり、これは私たちの業務に実質的な悪影響を及ぼす可能性があります。二十三事故、テロ行為、または他の放射性材料に関連する高調事件を含む米国または世界の原子力施設に関する事故は、原子力安全、私たちの顧客、および私たちが経営する市場に対する公衆の見方に実質的な悪影響を及ぼす可能性があり、これらの悪影響は、原子力の需要を減少させ、規制要件およびコストを増加させ、または私たちの業務に重大な悪影響を及ぼす可能性のある責任またはクレームをもたらす可能性がある。24.私たちのコスト推定は合理的だと信じていますが、サプライチェーンの可用性、製造コスト、規制過程における私たちの進展、あるいは他の要素(特に私たちの動力設備に影響を与える意外なコストの増加を含む)を考慮した後、設計成熟度の向上に伴い、コストが大幅に増加する可能性があります。二十五規制や建設の複雑さを含む多くの要因により、新たな燃料製造施設を建設することは挑戦的であり、より長い時間または我々が予想しているよりも高いコストを要する可能性がある。26.私たちはまだ第三者のコスト試算も求めていませんが、将来的にはそうなると予想されています。このような第三者コスト推定は、私たちの現在の見積もりよりも大幅に高くなる可能性があり、これは、当社の各社の即売性、および私たちのビジネス計画と将来の収益性に対する期待27に影響を与える可能性があります。二十八このタイプ,配置,規模の金属燃料高速炉の操作経験は,既存の大型軽水炉に比べて限られている。これは、予想よりも高い建設コスト、配備スケジュール、保守要件、異なる電力出力、およびより大きな運用費用をもたらす可能性がある。29。従来の電力や熱供給応用と比較して、遠隔環境や工業応用で原発を運営するには追加のリスクとコストがある。このような配備には、許可手順、工場構成制御、最低オペレータ、訓練、安全インフラ、放射線防護、政府報告、および核保険に関連するコストを含む追加のコストが必要となる可能性があり、これらのすべてのコストは、技術の競争力を後退させるか、または低減させる可能性がある。30.既存または新しい競争相手や技術からの競争は、価格の下振れ圧力、顧客の注文減少、利益率の低下、新しいビジネス機会を利用できない、市場シェアの喪失に直面する可能性がある。31。新しい代替無炭素エネルギー発電技術の商業化成功または既存の代替無炭素エネルギー発電技術のさらなる増強、例えば化石燃料発電所、風力エネルギー、太陽エネルギーまたは核融合における炭素捕獲と隔離/貯蔵メカニズムを増加させることは、より費用対効果が証明されるか、あるいは世界のエネルギー市場により魅力的であることが証明される可能性があるため、市場需要と目標発電所の商業化に成功する能力に悪影響を及ぼす可能性がある。32。私たちの発電所で発生する電力および熱エネルギーのコストは、他の源から発生する電力および/または熱エネルギーのコスト競争力を持たない可能性があり、他のエネルギーに対してプレミアムを徴収できる保証はありません。これは、私たちの業務の見通し、財務状況、運営結果、およびキャッシュフローに重大で不利な影響を与える可能性があります。33.石油、天然ガス、その他の形のエネルギーの供給とコストの変化は動揺した市場状況の影響を受け、これは私たちの業務の見通し、財務状況、経営業績、キャッシュフローに悪影響を及ぼす可能性がある。三十四私たちは限られた数の供給者に特定の材料と供給の部品を提供することに依存しており、その中のいくつかは高度に特化されており、私たちの発電所のために設計された唯一無二または独占的に使用されている。私たちと第三者サプライヤーは、私たちの製造および運営ニーズを満たすために十分な材料または供給されたコンポーネントを得ることができないかもしれません、またはそのような材料を割引条件で得ることができません。35歳。S。連邦と州レベルの政府当局はアメリカを含む。S。原子力管理委員会(“NRC”)と、私たちがその中に業務を設立する可能性のある他の司法管轄区域の規制機関。私たちの運営や業務計画は、政府の政策や優先順位の変化の大きな影響を受ける可能性がある。36。私たちの業務は厳格なアメリカの法律によって制限されている。S。輸出規制の法律法規。このような法律法規の不利な変化やアメリカ。S。政府の許可政策は、私たちがタイムリーな使用を保障できなかった。S。政府がこれらの法律と法規の許可に基づいて、あるいは私たちがこれらの法律と法規を遵守できなかったことは、私たちの世界的な拡張能力に重大な悪影響を与え、それによって私たちの業務の将来性、財務状況、運営結果、およびキャッシュフローに影響を与える可能性がある。37.政府機関予算の変化や国家実験室や他の政府機関の人員不足は、監督管理の承認と建設の見積もりスケジュールを延長する可能性がある。38.我々はNRCに新しい設計を申請しており、NRCが我々のセキュリティシステム設計および他の承認を承認する必要があり、いくつかのシステムを再設計する可能性があり、コスト増加および規制承認の遅延を招く可能性がある追加の分析および設計変更を招く可能性がある。39.我々は、Aurora製品シリーズ内の任意の動力装置がNRCまたは任意の他の規制機関の承認を得ていない場合、任意の場所で使用することができるかもしれない更新された共同運営ライセンス申請をNRCに提出しておらず、これらの設計の承認または許可およびそのような承認または許可の時間(あれば)を保証することはできない。40です既存のNRCフレームワークは,商業用途のための核燃料回収施設の許可には適用されておらず,NRCが提案した核燃料回収施設が予想されるスケジュールや我々の発展をまったく支持していない保証もない。41私たちの燃料製造施設はアメリカによって厳格に規制されるだろう。S。政府はNRCとアメリカを含むかもしれない。S。エネルギー省はこのような施設の承認や許可を保障しない。42オーロラ発電所の設計はどの国でも承認されておらず,発電所を配備する前に国ごとに承認されなければならない。承認が延期されたり拒否されたりする可能性があり、または私たちの設計を修正する必要があるかもしれません。これは、私たちの業務の見通し、財務状況、運営結果、およびキャッシュフローに大きな悪影響を及ぼす可能性があります。43.私たちの業務は有毒、危険、および/または放射性材料の使用、輸送および処置に関連し、過失や不注意を考慮しない責任を招く可能性がある。44.多くの先進的な核分裂炉と同様に,我々の動力装置は,現在大規模化生産できない高純度低濃縮ウラン(“HALEU”)に部分的に依存することが予想される。国内供給を獲得したHALEUは、供給を確保するために、大量の政府援助、規制承認、追加の第三者開発と投資を必要とする可能性がある。もし私たちがHALEUにアクセスできない場合、あるいは私たちの訪問が遅延されると、私たちが燃料を製造し、電力および/または熱を生産する能力は不利な影響を受け、これは私たちの業務の見通し、財務状況、運営結果、およびキャッシュフローに大きな悪影響を及ぼす可能性がある。45です私たちは私たちの燃料施設運営にウランの同位体を含めて放射性物質を持って使用するために政府の許可を得なければならない。このようなライセンスを取得または維持できなかったか、またはそのようなライセンスの取得を遅延させることは、私たちの顧客の発電および/または熱供給能力に影響を与え、私たちの業務の将来性、財務状況、運営業績、およびキャッシュフローに大きな悪影響を及ぼす可能性がある。

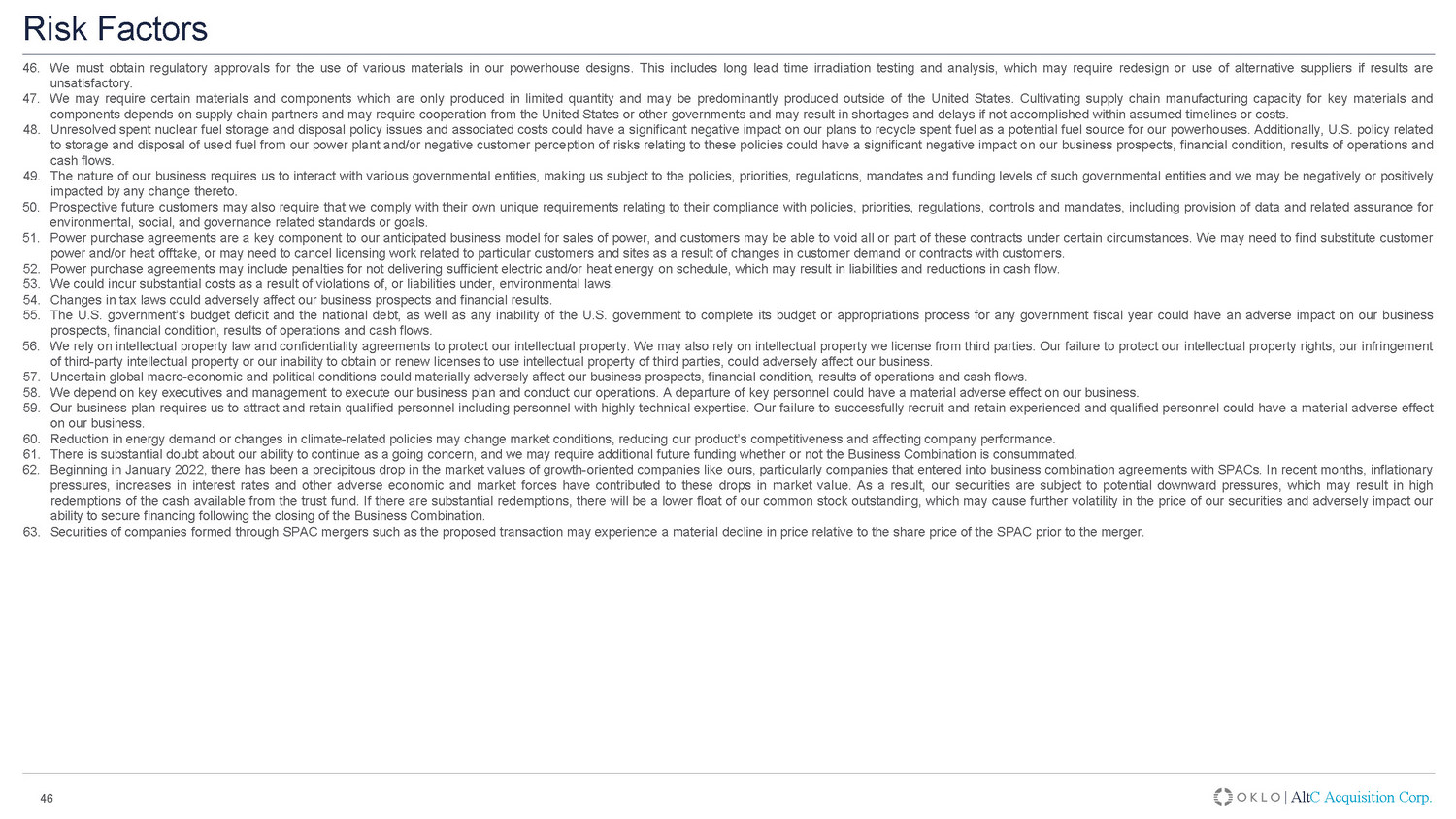

|Alt Cが企業46を買収するリスク要因46。私たちは私たちの動力室設計に様々な材料を使用するために、規制部門の許可を得なければならない。これは、結果が満足できない場合、代替供給者を再設計または使用する必要がある場合がある長時間の照射試験および分析を含む。47。私たちはいくつかの材料と部品が必要かもしれません。これらの材料と部品は数量限定で生産して、主にアメリカ以外で生産するかもしれません。キー材料や部品を育成するサプライチェーン製造能力はサプライチェーンパートナーに依存し、米国や他の政府の協力が必要となる可能性があり、想定されたスケジュールやコスト内で完成しなければ、不足や遅延を招く可能性がある。48。未解決の使用済み核燃料貯蔵·処分政策の問題や関連コストは、我々の原子力発電所の潜在的な燃料源として使用済み燃料を回収する計画に大きなマイナス影響を与える可能性がある。また、U.S。我々の発電所の使用済み燃料の貯蔵および処分に関する政策および/またはこれらの政策に関連するリスクに対する顧客の否定的な見方は、私たちの業務の将来性、財務状況、運営結果、およびキャッシュフローに大きな負の影響を及ぼす可能性がある。49.私たちの業務性質は私たちが様々な政府実体と相互作用することを要求して、これは私たちがこれらの政府実体の政策、優先事項、法規、任務、資金レベルに支配され、どんな変化も私たちにマイナスまたは積極的な影響を与える可能性がある。五十ドルです。将来の潜在的な顧客は、環境、社会、およびガバナンスに関連する基準または目標のためのデータおよび関連保証を提供することを含む、政策、優先事項、法規、制御、および許可を遵守するための彼らの独自の要件を遵守することを要求するかもしれません。51.電気購入契約は私たちが予想している電力販売業務モデルの重要な構成要素であり、場合によっては、顧客はこれらの契約を全部または部分的に無効にすることができるかもしれない。代替顧客電力および/または熱転送を探す必要がある場合があり、または顧客需要または顧客との契約が変化したため、特定の顧客およびサイトに関連する許可作業をキャンセルする必要がある場合があります。52.電気購入プロトコルは、計画通りに十分な電力および/または熱エネルギーを提供しない罰金を含む可能性があり、これは、負債およびキャッシュフローの減少をもたらす可能性がある。53。環境法違反や環境法による責任負担により巨額のコストを招く可能性がある。54。税法の変化は私たちの業務の見通しと財務業績に悪影響を及ぼす可能性がある。55アメリカです。S。政府の予算赤字と国家債務、そしてアメリカのいかなる能力も。S。もし政府がいかなる政府の財政年度の予算や支出手続きを完成できなかった場合、私たちの業務の将来性、財務状況、経営成果、キャッシュフローに悪影響を及ぼす可能性がある。56。私たちは知的財産権法と秘密保護協定に依存して私たちの知的財産権を保護する。私たちはまた第三者から許可を得た知的財産権に依存するかもしれない。私たちが私たちの知的財産権を保護できなかったこと、第三者の知的財産権を侵害したこと、または第三者知的財産権を使用する許可証を取得または更新することができなかったことは、私たちの業務に悪影響を及ぼす可能性がある。57。不確定な世界のマクロ経済と政治状況は、私たちの業務の見通し、財務状況、経営業績、キャッシュフローに重大な悪影響を及ぼす可能性がある。58私たちは主要幹部と経営陣に依存して私たちの業務計画を実行し、私たちの運営を行っています。キーパーソンの退職は私たちの業務に実質的な悪影響を及ぼすかもしれない。59.私たちの業務計画は高度な技術専門を持つ人を含む合格者を誘致して維持することを要求しています。私たちは経験のある合格者の採用と維持に成功できず、私たちの業務に実質的な悪影響を及ぼす可能性があります。六十エネルギー需要の減少や気候関連政策の変化は市場状況を変化させ、わが製品の競争力を低下させ、会社の業績に影響を与える可能性がある。61。私たちが経営を続ける企業として経営を続ける能力には大きな疑問があり、業務合併が完了するかどうかにかかわらず、将来的な追加資金が必要になるかもしれません。622022年1月から、私たちのような成長型会社の時価が急激に低下し、特にSPACと業務合併協定を締結した会社です。ここ数ヶ月、インフレ圧力、金利上昇及びその他の不利な経済と市場力は時価の低下を招いた。したがって、私たちの証券は潜在的な下振れ圧力に直面しており、これは信託基金が現金で大量に償還できる可能性がある。大量償還が発生すれば、我々が発行した普通株の流通株が減少し、証券価格のさらなる変動を招き、業務合併終了後に融資を得る能力に悪影響を及ぼす可能性がある。63.SPAC合併により形成された会社の証券は、提案された取引のように、合併前のSPAC株価に対する大幅な下落を経験する可能性がある。

|Alt C Acquisition Corp.デジタルレンダリングは説明の目的のみ

| AltC Acquisition Corp. Notes: (1) U.S. Energy Information Administration (Uranium Marketing Annual Report – 2022). (2) Department of Energy (5 Fast Fac ts about Spent Nuclear Fuel). 28 Fuel recycling Upside opportunity Oklo Large spent fuel stockpiles Spent fuel potential Oklo design advantage Unique upside opportunity Fuel supply constraints The U.S. currently relies on imports for fresh nuclear fuel ✗ In 2022, 95% (1) of uranium for U.S. nuclear plants was foreign - sourced ✗ In 2022, 33% (1) of uranium enrichment services for U.S. nuclear plants were purchased from Russia ✗ U.S. has limited HALEU production, which is the fuel for advanced reactors Limited U.S. fuel capabilities is a pressing concern for advanced reactor growth The U.S. has large and growing spent fuel stockpiles ✗ Expensive to manage ✗ U.S. reactors have generated 90,000 tons of spent fuel since 1950 (2) ✗ 2,000 tons of spent fuel generated each year (2) ✗ Spent fuel is currently stored at 70 reactor sites across 35 states (2) Spent fuel management is complex; needs will grow with new reactor deployment Spent fuel retains its energy potential and can be recycled x Fuel can be recycled and is done so in other countries, such as France x >90% of potential energy remains in spent fuel after use by current reactors (2) ✗ The U.S. does not currently recycle fuel Opportunity to address fuel supply constraints and spent fuel stockpiles with recycling Fast reactors can use either fresh or recycled fuel x EBR - II demonstrated fast reactor’s ability to use recycled fuel x Oklo plants designed with flexibility to use either fresh or recycled fuel x First Aurora powerhouse to be fueled by spent fuel recovered from EBR - II Fuel recycling could provide future margin uplift and new revenue streams Oklo is developing fuel recycling capabilities x Waste to clean energy x Selected for four projects with the Department of Energy to develop fuel recycling technologies x Initial plans to pursue a commercial - scale fuel recycling facility in the U.S. by 2030’s Oklo has the potential opportunity to lead the industry in fuel recycling

| AltC Acquisition Corp. U.S. nuclear power plants are heavily reliant on imported nuclear fuel Nuclear fuel imports | AltC Acquisition Corp. 29 Source of uranium for U.S. nuclear power plants (Uranium oxide, million pounds) (1) Notes: (1) U.S. Energy Information Administration (Nuclear explained – where our uranium comes from). (2) U.S. Energy Information Administration (Uranium Marketing Annual Report – 2022), (3) Orano (All about used fuel processing and recycling). Evolving geopolitical concerns In 2022, 95% (2) of uranium for U.S. nuclear plants was foreign - sourced In 2022, 33% (2) of foreign uranium enrichment services required by U.S. nuclear plants were purchased from Russia 0 20 40 60 80 1950 1960 1970 1980 1990 2000 2010 2020 Domestic production Purchased imports Fuel recycling could reduce U.S. imports The U.S. does not currently recycle spent fuel However, fuel can be recycled and is done so in other countries, such as France Nearly 1 in 10 light bulbs in France runs on recycled nuclear materials (3)

| Alt C Acquisition Corp. 30 Fuel recycling could provide potential future margin uplift and new revenue streams Potential opportunity to build and operate facilities that could supply recycled fuel to Aurora powerhouses as well as third - par ty customers Spent fuel recycling is a significant potential cost savings opportunity for Oklo that could reduce both initial plant capital costs as well as ongoing operating costs Vertically integrated fuel source will provide security and assurance Oklo’s recycling approach utilizes pyro - processing, which is a mature technology Additional potential revenue streams through the sale of spent fuel management services as well as the sale of byproducts and specialty isotopes to various end markets Fuel recycling solves a longstanding issue in the market and can create a sustainab le competitive advantage In January 2023, Oklo submitted a commercial - scale fuel recycling facility licensing project plan to the Nuclear Regulatory Commission How fuel recycling works Separate fuel material via electrochemistry Produce power in reactor Fabricate fuel by casting Dissolve fuel Chop up used fuel 1 2 3 4 5

| Alt C Acquisition Corp. 31 Oklo has the potential opportunity to lead the industry in fuel recycling Oklo selected by the Department of Energy for four cost - share awards to potentially commercialize recycling technologies Oklo’s recycling technology development projects Technology Commercialization Fund x Develop advanced sensors for key recycling process efficiency improvements ARPA – E Open x Utilize machine learning and digital twinning for recycling efficiency improvements and material accountability ARPA – E Onwards x Demonstrate the recycling process end - to - end and develop the technical basis for commercial - scale fuel recycling facility ARPA – E Curie x Demonstrate the conversion of used oxide fuel into metal, enabling the recycling of waste from the current fleet into advanced reactor fuel

| Alt C Acquisition Corp. 32 Deep and differentiated “hard tech,” nuclear engineering, and regulatory expertise …with a highly experienced team Founder - led organization with deep technical expertise and a highly experienced team x Oklo's team comes from Fortune 500 and global companies, as well as government and science backgrounds x Bringing together expertise and experience from several industries to deliver an advanced energy product (e.g., nuclear power, aerospace, automotive and tech) Jacob DeWitte Co - Founder and CEO Co - Founded Oklo in 2013 Caroline Cochran Co - Founder and COO Co - Founded Oklo in 2013 • 15+ years of experience in nuclear technology • PhD in nuclear engineering, MIT • Prior experiences at GE, Sandia National Labs, Urenco U.S., and the US Naval Nuclear Laboratory • 15+ years of experience in nuclear technology • MS in nuclear engineering, MIT • Prior experiences in the Office of the Secretary of Defense and U.S. Department of Energy Nuclear Energy Advisory Committee Founder - led organization… 51 employees, including 8 PhDs (16%) and 20 Masters in Engineering / Science (39%) Multiple engineers and regulatory experts have joined the Oklo team since the last licensing process Six former NRC staff members to assist with the next application filing Board of Directors includes leading hard tech investors

| AltC Acquisition Corp. 33 Strong policy support driven by critical need for nuclear energy Simplified, modern design approach applied to demonstrated technology Attractive business model targeting profitable recurring revenue Winning value proposition intended to accelerate customer adoption Site and fuel secured for first deployment Embedded potential upside from unique fuel recycling opportunity Strong founder - led team with deep technical expertise Our mission is to provide clean, reliable, affordable energy on a global scale Compelling opportunity aligned with AltC’s “hard tech” investment focus Why invest 1 2 3 4 5 6 7 Oklo’s Aurora powerhouse Digital rendering for illustrative purposes only

| Alt C Acquisition Corp. Oklo history 1 Transaction information Oklo financial information 2 3 Supporting material Digital rendering for illustrative purposes only

| Alt C Acquisition Corp. 35 Oklo is building upon a strong track record of development success 2013 Oklo founded 2014 Oklo raises seed round from 2015 Oklo raises second seed round from led by Sam Altman and a Series A round led by & 2016 Oklo begins formal pre - application process with NRC 2017 Oklo demonstrates ability to fabricate fuel prototypes using gravity casting 2018 Oklo pilots novel application with the NRC Thermal testing at Sandia National Lab 2019 DOE issues Oklo a Site Use Permit at Idaho National Laboratory and Idaho National Laboratory awards fuel material to Oklo 2020 Oklo submits novel combined license application to the NRC NRC approves Oklo’s quality assurance program description 2021 Oklo receives site specific authorization for Aurora powerhouse located at the Idaho National Laboratory 2023 Oklo submitted commercial - scale fuel recycling facility licensing project plan to the NRC Oklo announces partnership with the Southern Ohio Diversification Initiative (SODI) for two plants in Ohio 2024/2025 Oklo plans submission of updated combined license application to the NRC 2026/2027 Oklo targets first deployment and electricity production at Idaho National Laboratory Deep technical background, strong partnerships, and intensive regulatory engagement

| Alt C Acquisition Corp. Oklo history 1 Transaction information Oklo financial information 2 3 Supporting material Digital rendering for illustrative purposes only

| Alt C Acquisition Corp. 37 Illustrative unit economics: Aurora powerhouse (15 MWe) Oklo believes that expected cumulative plant cash flow equals more than 2.5x expected cumulative capital costs Notes: (1) Key assumptions based on expected NOAK (nth of a kind) plant. (2) Assumes all regulatory approvals have been obtai ned on the expected timelines. The regulatory process, including necessary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actual time necessary to obtain all the required approvals. Th e u nit economics are presented in real terms and are presented as of May 2023. The unit economics provided herein are for illust rat ive purposes only. Actual results may differ materially. (3) FOAK (first - of - a - kind) plant capital expenditure expected to be ~$34 mi llion. (4) Represents 15 MWe generating capacity at a 92% capacity factor. Aurora powerhouse (15 MWe) (2) 0 50 100 150 Year 2 Year 4 Year 6 Year 8 Year 10 Illustrative Annual Deployments (Units) Low High • 40 - year plant design life • Plant capital expenditures: ‒ Initial plant construction cost of approximately $24.0 million (excluding initial fuel load) (3) • Fuel capital expenditures: ‒ Initial fuel load of 4,750 kg ‒ Refueling load of 2,375 kg every 10 years over the 40 - year plant design life ‒ Does not assume Oklo recycles fuel for internal supply. Assumes all fuel is newly fabricated HALEU purchased from a third - party supplier at a cost of $7,000 / kg • Revenue from annual power sales : recurring revenue of approximately $13.0 million assuming annual generation of approximately 121,000 MWh (4) and average real power price of $105 / MWh • Operating costs: ‒ Annual fixed expense of $2.4 million ‒ Annual variable expense of $5.00 / MWh T+0 T+1 T+2 T+3 T+4 T+5 T+10 40-Yr Life of Plant ($ in Millions) Capital Expenditures ($57) ($17) ($107) Construction of Plant ($24) ($24) Fuel Capex ($33) ($33) Refueling Capex ($17) ($50) Revenue $13 $13 $13 $13 $13 $13 $508 Revenue from Power Sales $13 $13 $13 $13 $13 $13 $508 Expenses ($3) ($3) ($3) ($3) ($3) ($3) ($120) Fixed Plant ($2) ($2) ($2) ($2) ($2) ($2) ($96) Variable Plant ($1) ($1) ($1) ($1) ($1) ($1) ($24) Annual Plant Cash Flow ($57) $10 $10 $10 $10 $10 ($7) $281 Cash Margin NA 76.4% 76.4% 76.4% 76.4% 76.4% (54.4%) 55.4% Key Assumptions (1)(2) Aurora 15 MWe Illustrative Unit Economics (1)(2)

| Alt C Acquisition Corp. 38 Illustrative unit economics: Aurora powerhouse (50 MWe) Oklo believes that expected cumulative plant cash flow equals more than 5.0x expected cumulative capital costs Notes: (1) Key assumptions based on expected NOAK (nth of a kind) plant. (2) Assumes all regulatory approvals have been obtai ned on the expected timelines. The regulatory process, including necessary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actual time necessary to obtain all the required approvals. Th e u nit economics are presented in real terms and are presented as of May 2023. The unit economics provided herein are for illust rat ive purposes only. Actual results may differ materially. (3) FOAK (first - of - a - kind) plant capital expenditure expected to be ~$86 mi llion. (4) Represents 50 MWe generating capacity at a 92% capacity factor. • 40 - year plant design life • Plant capital expenditures: ‒ Initial plant construction cost of approximately $61.0 million (excluding initial fuel load) (3) • Fuel capital expenditures: ‒ Initial fuel load of 7,800 kg ‒ Refueling load of 3,900 kg every 10 years over the 40 - year plant design life ‒ Does not assume Oklo recycles fuel for internal supply. Assumes all fuel is newly fabricated HALEU purchased from a third - party supplier at a cost of $7,000 / kg • Revenue from annual power sales : recurring revenue of approximately $36.0 million assuming annual generation of approximately 403,000 MWh (4) and average real power price of $90 / MWh • Operating costs: ‒ Annual fixed expense of $5.6 million ‒ Annual variable expense of $4.00 / MWh Key Assumptions (1)(2) Aurora 50 MWe Illustrative Unit Economics (1)(2) T+0 T+1 T+2 T+3 T+4 T+5 T+10 40-Yr Life of Plant ($ in Millions) Capital Expenditures ($116) ($27) ($198) Construction of Plant ($61) ($61) Fuel Capex ($55) ($55) Refueling Capex ($27) ($82) Revenue $36 $36 $36 $36 $36 $36 $1,452 Revenue from Power Sales $36 $36 $36 $36 $36 $36 $1,452 Expenses ($7) ($7) ($7) ($7) ($7) ($7) ($288) Fixed Plant ($6) ($6) ($6) ($6) ($6) ($6) ($224) Variable Plant ($2) ($2) ($2) ($2) ($2) ($2) ($65) Annual Plant Cash Flow ($116) $29 $29 $29 $29 $29 $2 $966 Cash Margin NA 80.1% 80.1% 80.1% 80.1% 80.1% 4.9% 66.5% Aurora powerhouse (50 MWe) (2) 0 50 100 150 Year 2 Year 4 Year 6 Year 8 Year 10 Illustrative Annual Deployments (Units) Low High

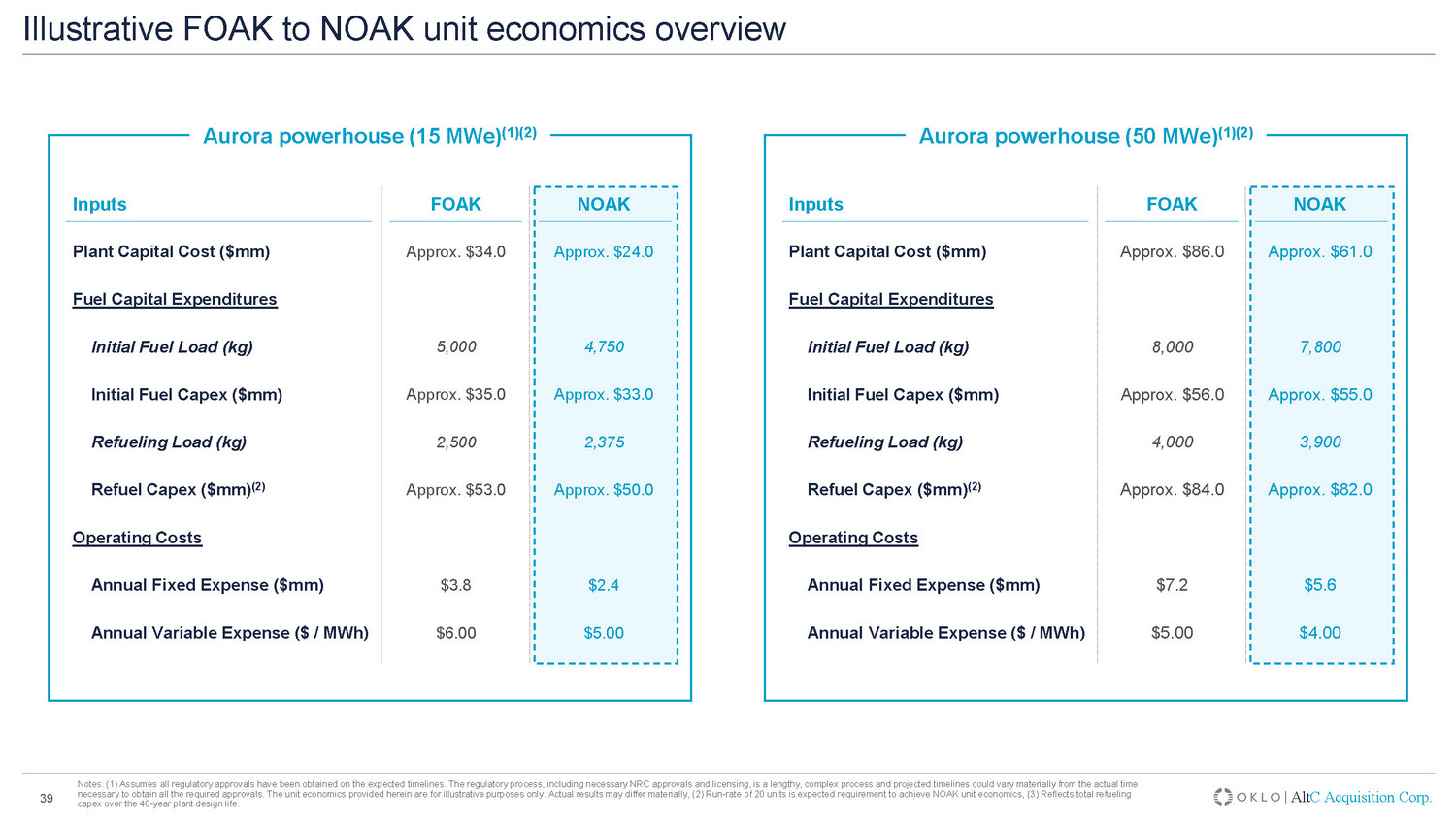

| Alt C Acquisition Corp. Inputs FOAK NOAK Plant Capital Cost ($mm) Approx. $34.0 Approx. $24.0 Fuel Capital Expenditures Initial Fuel Load (kg) 5,000 4,750 Initial Fuel Capex ($mm) Approx. $35.0 Approx. $33.0 Refueling Load (kg) 2,500 2,375 Refuel Capex ($mm) (2) Approx. $53.0 Approx. $50.0 Operating Costs Annual Fixed Expense ($mm) $3.8 $2.4 Annual Variable Expense ($ / MWh) $6.00 $5.00 Notes: (1) Assumes all regulatory approvals have been obtained on the expected timelines. The regulatory process, including n ece ssary NRC approvals and licensing, is a lengthy, complex process and projected timelines could vary materially from the actua l t ime necessary to obtain all the required approvals. The unit economics provided herein are for illustrative purposes only. Actual re sults may differ materially, (2) Run - rate of 20 units is expected requirement to achieve NOAK unit economics, (3) Reflects total refueling capex over the 40 - year plant design life. 39 Illustrative FOAK to NOAK unit economics overview Aurora powerhouse (15 MWe) (1)(2) Aurora powerhouse (50 MWe) (1)(2) Inputs FOAK NOAK Plant Capital Cost ($mm) Approx. $86.0 Approx. $61.0 Fuel Capital Expenditures Initial Fuel Load (kg) 8,000 7,800 Initial Fuel Capex ($mm) Approx. $56.0 Approx. $55.0 Refueling Load (kg) 4,000 3,900 Refuel Capex ($mm) (2) Approx. $84.0 Approx. $82.0 Operating Costs Annual Fixed Expense ($mm) $7.2 $5.6 Annual Variable Expense ($ / MWh) $5.00 $4.00

| Alt C Acquisition Corp. 40 Additional financial information Assumption Commentary General and Administrative Expenses • Before first deployment : Approximately $19.5 million in 2024 scaling to approximately $34.5 million by 2027 • Long - term assumption : Approximately 20% of power revenue Manufacturing Facility Expenditures • Reflects the required spend by Oklo to establish manufacturing and fabrication capabilities to support deployment of the Aurora powerhouse • Approximately $40 million in plant manufacturing facility capital expenditures by 2030 (1) Maintenance Expenditures • Approximately 10% maintenance capital expenditures of initial plant capital costs every 10 years Occupancy Expense • Approximately 5.0% of power revenue Working Capital • Approximately 4.0% of power revenue Notes: (1) Does not include any potential fuel fabrication or recycling investment.

| Alt C Acquisition Corp. Oklo history 1 Transaction information Oklo financial information 2 3 Supporting material Digital rendering for illustrative purposes only

| Alt C Acquisition Corp. Sources $ millions % AltC cash-in-trust 516 38% Existing Oklo shareholders 850 62% Total sources 1,366 100% Uses $ millions % Cash to balance sheet 478 35% Existing Oklo shareholders 850 62% Illutrative fees and expenses 38 3% Total uses 1,366 100% Notes: (1) AltC cash - in - trust was $515,791,749 as of June 30, 2023. For illustrative purposes only, (2) Assumes no AltC shareholders exercise their redemption rights to receive cash from the trust account at closing, (3) Proposed transaction pre - m oney equity value, subject to potential increase for permitted company financings prior to close of the business combination. Pre - money equity valu e to convert at $10 per share at close of the business combination. Excludes impact of potential earnout shares, (4) AltC cash - in - trust less illustrative fees and expenses, (5) Includes all outstanding AltC Class A shares. Includes the potential dilutive impact of 6.250 million Class B founder shares that are unvested at close and s ubject to vesting if the post - closing share price remains at or above $10 per share for 20 of 60 days. Excludes the impact of 3.125 million Class B founder shares that vest at $12.00 per share an d 3 .125 million Class B founder shares that vest ratably at $14.00 per share and $16.00 per share within 5 - years of closing. 42 Transaction values Oklo at a pre - money equity value of $850 million, which is roughly half the value of comparable clean energy go public transactions Estimated transaction sources and uses Pro forma ownership Transaction highlights (1)(2) (4) Proposed transaction overview (3) (3) Assumes $10 per share Shares (millions) % Ownership Existing Oklo shareholders 85 60% AltC shareholders 58 40% Total sources 143 100% (3) (1)(5) • Pre - money equity value of $850 million, which is roughly half the value of comparable clean energy go public transactions • Up to 15.0 million earnout shares available for existing Oklo shareholders, vesting ratably at $12.00, $14.00, and $16.00 per share within 5 - years of closing • No cash to Oklo shareholders – will roll 100% of existing shares • All proceeds raised, net of transaction expenses, will go directly to Oklo’s balance sheet and will be used to accelerate its business plan and fund the first deployment of the Aurora powerhouse • AltC sponsor will subject 100% of retained shares to performance vesting • Oklo founders and AltC sponsor shares will be subject to a staggered lock - up over 3 years following closing of the business combination

| Alt C Acquisition Corp. Notes: (1) Excluding earnout shares and adjustments for permitted financings. 43 Simple transaction structure with alignment of long - term interests between public investors, the AltC sponsors, and existing Oklo shareholders • Oklo shareholders will receive 85.0 million shares (1) in the combined company as part of the transaction; no cash proceeds to be received by Oklo shareholders • Up to 15.0 million earnout shares available upon share price appreciation of 20 – 60% within 5 - years; enables transaction value to be set at an attractive level by providing upside to Oklo shareholders if the share price rises • AltC sponsor will un - vest 100% of founder shares at close of the business combination and will not earn back its shares unless the share price appreciates • Oklo founders and AltC sponsor shares will be subject to a staggered lock - up over 3 years following close of the business combination • Committed to operate with strong public company governance • Board with relevant expertise to be assembled; one director nominated by AltC and another director mutually designated by AltC and Oklo • Oklo will have a single class of shares following the transaction with equal voting rights for all shareholders • Simplicity is core to Oklo’s ethos – straightforward corporate structure and no special agreements that only benefit existing Oklo shareholders x All net transaction proceeds invested in Oklo, no cash to Oklo shareholders x Oklo shareholders to roll 100% of existing equity x AltC’s sponsor to subject 100% of retained shares to performance vesting x Long duration lock - up for Oklo founders and AltC’s sponsor x Board of director talent to be assembled to provide support from proven business leaders and value creators in the public markets x Single class of shares with equal voting rights for all shareholders x No complex corporate structure or special shareholder tax agreements Oklo shareholders to roll 100% of existing equity into the combined company Oklo shareholders eligible for performance - based earnout shares AltC sponsor will subject 100% of retained shares to performance vesting Long duration lock - up for Oklo founders and AltC sponsor Leading governance and board of director talent Single class of shares No complex corporate structure or special shareholder tax agreements Transaction structure priorities Public investor benefits Proposed transaction structure

| Alt C Acquisition Corp. 44 Risk Factors 1. Our business plan requires substantial investment . If there are significant redemptions in connection with the proposed Business Combination, we may need to make significant adjustments to our business plan or seek additional capital . Depending on our available capital resources, we may need to delay or discontinue expected near - term expenditures, which could materially impact our business prospects, financial condition, results of operations and cash flows by limiting our ability to pursue some of our other strategic objectives and/or reducing the resources available to further develop our design, sales and manufacturing efforts . 2. In order to fulfill our business plan, we will require additional funding in addition to any funding resulting from the proposed Business Combination . Such funding may be dilutive to our investors and no assurances can be provided as to the availability or terms of any such funding . Any such funding and the associated terms will be highly dependent upon market conditions and the progress of our business at the time we seek such funding . 3. Our projected corporate expenditures and our ability to achieve profitability are subject to numerous risks and uncertainties, including uncertainties related to the impact of inflation, evolving regulatory requirements, raw material and nuclear fuel availability, global conflicts, global supply chain challenges and component manufacturing and testing uncertainties, local and domestic energy policies, international energy policies, international trade policies, government contracting and procurement rules, among other factors . Accordingly, it is possible that our overall expenditures could be higher than the levels we currently estimate, and any increases could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 4. We may experience a disproportionately larger impact from inflation and rising costs . Although the impact of material cost, labor, or other inflationary or economically driven factors will impact the entire nuclear and energy transition industry (including renewable sources of electricity, like solar and wind), the relative impact will not be the same across the industry, and the particular effects within the industry will depend on a number of factors, including material use, technology, design, structure of supply agreements, project management and other factors, which could result in significant changes to the competitiveness of our technology and our ability to sell our powerhouses, which could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 5. We are an early - stage company with a history of financial losses (e . g . , negative cash flows), and we expect to incur significant expenses and continuing financial losses at least until our powerhouses become commercially viable, which may never occur . 6. If we fail to manage our growth effectively, we may be unable to execute our business plan which could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 7. We have not yet sold any powerhouses or entered into any binding contract with any customer to deliver electricity or heat and there is no guarantee that we will be able to do so in the future . This limited commercial operating history makes it difficult to evaluate our prospects and the risks and challenges we may encounter . 8. Our business plan includes the use of investment tax credits, production tax credits or other forms of government funding to finance the commercial development of our powerhouses, and there is no guarantee that our projects will qualify for these credits or that government funding will be available in the future . 9. The amount of time and funding needed to bring our powerhouses to market may greatly exceed our projections . 10. Our construction and delivery timeline estimates for our powerhouses may increase due to a number of factors, including the degree of pre - fabrication, standardization, on - site construction, long - lead procurement, contractor performance, plant qualification testing and other site - specific considerations . 11. We do not currently employ any risk sharing structures to mitigate the risks associated with the delivery and performance of our powerhouses . Any delays or setbacks we may experience for our first commercial delivery or failure to obtain final investment decisions for future orders could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows and could harm our reputation . 12. Any failure to effectively update the design, construction, and operations of our powerhouses to ensure cost competitiveness could reduce the marketability of our powerhouses and adversely impact our expected deployment schedules . 13. Our business plan and our ability to achieve profitability relies on the concurrent development of two configurations of our powerhouses ( 15 MWe and 50 MWe), and makes certain assumptions with respect to learnings, efficiencies and regulatory approvals as a result of this concurrent development approach which may not be accurate or correct . Any adverse change to these assumptions may have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 14. Our business plan and our ability to achieve profitability may also rely on the development of other configurations of our powerhouses ( 100 MWe, or other sizes), and makes certain assumptions with respect to learnings, efficiencies and regulatory approvals as a result of this new development approach which may not be accurate or correct . Any adverse change to these assumptions may have a material adverse effect on our business prospects, financial condition and results of operation and cash flows . 15. Our cost estimates are highly sensitive to broader economic factors, and our ability to control or manage our costs may be limited . Capital and operating costs for the deployment of a first - of - a - kind powerhouse like the Aurora are difficult to project, inherently variable and are subject to significant change based on a variety of factors including site specific factors, customer off - take requirements, regulatory oversight, operating agreements, supply chain availability, supply chain availability effects on reactor and power plant performance, inflation and other factors . 16. Opportunities for cost reductions with subsequent deployments are similarly uncertain . To the extent cost reductions are not achieved within the expected timeframe or magnitude, the Aurora may not be cost competitive with alternative technologies, which may have a material adverse effect on our business prospects, financial condition, results of operations and cash flows and could harm our reputation . 17. The amount of time and funding needed to bring our nuclear fuel to market at scale may significantly exceed our expectations . Any material change to our assumptions or expectations with respect to our timeline and funding needs, or any material overruns or other unexpected increase in costs or delays, which may have a material adverse effect on our business prospects, financial condition, results of operations and cash flows and could harm our reputation . 18. The market for advanced fission power is not yet established and may not achieve the growth potential we expect or may grow more slowly than expected and may be superseded or rendered obsolete by new technology or the novel application of existing technology . 19. The market for recycled nuclear fuel in the United States is not yet established and may not achieve the growth potential we expect or may grow more slowly than expected as a result our investment in recycling may be misplaced . 20. We and our customers operate in a politically sensitive environment, and the public perception of fission energy can affect our customers and us . 21. Our technology requires regulatory approvals, and policies around the handling and use of radioactive materials that affect regulatory requirements, processes and the ability to regulate these technologies may change and make regulatory approvals not attainable, adversely affecting our business .

| Alt C Acquisition Corp. 45 Risk Factors 22. Our business plan involves contracting with the government and government - affiliated entities, and any changes or delays to contracting procedures, rules and regulations could lengthen our timeframes to construct and operate our plants, which could materially and adversely affect our business . 23. Incidents involving nuclear energy facilities in the United States or globally, including accidents, terrorist acts or other high profile events involving radioactive materials, could materially and adversely affect the public perception of the safety of nuclear energy, our customers and the markets in which we operate, and such adverse effects could potentially decrease demand for nuclear energy, increase regulatory requirements and costs or result in liability or claims that could materially and adversely affect our business . 24. While we believe our cost estimates are reasonable, they may increase significantly through design maturity, when accounting for supply chain availability, fabrication costs, as we progress through the regulatory process, or as a result of other factors, including unexpected cost increases that particularly effect our powerhouses . 25. Building a new fuel fabrication facility is challenging as a result of many factors, including regulatory and construction complexity, and may take longer or cost more than we expect . 26. We have not sought nor received third - party cost estimates at this time but expect to do so in the future . Such third - party cost estimates may be significantly higher than our current estimates, which may affect the marketability of our powerhouses and our expectations with respect to our business plan and future profitability 27. There is limited precedent for independent developer construction and operation, or use of power purchase agreements, other behind - the - meter or off - grid business models relating to deployment of fission power plants . 28. There is limited operating experience for metal - fueled fast reactors of this type, configuration and scale, compared to that of the existing fleet of large light water reactors . This may result in greater than expected construction cost, deployment timelines, maintenance requirements, differing power output and greater operating expense . 29. Operating a nuclear power plant in a remote environment or in an industrial application has additional risks and costs compared to conventional electric power and heat applications . Such deployments may require additional costs including costs associated with the licensing process, configuration control of the plant, minimum operating staff, training, security infrastructure, radiation protection, government reporting, and nuclear insurance, all of which may be cost prohibitive or reduce the competitiveness of technology . 30. Competition from existing or new competitors or technologies could cause us to experience downward pressure on prices, fewer customer orders, reduced margins, the inability to take advantage of new business opportunities, and the loss of market share . 31. Successful commercialization of new, or further enhancements to existing, alternative carbon - free energy generation technologies, such as adding carbon capture and sequestration/storage mechanisms to fossil fuel power plants, wind, solar, or fusion, may prove to be more cost effective or appealing to the global energy markets and therefore may adversely affect the market demand for, and our ability to, successfully commercialize our targeted powerhouses . 32. The cost of electricity and heat generated from our powerhouses may not be cost competitive with electricity and/or heat generated from other sources, and there is no guarantee that we will be able to charge a premium relative to other energy sources, which could materially and adversely affect our business prospects, financial condition, results of operations and cash flows . 33. Changes in the availability and cost of oil, natural gas and other forms of energy are subject to volatile market conditions that could adversely affect our business prospects, financial condition, results of operations and cash flows . 34. We rely on a limited number of suppliers for certain materials and supplied components, some of which are highly specialized and are being designed for first - of - a - kind or sole use in our power plants . We and our third party vendors may not be able to obtain sufficient materials or supplied components to meet our manufacturing and operating needs or obtain such materials on favorable terms . 35. The operations of our planned fuel facility in Idaho, planned power plants in Idaho and Ohio, and any future facilities, will be highly regulated by the U . S . federal and state - level governmental authorities, including the U . S . Nuclear Regulatory Commission (“NRC”) and regulatory bodies in other jurisdictions in which we may establish operations . Our operations and business plans could be significantly impacted by changes in government policies and priorities . 36. Our business is subject to stringent U . S . export control laws and regulations . Unfavorable changes in these laws and regulations or U . S . government licensing policies, our failure to secure timely U . S . government authorizations under these laws and regulations, or our failure to comply with these laws and regulations could have a material adverse effect on our ability to expand globally and thereby affect our business prospects, financial condition, results of operations and cash flows . 37. Changes in governmental agency budgets as well as staffing shortages at national laboratories and other governmental agencies may lengthen our estimated timelines for regulatory approval and construction . 38. We are pursuing an application for a novel design with the NRC, which will require NRC approval of our safety system design among other approvals and may result in additional analysis and design changes, including potential redesigns of certain systems, and could lead to increased costs and delays with respect to regulatory approvals . 39. We have not yet submitted our updated combined operating license application to the NRC and no powerhouse in the Aurora product family has yet been approved or licensed for use at any site by the NRC or any other regulatory agency, and approval or licensing of these designs and the timing of such approval or licensing, if any, is not guaranteed . 40. The existing NRC framework has not been applied to license a nuclear fuel recycling facility for commercial use, and there is no guarantee that the NRC will support the development of our proposed nuclear fuel recycling facility on the timeline we anticipate or at all . 41. Our fuel fabrication facilities will be highly regulated by the U . S . government, potentially including both the NRC and the U . S . Department of Energy and approval or licensing of these facilities is not guaranteed . 42. The design of the Aurora powerhouses has not been approved in any country, and approvals must be obtained on a country - by - country basis before the powerhouses can be deployed . Approvals may be delayed or denied or may require modification to our design, which could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 43. Our operations involve the use, transportation and disposal of toxic, hazardous and/or radioactive materials and could result in liability without regard to fault or negligence . 44. Our powerhouses, like many advanced fission reactors, are expected to rely, in part, on high assay low enriched uranium (“ HALEU ”) which is not currently available at scale . Access to a domestic supply of HALEU may require significant government assistance, regulatory approval, and additional third - party development and investment to ensure availability . If we are unable to access HALEU , or our access is delayed, our ability to manufacture fuel and to produce electricity and/or heat will be adversely affected, which could have a material adverse effect on our business prospects, financial condition, results of operations and cash flows . 45. We must obtain governmental licenses to possess and use radioactive materials, including isotopes of uranium, in our fuel facility operations . Failure to obtain or maintain, or delays in obtaining, such licenses could impact our ability to generate electricity and/or heat for our customers and have a material adverse effect on our business prospects, financial condition, results of operations and cash flows .

| Alt C Acquisition Corp. 46 Risk Factors 46. We must obtain regulatory approvals for the use of various materials in our powerhouse designs . This includes long lead time irradiation testing and analysis, which may require redesign or use of alternative suppliers if results are unsatisfactory . 47. We may require certain materials and components which are only produced in limited quantity and may be predominantly produced outside of the United States . Cultivating supply chain manufacturing capacity for key materials and components depends on supply chain partners and may require cooperation from the United States or other governments and may result in shortages and delays if not accomplished within assumed timelines or costs . 48. Unresolved spent nuclear fuel storage and disposal policy issues and associated costs could have a significant negative impact on our plans to recycle spent fuel as a potential fuel source for our powerhouses . Additionally, U . S . policy related to storage and disposal of used fuel from our power plant and/or negative customer perception of risks relating to these policies could have a significant negative impact on our business prospects, financial condition, results of operations and cash flows . 49. The nature of our business requires us to interact with various governmental entities, making us subject to the policies, priorities, regulations, mandates and funding levels of such governmental entities and we may be negatively or positively impacted by any change thereto . 50. Prospective future customers may also require that we comply with their own unique requirements relating to their compliance with policies, priorities, regulations, controls and mandates, including provision of data and related assurance for environmental, social, and governance related standards or goals . 51. Power purchase agreements are a key component to our anticipated business model for sales of power, and customers may be able to void all or part of these contracts under certain circumstances . We may need to find substitute customer power and/or heat offtake, or may need to cancel licensing work related to particular customers and sites as a result of changes in customer demand or contracts with customers . 52. Power purchase agreements may include penalties for not delivering sufficient electric and/or heat energy on schedule, which may result in liabilities and reductions in cash flow . 53. We could incur substantial costs as a result of violations of, or liabilities under, environmental laws . 54. Changes in tax laws could adversely affect our business prospects and financial results . 55. The U . S . government’s budget deficit and the national debt, as well as any inability of the U . S . government to complete its budget or appropriations process for any government fiscal year could have an adverse impact on our business prospects, financial condition, results of operations and cash flows . 56. We rely on intellectual property law and confidentiality agreements to protect our intellectual property . We may also rely on intellectual property we license from third parties . Our failure to protect our intellectual property rights, our infringement of third - party intellectual property or our inability to obtain or renew licenses to use intellectual property of third parties, could adversely affect our business . 57. Uncertain global macro - economic and political conditions could materially adversely affect our business prospects, financial condition, results of operations and cash flows . 58. We depend on key executives and management to execute our business plan and conduct our operations . A departure of key personnel could have a material adverse effect on our business . 59. Our business plan requires us to attract and retain qualified personnel including personnel with highly technical expertise . Our failure to successfully recruit and retain experienced and qualified personnel could have a material adverse effect on our business . 60. Reduction in energy demand or changes in climate - related policies may change market conditions, reducing our product’s competitiveness and affecting company performance . 61. There is substantial doubt about our ability to continue as a going concern, and we may require additional future funding whether or not the Business Combination is consummated . 62. Beginning in January 2022 , there has been a precipitous drop in the market values of growth - oriented companies like ours, particularly companies that entered into business combination agreements with SPACs . In recent months, inflationary pressures, increases in interest rates and other adverse economic and market forces have contributed to these drops in market value . As a result, our securities are subject to potential downward pressures, which may result in high redemptions of the cash available from the trust fund . If there are substantial redemptions, there will be a lower float of our common stock outstanding, which may cause further volatility in the price of our securities and adversely impact our ability to secure financing following the closing of the Business Combination . 63. Securities of companies formed through SPAC mergers such as the proposed transaction may experience a material decline in price relative to the share price of the SPAC prior to the merger .

| Alt C Acquisition Corp. Digital rendering for illustrative purposes only