截至2024年6月30日的债务到期情况主要银行债务协议其他 银行债务截至2024年6月30日的债务总额:75.53亿美元固定收益租赁平均债务寿命:4.6年 1,502 1,389 1,254 1,254 1,2522 908 826 484 169 2024 2026 2027 2028 2029 2030 203100万美元债务到期日概况不包括Cemex Holdings的债务菲律宾公司(CHP)及其子公司欠Cemex集团以外的第三方的债务,由于我们同意剥离在 {的业务,这笔债务被重新归类为持有的21笔待售负债br} 菲律宾,根据国际财务报告准则

年初至今的合并销量和价格与24年第二季度对比23年第二季度与24年第一季度年初至今 23年第二季度成交量 (1%) (0%) 12% 国内灰色价格 (美元) 5% 2% (0%) 水泥价格 (l-t-l) 3% 3% 1% 成交量 (10%) (9%) 10% 预拌价格 (美元) 6% 4% (1%) 价格 (l-t-l) 5% 0% 成交量 (3%) (3%) 12% 总价格 (美元) 4% 3% (2%) 价格 (l-t-l) 3% 3% (1%) 价格 (l-t-l) 在恒定外汇汇率下按交易量加权平均值计算的价格 (l-t-l) 22

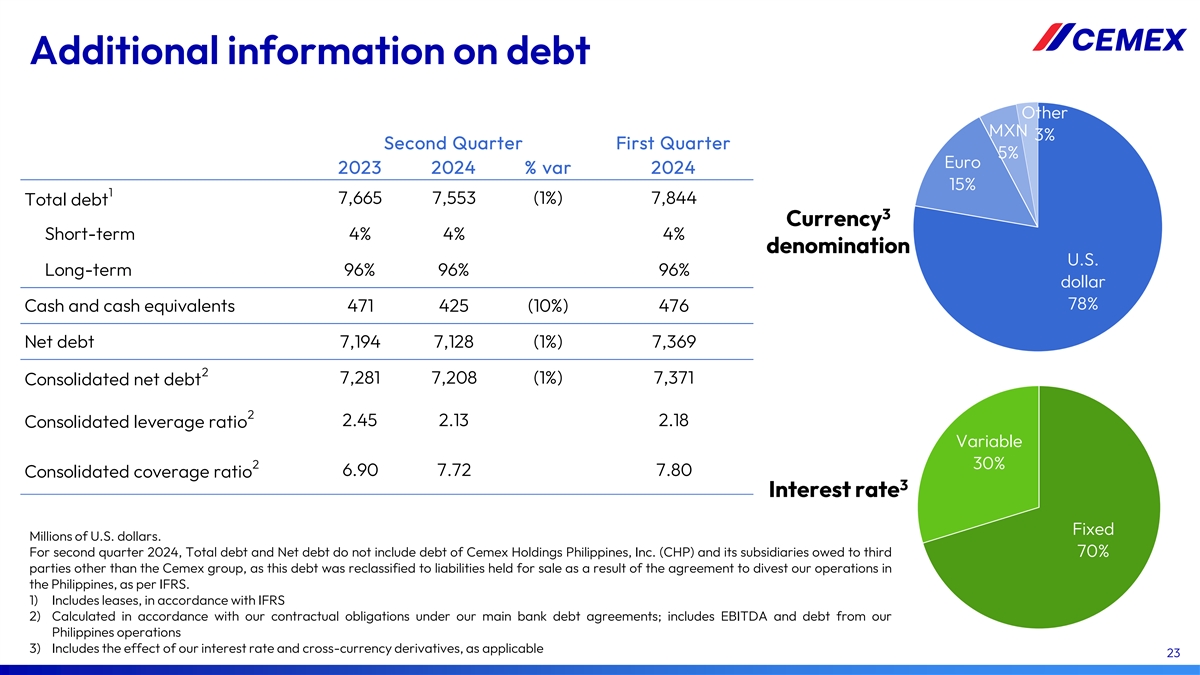

其他债务信息其他第一季度墨西哥比索 3% 5% 欧元 2024% var 2024 15% 1 7,665 7,553 (1%) 7,844 债务总额 3 货币短期 4% 4% 4% 面额美国长期 96% 96% 96% 96% 美元 78% 现金及现金等价物 471 425 (10%) 476 净负债 7,194 7,128 (1%) 7,369 2 7,281 7,208 (1%) 7,371 合并净负债 2 2.45 2.13 2.18 合并杠杆率变量 2 30% 6.90 7.72 7.80 合并承保率 3 固定利率百万美元。2024年第二季度,总负债和净负债不包括菲律宾Cemex Holdings, Inc.(CHP)及其子公司欠Cemex集团以外的第三方70%的债务 ,因为根据国际财务报告准则,该债务被重新归类为出售的负债, 。1) 包括租赁,根据国际财务报告准则2计算我们在主要银行债务协议下的合同义务;包括息税折旧摊销前利润和我们在菲律宾业务的债务 3) 包括我们 的影响利率和跨货币衍生品(视情况而定)23

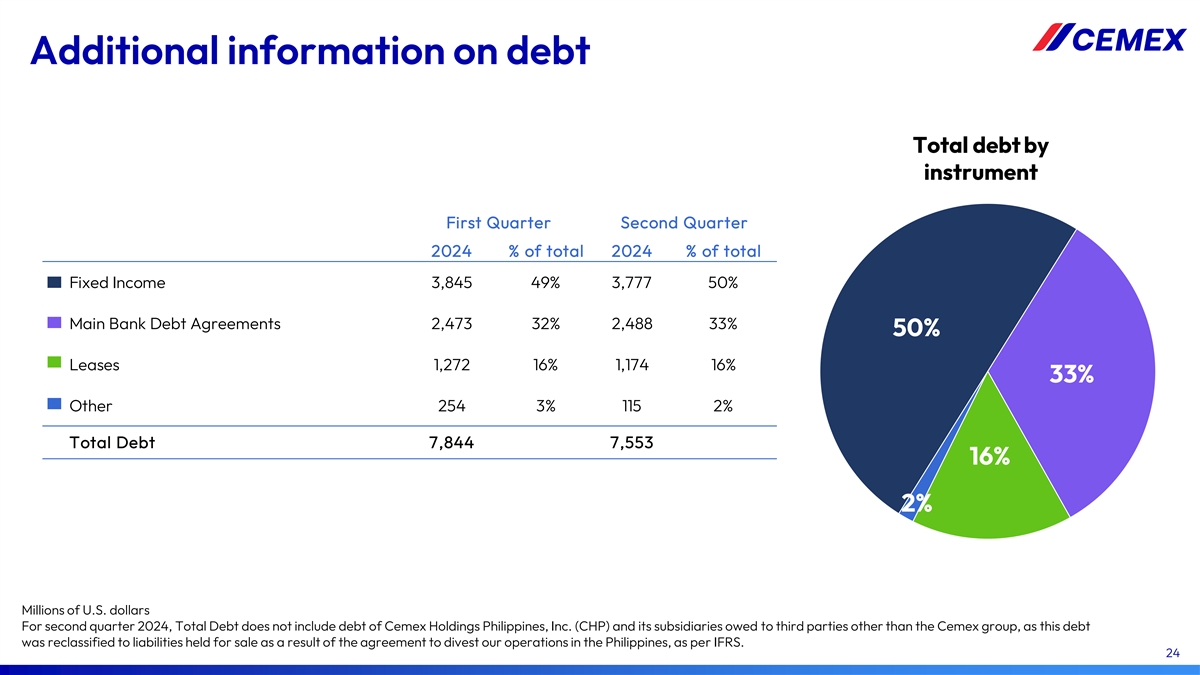

债务其他信息按工具划分的债务总额2024年第一季度 第二季度占总额的百分比 2024 年第二季度占总固定收益的百分比 3,845 49% 3,777 50% 主银行债务协议 2,473 32% 2% 2% 租赁1,272 16% 1,174 16% 33% 其他 254 3% 115 2% 总债务 7,844 7,553 16% 2% 百万美元2024年第二季度包括菲律宾Cemex Holdings, Inc.(CHP)及其子公司欠Cemex集团以外的第三方的债务,因为该债务被重新归类为根据该协议持有的待售负债 根据国际财务报告准则,剥离我们在菲律宾的业务。24

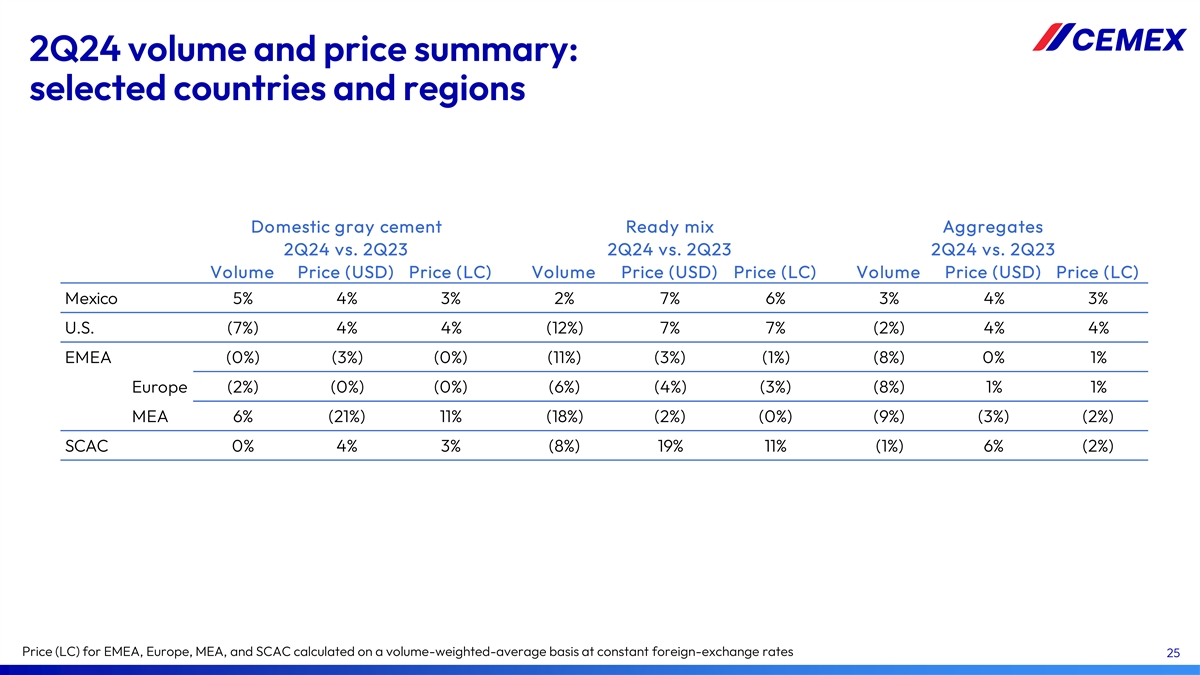

24 年第二季度成交量和价格摘要:选定的国家和地区国内 灰色水泥预拌混料总量 24 年第 2 季度与 23 年第 2 季度与 23 年第二季度成交量(美元)价格(美元)成交量(美元)价格(LC)成交量(美元)价格(LC)墨西哥 5% 3% 2% 7% 3% 3% 4% 3% 3% 美国(7%)4%(12%)7%(2%)4% 4% 欧洲 (2%) (0%) (3%) (0%) (11%) (3%) (8%) 0% 1% 欧洲 (2%) (0%) (6%) (4%) (3%) (8%) 1% MEA 6% (21%) 11% (18%) (2%) (0%) (3%) (2%) SCAC 0% 4% (8%) 19% (8%) 19% (11%) 1%) 按照 交易量计算的欧洲、中东和非洲、欧洲、中东和非洲地区和 SCAC 的 6% (2%) 价格 (LC)-按固定外汇汇率计算的加权平均值 25

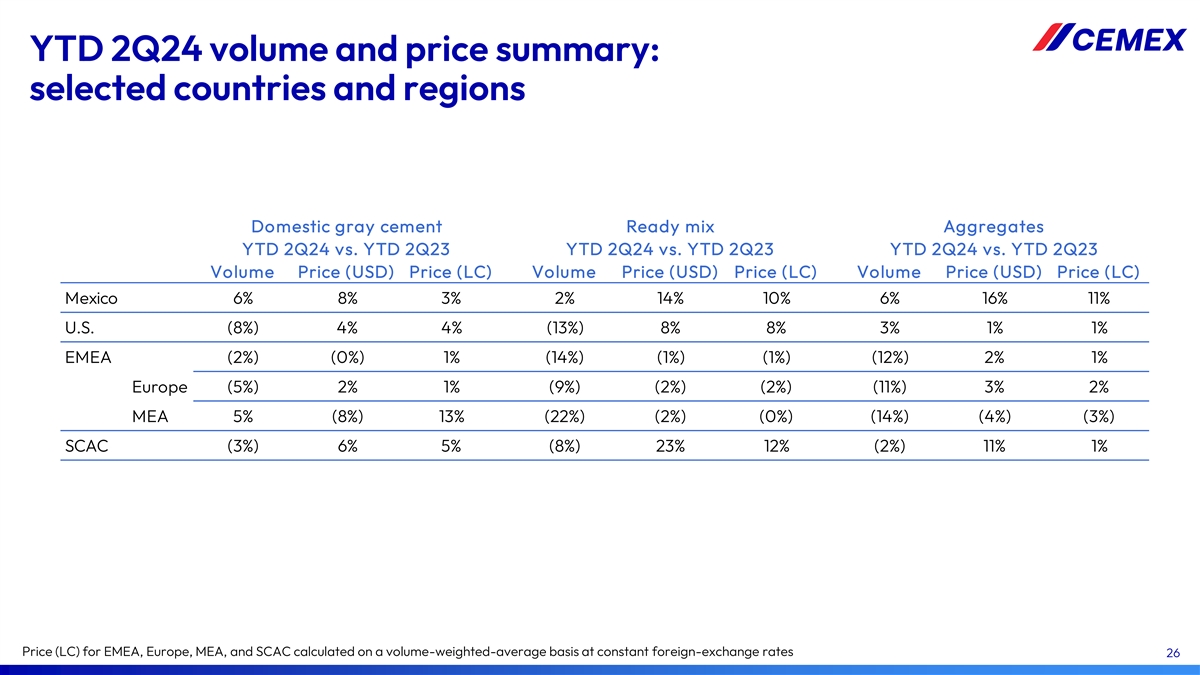

年初至今 24 年第 2 季度销量和价格摘要:部分国家和地区国内 灰色水泥预拌骨料年初至今 24 年第 2 季度与 2023 年第二季度年初至今 2 季度年初至今 2 季度年初至今 2 季度成交量(美元)价格(美元)价格(LC)成交量(美元)价格(LC)墨西哥 6% 8% 2% 14% 10% 6% 16% 11% 美国(8%)4% 4% (13%) 8% 3% 1% 1% 欧洲、中东和非洲 (2%) (0%) 1% (14%) (1%) (12%) 2% 1% 欧洲 (5%) 2% 1% (9%) (2%) (2%) (2%) 2% MEA 5% (8%) 13% (22%) (2%) (14%) (4%) (3%) SCAC (3%) 6% (8%) 5% (8%)) 23% 12% (2%) 11% 1% 价格 (LC) 适用于 EMEA、欧洲、中东和非洲地区和 SCAC 以恒定外汇汇率的交易量加权平均值计算 26

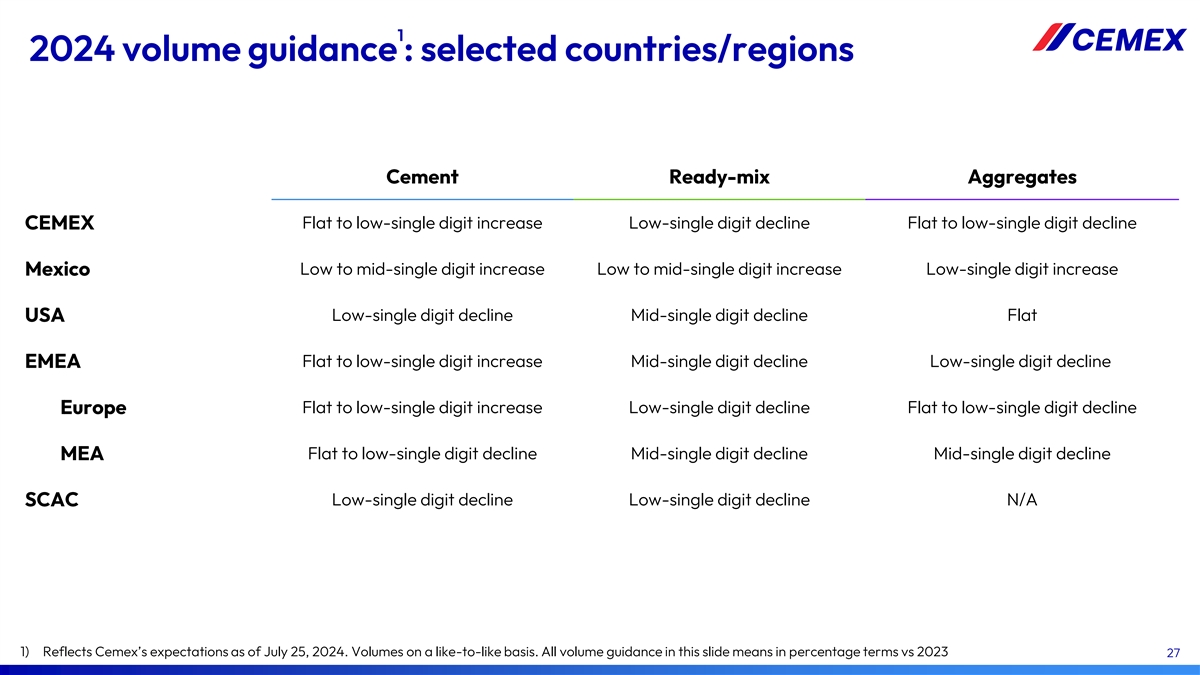

1 2024年成交量指引:部分国家/地区水泥预混料 总量持平至低个位数增幅低个位数下降幅度持平至较低个位数降幅 CEMEX 低至中个位数增长低个位数增幅墨西哥低个位数下降中位数 降幅持平至低个位数增幅美国持平至低个位数增幅低个位数下降幅度持平至低个位数下降 MEA 持平至较低的个位数跌幅 中等个位数下降幅度中位数下降SCAC 低个位数下降低个位数下降N/A 1) 反映了Cemex截至2024年7月25日的预期。成交量以点赞为基础。本幻灯片中的所有交易量指导均以 百分比表示,与 2023 年相比 27

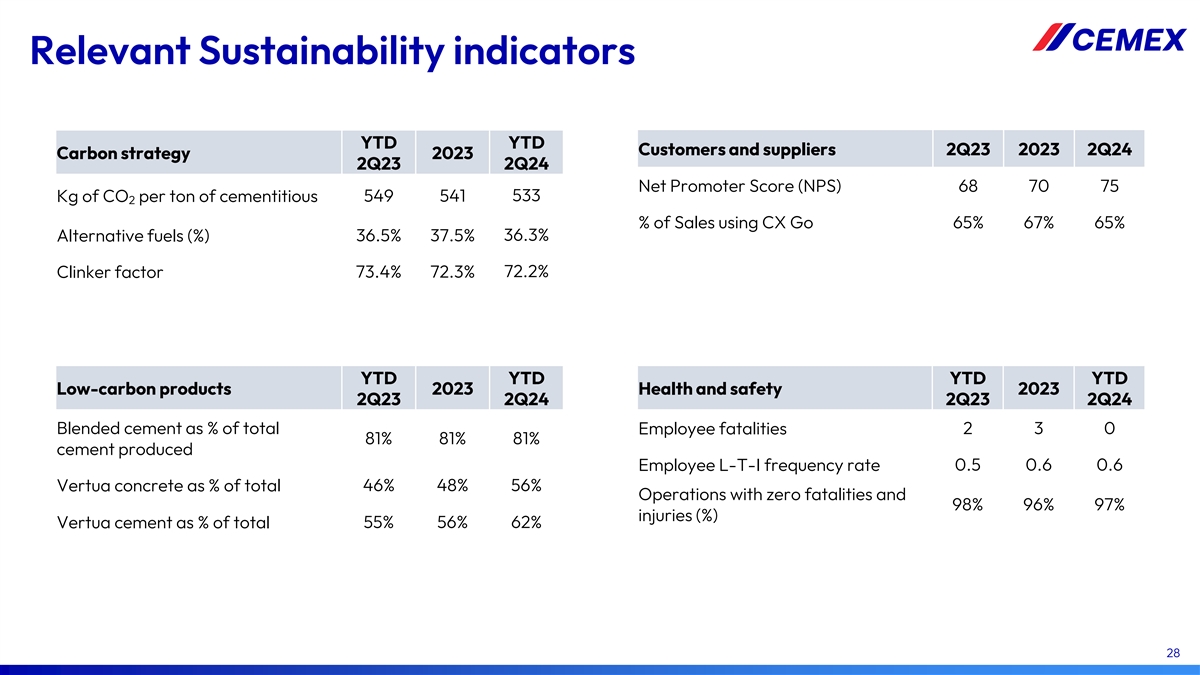

年初至今相关可持续发展指标客户和供应商 2023 年第二季度 24 年第二季度碳战略 2023 年第二季度第二季度净推荐值(NPS)68 70 75 533 千克二氧化碳 549 541 使用 CX Go 占销售额的 2% 65% 67% 65% 替代燃料(%)36.5% 36.3% 年初至今 73.4% 72.3% 72.3% 72.2% 熟料系数 低碳产品 2023 年健康与安全 2023 年第二季度第二季度 23 年第二季度混合水泥占总数 2 3 0 员工死亡人数的百分比 81% 81% 81% 81% 81% 水泥生产员工 L-t-i 频率 0.5 0.6 0.6 Vertua 混凝土占总数 46% 48% 56% 运营 死亡人数为零 ,98% 96% 97% 受伤 (%) Vertua 水泥占总数的百分比 55% 56% 62% 28

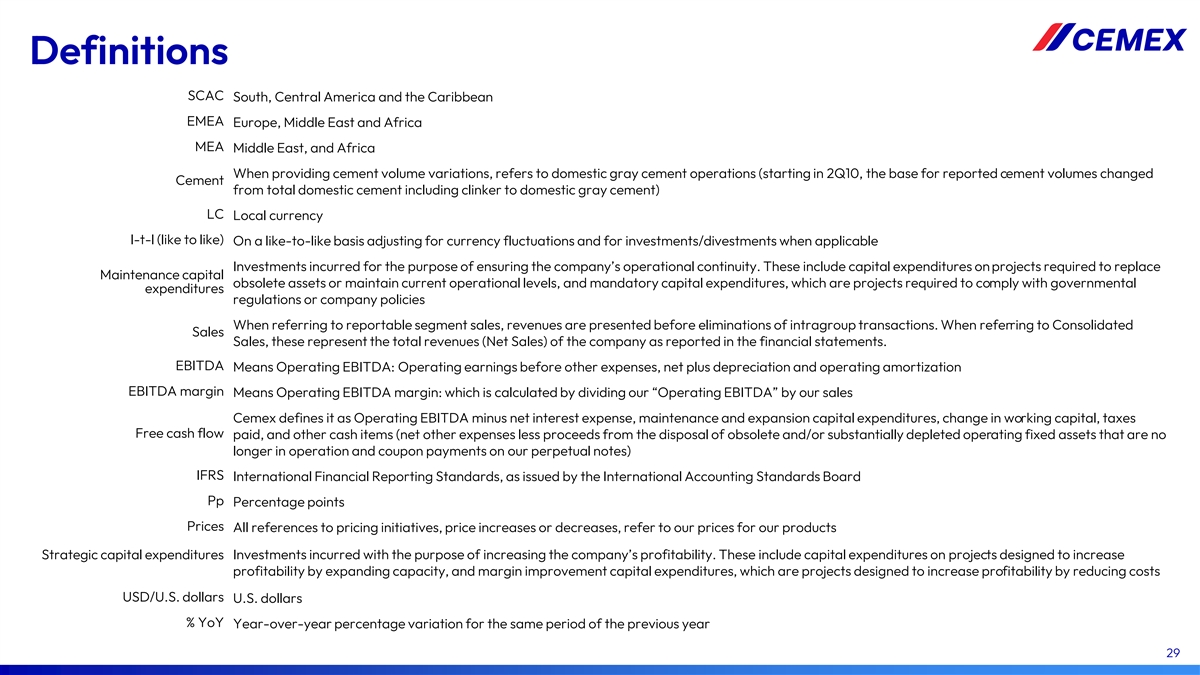

定义 SCAC 南部、中美洲和加勒比地区 EMEA 欧洲、 中东和非洲 MEA 中东和非洲在提供水泥产量变化时,是指国内灰水泥业务(从 2010 年第二季度开始,报告的水泥产量的基准将水泥从包括熟料 的国内水泥总量改为国产灰水泥)LC 当地货币 l-t-l(点赞)根据货币波动和投资情况进行调整/按类比调整在适用的情况下撤资为确保公司的 而产生的投资运营连续性。其中包括更换维护资本、过时资产或维持当前运营水平所需的项目的资本支出,以及强制性资本支出,这些项目必须遵守 政府支出法规或公司政策。当涉及应报告的细分市场销售时,收入在取消集团内部交易之前列报。当提及合并销售额时,它们代表财务报表中报告的公司总收入(净销售额)。息税折旧摊销前利润是指营业息税折旧摊销前利润:扣除其他费用、净额加上折旧和营业摊销前利润率是指营业息税折旧摊销前利润率: 通过将我们的 “营业息税折旧摊销前利润” 除以销售额计算得出 Cemex 将其定义为运营息税折旧摊销前利润减去净利息支出、营运资金变动、已付税款和 其他现金项目(净其他费用减去收益)来自处置已不在的过时和/或已严重耗尽的运营固定资产永续票据的运营和息票支付)国际财务报告准则国际财务报告准则 标准,由国际会计准则委员会发布的 Pp 百分点价格。所有提及定价举措、价格上涨或下跌的内容,均指我们的产品价格战略资本支出投资 以提高公司盈利能力为目的而发生的投资 。其中包括旨在通过扩大产能提高盈利能力的项目的资本支出,以及利润率改善资本支出,这些项目 旨在通过降低成本来提高盈利能力(美元/美元)去年同期的同比百分比变化百分比 29

联系信息投资者关系美国股票信息 各州:纽约证券交易所(ADS):+1 877 7CX 墨西哥纽约证券交易所 CX:墨西哥证券交易所 +52 81 8888 4292(CPO):CEMEX.CPO ir@cemex.com CPO CPO 与 ADS 的比例:10 比 1

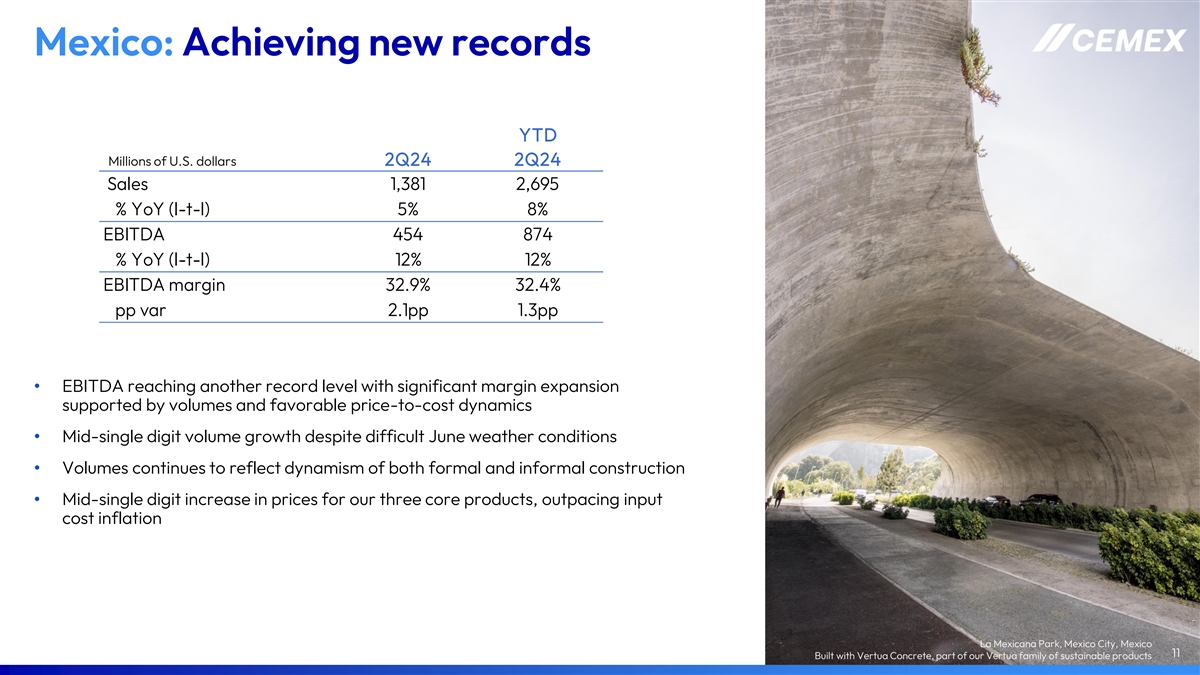

Mexico: Achieving new records YTD Millions of U.S. dollars 2Q24 2Q24 Sales 1,381 2,695 % YoY (l-t-l) 5% 8% EBITDA 454 874 % YoY (l-t-l) 12% 12% EBITDA margin 32.9% 32.4% pp var 2.1pp 1.3pp • EBITDA reaching another record level with significant margin expansion supported by volumes and favorable price-to-cost dynamics • Mid-single digit volume growth despite difficult June weather conditions • Volumes continues to reflect dynamism of both formal and informal construction • Mid-single digit increase in prices for our three core products, outpacing input cost inflation La Mexicana Park, Mexico City, Mexico 11 Built with Vertua Concrete, part of our Vertua family of sustainable products

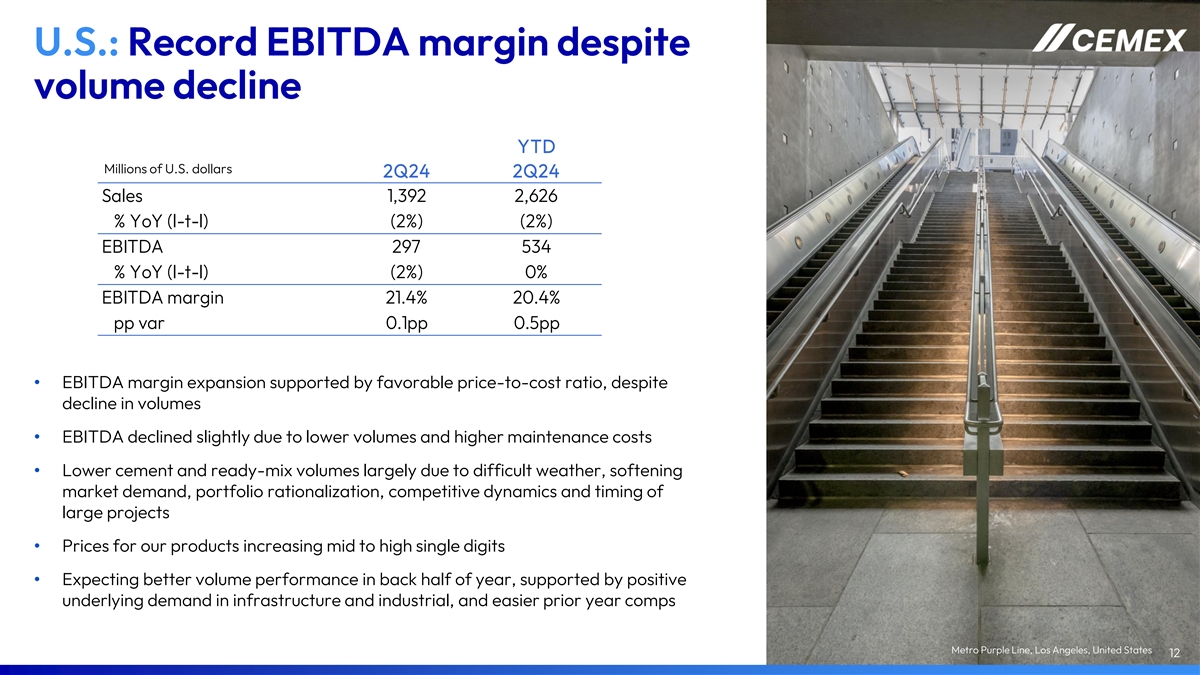

U.S.: Record EBITDA margin despite volume decline YTD Millions of U.S. dollars 2Q24 2Q24 Sales 1,392 2,626 % YoY (l-t-l) (2%) (2%) EBITDA 297 534 % YoY (l-t-l) (2%) 0% EBITDA margin 21.4% 20.4% pp var 0.1pp 0.5pp • EBITDA margin expansion supported by favorable price-to-cost ratio, despite decline in volumes • EBITDA declined slightly due to lower volumes and higher maintenance costs • Lower cement and ready-mix volumes largely due to difficult weather, softening market demand, portfolio rationalization, competitive dynamics and timing of large projects • Prices for our products increasing mid to high single digits • Expecting better volume performance in back half of year, supported by positive underlying demand in infrastructure and industrial, and easier prior year comps Metro Purple Line, Los Angeles, United States 12

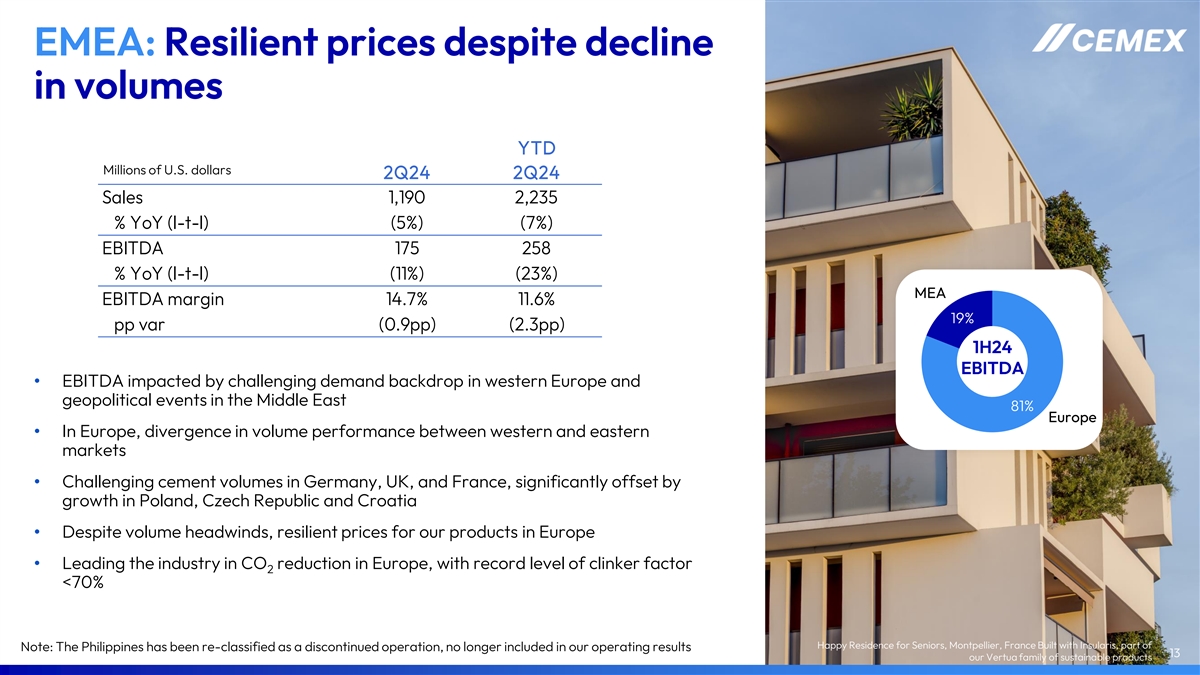

EMEA: Resilient prices despite decline in volumes YTD Millions of U.S. dollars 2Q24 2Q24 Sales 1,190 2,235 % YoY (l-t-l) (5%) (7%) EBITDA 175 258 % YoY (l-t-l) (11%) (23%) MEA EBITDA margin 14.7% 11.6% 19% pp var (0.9pp) (2.3pp) 1H24 EBITDA • EBITDA impacted by challenging demand backdrop in western Europe and geopolitical events in the Middle East 81% Europe • In Europe, divergence in volume performance between western and eastern markets • Challenging cement volumes in Germany, UK, and France, significantly offset by growth in Poland, Czech Republic and Croatia • Despite volume headwinds, resilient prices for our products in Europe • Leading the industry in CO reduction in Europe, with record level of clinker factor 2

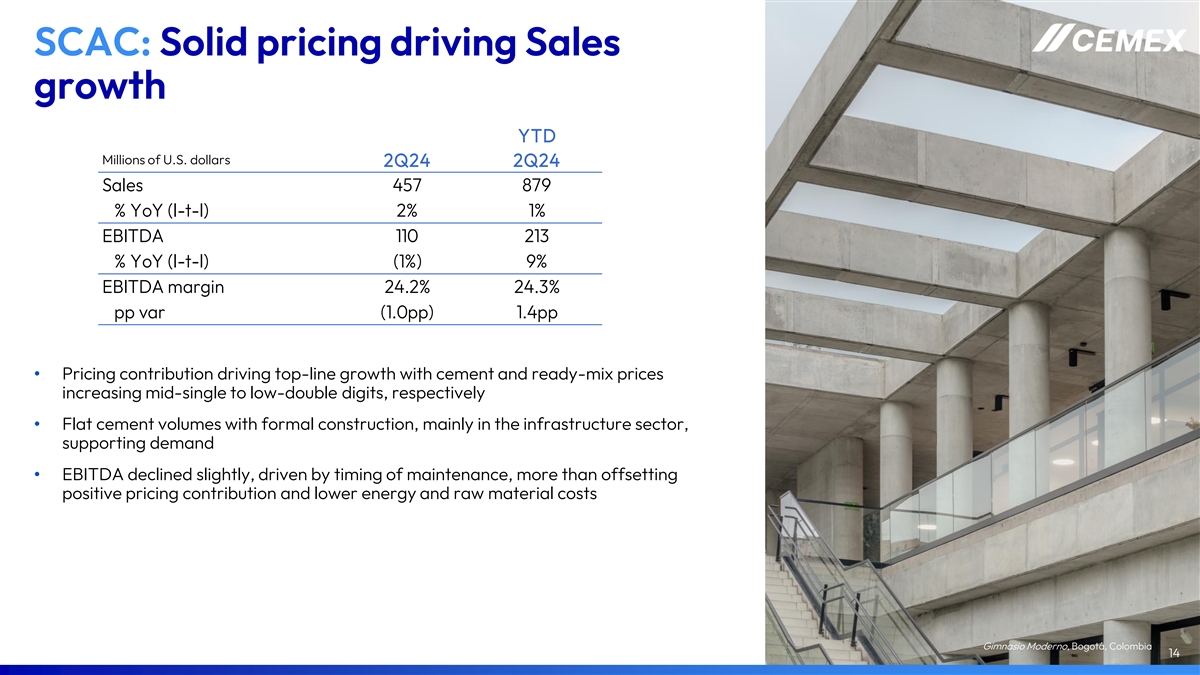

SCAC: Solid pricing driving Sales growth YTD Millions of U.S. dollars 2Q24 2Q24 Sales 457 879 % YoY (l-t-l) 2% 1% EBITDA 110 213 % YoY (l-t-l) (1%) 9% EBITDA margin 24.2% 24.3% pp var (1.0pp) 1.4pp • Pricing contribution driving top-line growth with cement and ready-mix prices increasing mid-single to low-double digits, respectively • Flat cement volumes with formal construction, mainly in the infrastructure sector, supporting demand • EBITDA declined slightly, driven by timing of maintenance, more than offsetting positive pricing contribution and lower energy and raw material costs Gimnasio Moderno, Bogotá, Colombia 14

Financial Developments Pelješac Bridge, Pelješac, Croatia Built with Vertua Concrete, part of our Vertua family of sustainable products

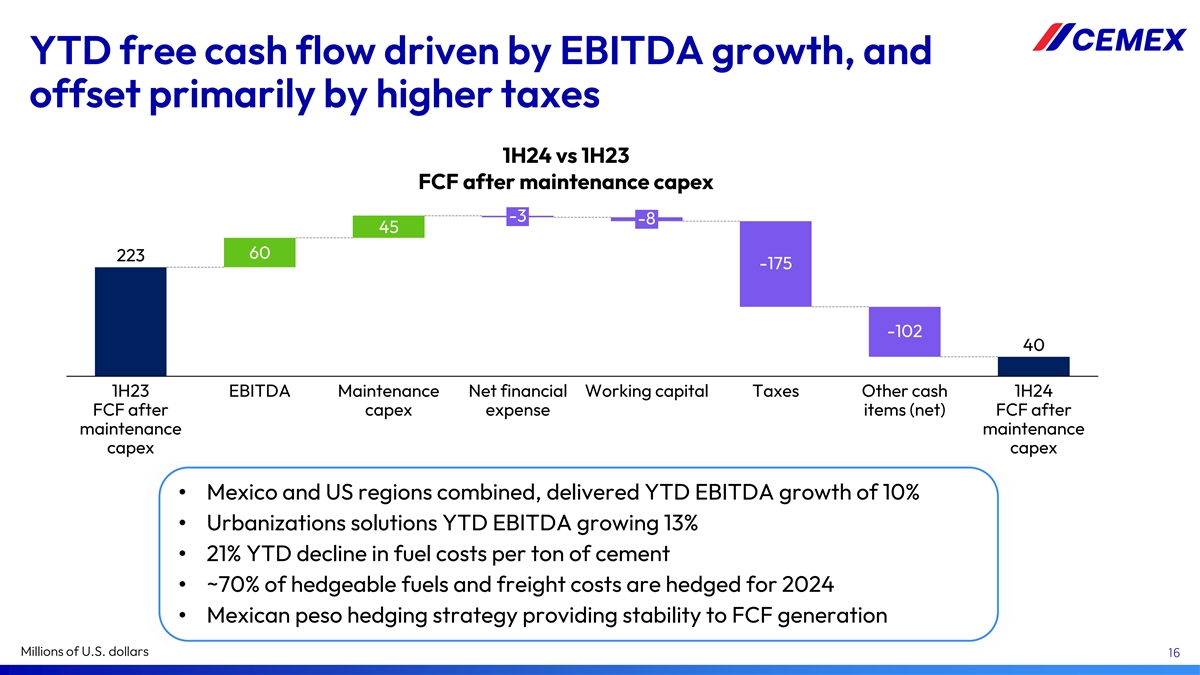

YTD free cash flow driven by EBITDA growth, and offset primarily by higher taxes 1H24 vs 1H23 FCF after maintenance capex -3 -8 45 60 223 -175 -102 40 1H23 EBITDA Maintenance Net financial Working capital Taxes Other cash 1H24 FCF after capex expense items (net) FCF after maintenance maintenance capex capex • Mexico and US regions combined, delivered YTD EBITDA growth of 10% • Urbanizations solutions YTD EBITDA growing 13% • 21% YTD decline in fuel costs per ton of cement • ~70% of hedgeable fuels and freight costs are hedged for 2024 • Mexican peso hedging strategy providing stability to FCF generation Millions of U.S. dollars 16

2024 Outlook Gilbert Chabroux School, Lyon, France Built with Insularis, part of our Vertua family of sustainable products

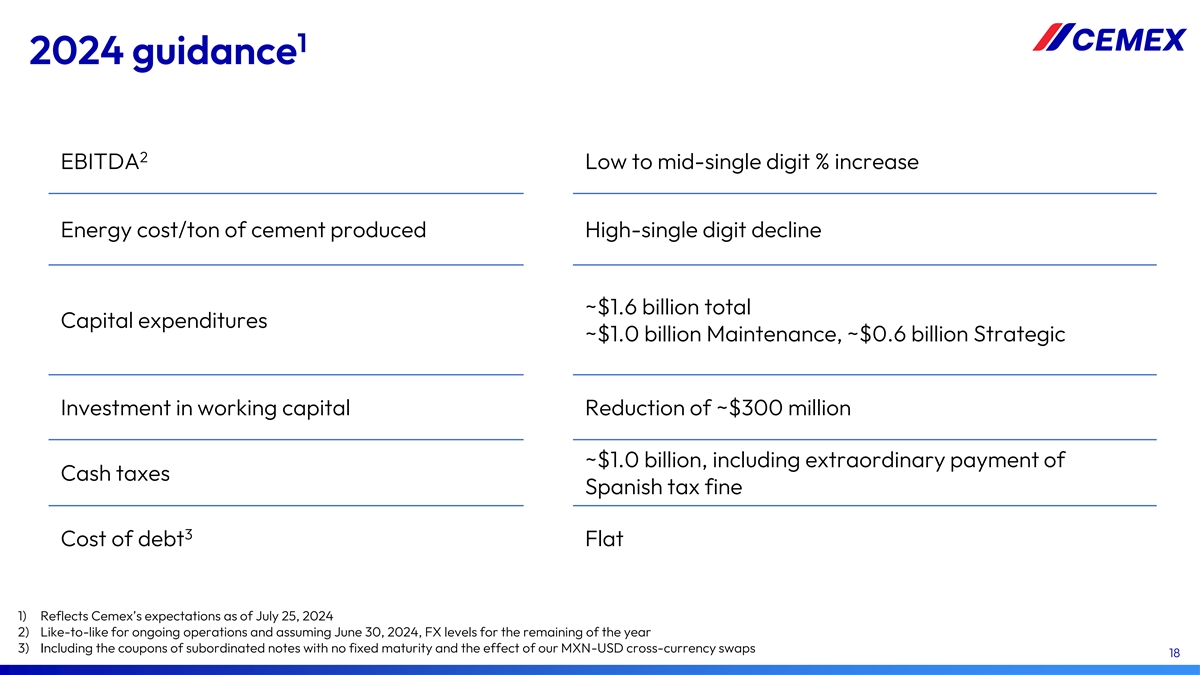

1 2024 guidance 2 EBITDA Low to mid-single digit % increase Energy cost/ton of cement produced High-single digit decline ~$1.6 billion total Capital expenditures ~$1.0 billion Maintenance, ~$0.6 billion Strategic Investment in working capital Reduction of ~$300 million ~$1.0 billion, including extraordinary payment of Cash taxes Spanish tax fine 3 Cost of debt Flat 1) Reflects Cemex’s expectations as of July 25, 2024 2) Like-to-like for ongoing operations and assuming June 30, 2024, FX levels for the remaining of the year 3) Including the coupons of subordinated notes with no fixed maturity and the effect of our MXN-USD cross-currency swaps 18

Appendix International Museum of Baroque, Puebla, Mexico

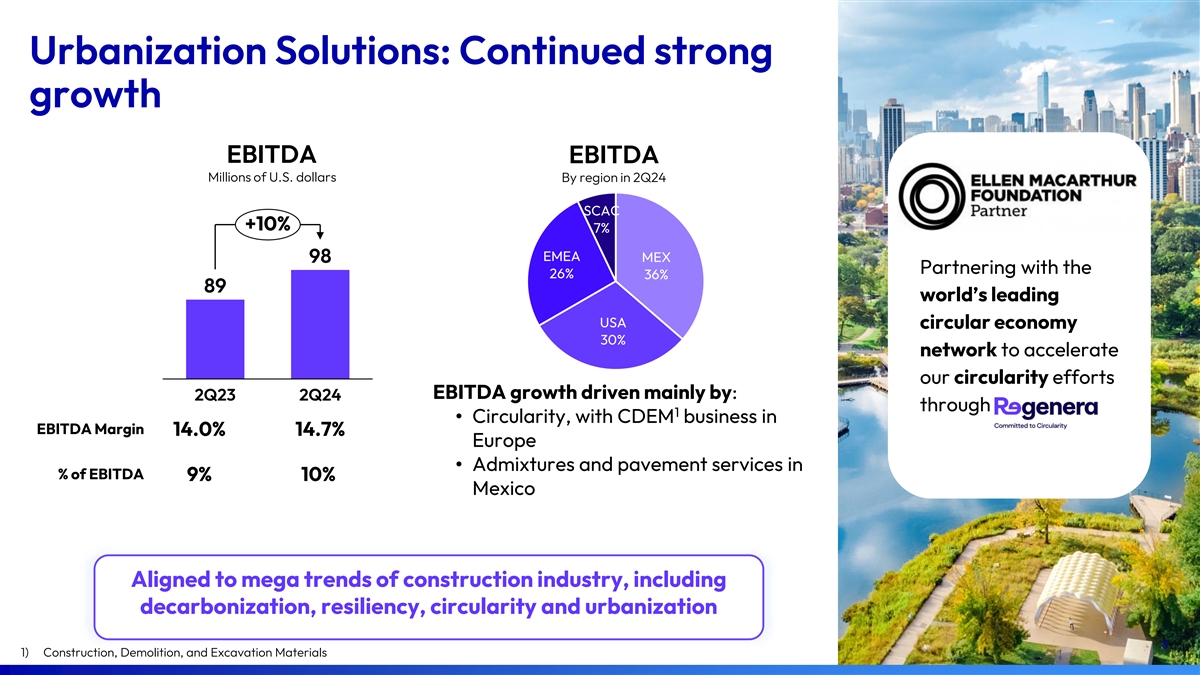

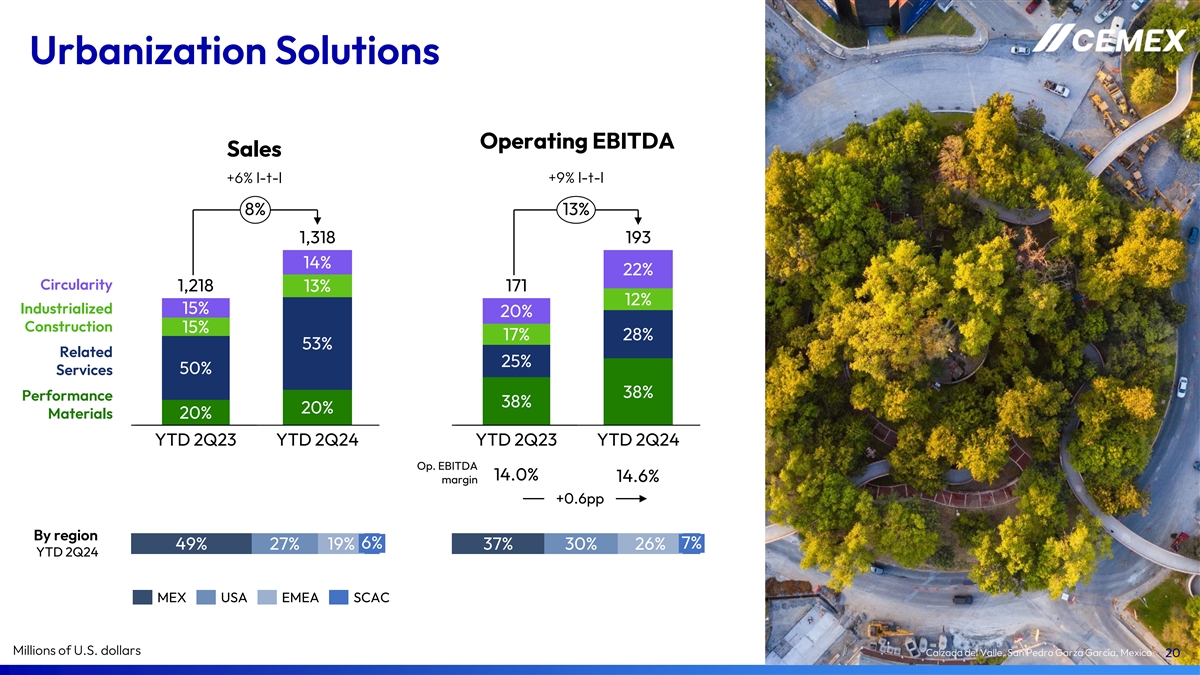

Urbanization Solutions Operating EBITDA Sales +9% l-t-l +6% l-t-l 8% 13% 1,318 193 14% 22% Circularity 1,218 171 13% 12% Industrialized 15% 20% Construction 15% 17% 28% 53% Related 25% 50% Services 38% Performance 38% 20% Materials 20% YTD 2Q23 YTD 2Q24 YTD 2Q23 YTD 2Q24 Op. EBITDA 14.0% 14.6% margin +0.6pp By region 6% 7% 49% 27% 19% 37% 30% 26% YTD 2Q24 MEX USA EMEA SCAC Millions of U.S. dollars Calzada del Valle, San Pedro Garza García, Mexico 20

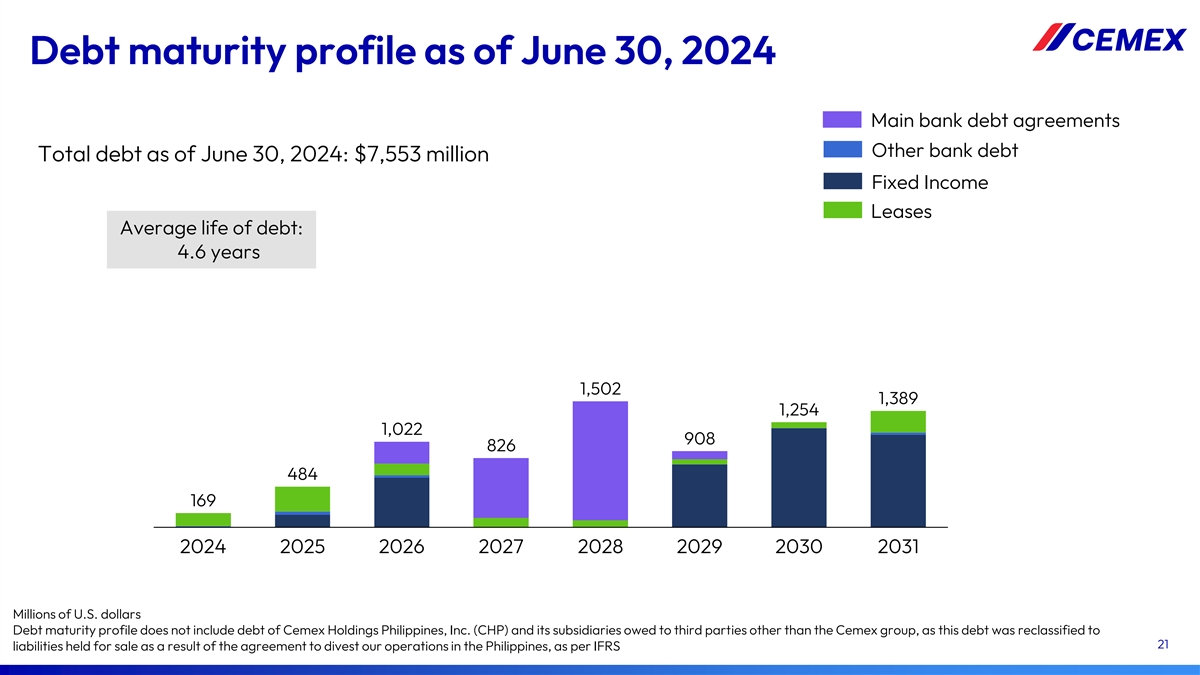

Debt maturity profile as of June 30, 2024 Main bank debt agreements Other bank debt Total debt as of June 30, 2024: $7,553 million Fixed Income Leases Average life of debt: 4.6 years 1,502 1,389 1,254 1,022 908 826 484 169 2024 2025 2026 2027 2028 2029 2030 2031 Millions of U.S. dollars Debt maturity profile does not include debt of Cemex Holdings Philippines, Inc. (CHP) and its subsidiaries owed to third parties other than the Cemex group, as this debt was reclassified to 21 liabilities held for sale as a result of the agreement to divest our operations in the Philippines, as per IFRS

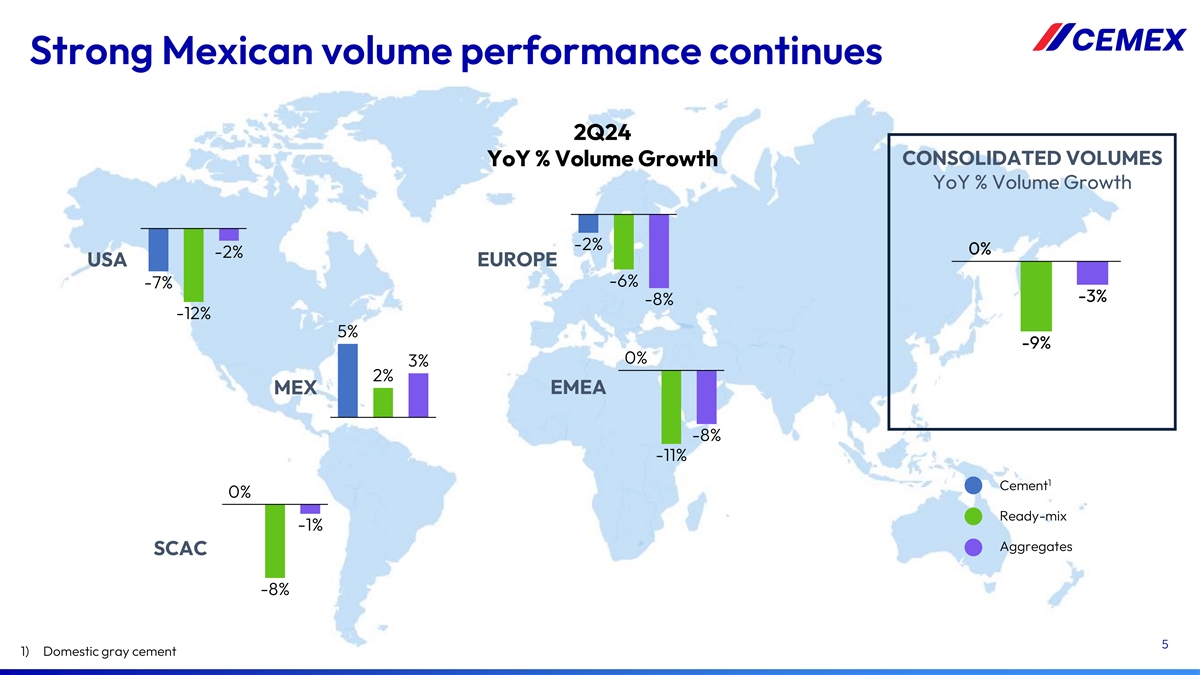

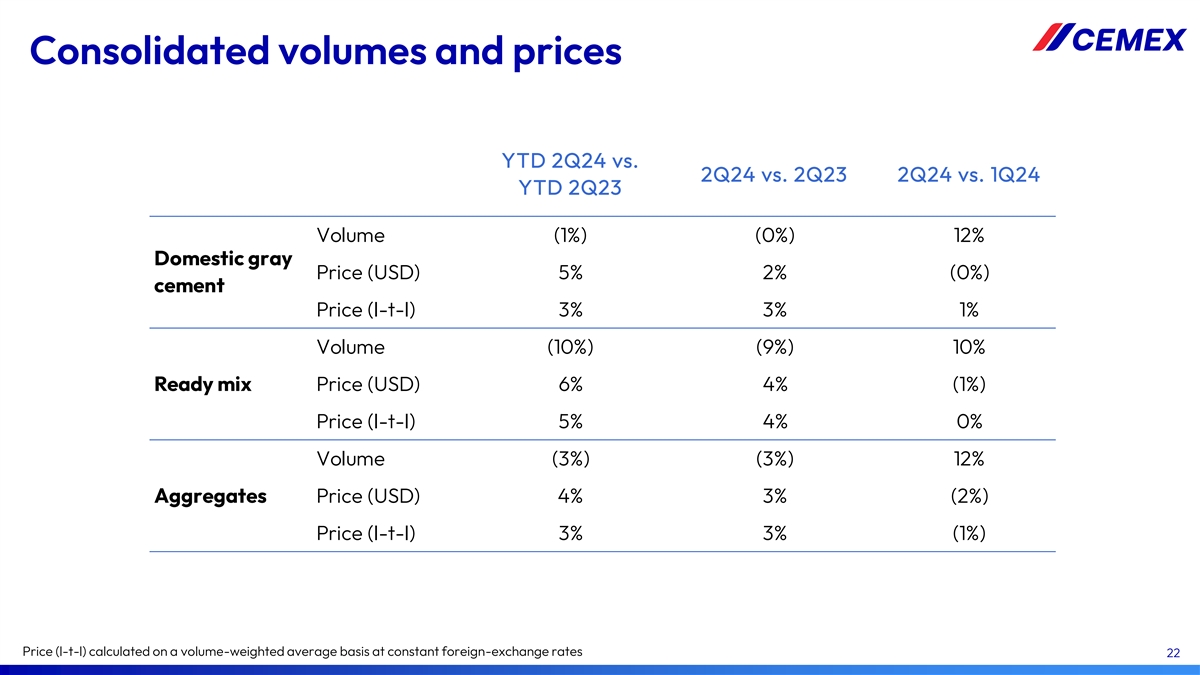

Consolidated volumes and prices YTD 2Q24 vs. 2Q24 vs. 2Q23 2Q24 vs. 1Q24 YTD 2Q23 Volume (1%) (0%) 12% Domestic gray Price (USD) 5% 2% (0%) cement Price (l-t-l) 3% 3% 1% Volume (10%) (9%) 10% Ready mix Price (USD) 6% 4% (1%) Price (l-t-l) 5% 4% 0% Volume (3%) (3%) 12% Aggregates Price (USD) 4% 3% (2%) Price (l-t-l) 3% 3% (1%) Price (l-t-l) calculated on a volume-weighted average basis at constant foreign-exchange rates 22

Additional information on debt Other MXN 3% Second Quarter First Quarter 5% Euro 2023 2024 % var 2024 15% 1 7,665 7,553 (1%) 7,844 Total debt 3 Currency Short-term 4% 4% 4% denomination U.S. Long-term 96% 96% 96% dollar 78% Cash and cash equivalents 471 425 (10%) 476 Net debt 7,194 7,128 (1%) 7,369 2 7,281 7,208 (1%) 7,371 Consolidated net debt 2 2.45 2.13 2.18 Consolidated leverage ratio Variable 2 30% 6.90 7.72 7.80 Consolidated coverage ratio 3 Interest rate Fixed Millions of U.S. dollars. For second quarter 2024, Total debt and Net debt do not include debt of Cemex Holdings Philippines, Inc. (CHP) and its subsidiaries owed to third 70% parties other than the Cemex group, as this debt was reclassified to liabilities held for sale as a result of the agreement to divest our operations in the Philippines, as per IFRS. 1) Includes leases, in accordance with IFRS 2) Calculated in accordance with our contractual obligations under our main bank debt agreements; includes EBITDA and debt from our Philippines operations 3) Includes the effect of our interest rate and cross-currency derivatives, as applicable 23

Additional information on debt Total debt by instrument First Quarter Second Quarter 2024 % of total 2024 % of total Fixed Income 3,845 49% 3,777 50% Main Bank Debt Agreements 2,473 32% 2,488 33% 50% Leases 1,272 16% 1,174 16% 33% Other 254 3% 115 2% Total Debt 7,844 7,553 16% 2% Millions of U.S. dollars For second quarter 2024, Total Debt does not include debt of Cemex Holdings Philippines, Inc. (CHP) and its subsidiaries owed to third parties other than the Cemex group, as this debt was reclassified to liabilities held for sale as a result of the agreement to divest our operations in the Philippines, as per IFRS. 24

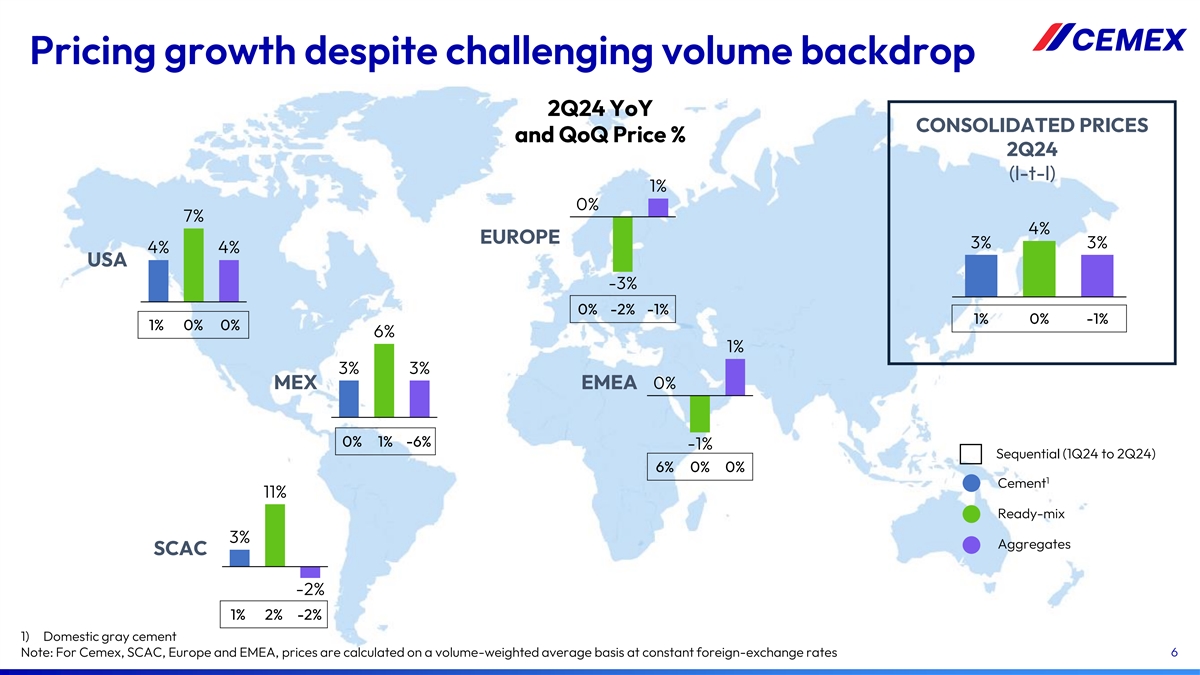

2Q24 volume and price summary: selected countries and regions Domestic gray cement Ready mix Aggregates 2Q24 vs. 2Q23 2Q24 vs. 2Q23 2Q24 vs. 2Q23 Volume Price (USD) Price (LC) Volume Price (USD) Price (LC) Volume Price (USD) Price (LC) Mexico 5% 4% 3% 2% 7% 6% 3% 4% 3% U.S. (7%) 4% 4% (12%) 7% 7% (2%) 4% 4% EMEA (0%) (3%) (0%) (11%) (3%) (1%) (8%) 0% 1% Europe (2%) (0%) (0%) (6%) (4%) (3%) (8%) 1% 1% MEA 6% (21%) 11% (18%) (2%) (0%) (9%) (3%) (2%) SCAC 0% 4% 3% (8%) 19% 11% (1%) 6% (2%) Price (LC) for EMEA, Europe, MEA, and SCAC calculated on a volume-weighted-average basis at constant foreign-exchange rates 25

YTD 2Q24 volume and price summary: selected countries and regions Domestic gray cement Ready mix Aggregates YTD 2Q24 vs. YTD 2Q23 YTD 2Q24 vs. YTD 2Q23 YTD 2Q24 vs. YTD 2Q23 Volume Price (USD) Price (LC) Volume Price (USD) Price (LC) Volume Price (USD) Price (LC) Mexico 6% 8% 3% 2% 14% 10% 6% 16% 11% U.S. (8%) 4% 4% (13%) 8% 8% 3% 1% 1% EMEA (2%) (0%) 1% (14%) (1%) (1%) (12%) 2% 1% Europe (5%) 2% 1% (9%) (2%) (2%) (11%) 3% 2% MEA 5% (8%) 13% (22%) (2%) (0%) (14%) (4%) (3%) SCAC (3%) 6% 5% (8%) 23% 12% (2%) 11% 1% Price (LC) for EMEA, Europe, MEA, and SCAC calculated on a volume-weighted-average basis at constant foreign-exchange rates 26

1 2024 volume guidance : selected countries/regions Cement Ready-mix Aggregates Flat to low-single digit increase Low-single digit decline Flat to low-single digit decline CEMEX Low to mid-single digit increase Low to mid-single digit increase Low-single digit increase Mexico Low-single digit decline Mid-single digit decline Flat USA Flat to low-single digit increase Mid-single digit decline Low-single digit decline EMEA Europe Flat to low-single digit increase Low-single digit decline Flat to low-single digit decline MEA Flat to low-single digit decline Mid-single digit decline Mid-single digit decline SCAC Low-single digit decline Low-single digit decline N/A 1) Reflects Cemex’s expectations as of July 25, 2024. Volumes on a like-to-like basis. All volume guidance in this slide means in percentage terms vs 2023 27

Relevant Sustainability indicators YTD YTD Customers and suppliers 2Q23 2023 2Q24 Carbon strategy 2023 2Q23 2Q24 Net Promoter Score (NPS) 68 70 75 533 Kg of CO per ton of cementitious 549 541 2 % of Sales using CX Go 65% 67% 65% Alternative fuels (%) 36.5% 37.5% 36.3% 73.4% 72.3% 72.2% Clinker factor YTD YTD YTD YTD Low-carbon products 2023 Health and safety 2023 2Q23 2Q24 2Q23 2Q24 Blended cement as % of total 2 3 0 Employee fatalities 81% 81% 81% cement produced Employee L-T-I frequency rate 0.5 0.6 0.6 Vertua concrete as % of total 46% 48% 56% Operations with zero fatalities and 98% 96% 97% injuries (%) Vertua cement as % of total 55% 56% 62% 28

Definitions SCAC South, Central America and the Caribbean EMEA Europe, Middle East and Africa MEA Middle East, and Africa When providing cement volume variations, refers to domestic gray cement operations (starting in 2Q10, the base for reported cement volumes changed Cement from total domestic cement including clinker to domestic gray cement) LC Local currency l-t-l (like to like) On a like-to-like basis adjusting for currency fluctuations and for investments/divestments when applicable Investments incurred for the purpose of ensuring the company’s operational continuity. These include capital expenditures on projects required to replace Maintenance capital obsolete assets or maintain current operational levels, and mandatory capital expenditures, which are projects required to comply with governmental expenditures regulations or company policies When referring to reportable segment sales, revenues are presented before eliminations of intragroup transactions. When referring to Consolidated Sales Sales, these represent the total revenues (Net Sales) of the company as reported in the financial statements. EBITDA Means Operating EBITDA: Operating earnings before other expenses, net plus depreciation and operating amortization EBITDA margin Means Operating EBITDA margin: which is calculated by dividing our “Operating EBITDA” by our sales Cemex defines it as Operating EBITDA minus net interest expense, maintenance and expansion capital expenditures, change in working capital, taxes Free cash flow paid, and other cash items (net other expenses less proceeds from the disposal of obsolete and/or substantially depleted operating fixed assets that are no longer in operation and coupon payments on our perpetual notes) IFRS International Financial Reporting Standards, as issued by the International Accounting Standards Board Pp Percentage points Prices All references to pricing initiatives, price increases or decreases, refer to our prices for our products Strategic capital expenditures Investments incurred with the purpose of increasing the company’s profitability. These include capital expenditures on projects designed to increase profitability by expanding capacity, and margin improvement capital expenditures, which are projects designed to increase profitability by reducing costs USD/U.S. dollars U.S. dollars % YoY Year-over-year percentage variation for the same period of the previous year 29

Contact Information Investors Relations Stock Information In the United States: NYSE (ADS): +1 877 7CX NYSE CX In Mexico: Mexican Stock Exchange +52 81 8888 4292 (CPO): CEMEX.CPO ir@cemex.com Ratio of CPO to ADS: 10 to 1