展品99.3

|

|

在能源转型中茁壮成长气候转型行动计划和2023年进展报告

|

气候和2023年过渡进展行动报告 承认国家伍德赛德的计划承认土著和托雷斯海峡岛民为澳大利亚?S原住民。我们承认它们与土地、水和环境的联系,并向祖先和长辈致敬,无论是过去的还是现在的。我们对世界各地的原住民人民和社区给予这种承认和尊重。关于本报告本《气候过渡行动计划和2023年进展报告》概述了2023年1月1日至2023年12月31日期间的伍德赛德?S气候相关计划、活动、进展和气候相关数据。它旨在提供符合气候相关财务披露特别工作组(TCFD)建议的披露之间的平衡,同时避免向读者提供大量信息。伍德赛德认为,本报告包含符合TCFD的披露?S提出了4项建议和11项建议披露,并注意到其对所有部门的指导和对非金融集团的指导。1,2伍德赛德指出,在完成其2023年状况报告后,TCFD已完成其职权范围并解散。国际清算银行金融安全委员会已要求国际财务报告准则(IFRS)基金会接管对公司进展的监督?与气候有关的披露。本报告的编制也参考了可持续会计准则委员会(SASB)石油和天然气勘探与生产标准中选定的相关指标。3索引将本报告中的内容与这些建议交叉引用。鉴于本气候过渡行动计划的重点,它必须面向未来事件, 包含有关伍德赛德与气候变化相关的计划、战略、目标、指标、抱负等的前瞻性信息。无论是我们帮助我们实现战略目标的计划,还是本报告更一般的内容,都不是对未来事件将会或可能发生的声明、保证或预测。关于本报告范围的进一步详情,包括免责声明、风险、排放数据和其他重要信息,载于第81-82页。除非另有说明,所有美元均以美国货币伍德赛德股票表示。除非另有说明,排放是指温室气体排放。伍德赛德能源集团有限公司(ABN 55 004 898 962)是伍德赛德集团公司的最终控股公司。在本报告中,除非另有说明,否则指的是伍德赛德、我们的、我们的。或者?我们?请参考伍德赛德能源集团有限公司及其控制的实体。2023年年报我们的2023年年报提供了截至2023年12月31日的12个月期间伍德赛德?S的运营和活动以及伍德赛德?S截至2023年12月31日的财务状况的摘要。它还提供了截至2023年12月31日的12个月期间伍德赛德?S的可持续发展方法、健康和安全绩效以及其他 信息的摘要。2023年年度报告和本气候转型行动计划以及2023年进展报告共同为伍德赛德?S的业务提供了补充回顾。这些报告可在我们的 网站伍德赛德网站上找到。报告反馈我们欢迎对本《气候过渡行动计划》和《2023年进度报告》的反馈,请发送至pananyinfo@wood side.com。GHD Pty Ltd已对选定的温室气体排放数据进行了有限保证。有关保证范围的更多信息,请参阅第83页。封面以日本东京的天际线为特色。1金融稳定委员会,2017年。?与气候有关的财务披露问题工作队的建议。最终报告。?图4,第14页。TCFD的一些要素?S的四项建议和11项建议公开以不同的顺序列出,以增强可读性。第80页提供了TCFD和本报告之间的交叉引用。2金融稳定委员会,2021年。?执行气候相关财务披露工作队的建议。3 SASB,2018。?石油和天然气?勘探和生产。可持续性 会计准则。版本2018-10。?表1,第6页,伍德赛德?S气候过渡行动计划和2023年进展报告伍德赛德能源集团有限公司2

|

内容1.摘要4 1.1倾听和回应4 1.2如何阅读本报告8 2.治理10 2.1董事会监督11 3.脱碳战略13 3.1气候战略14 3.2 2023净股本范围1和2排放绩效16 3.3净股本范围1和2:净零行动计划18 3.4碳 信用额度28 3.5范围3排放32 3.6范围3目标34 3.7支持我们的价值链41 4.资本分配42 4.1资本调整43 4.2全球石油和天然气需求天然气44 4.3天然气的角色演变46 4.4通过多元化管理不确定性 48 4.5评估转型弹性的投资决策50 4.6伍德赛德?S投资组合的情景分析52 4.7客户关系54 5.风险管理56 5.1风险管理框架57 5.2与气候有关的关键风险和机会59 5.3管理实物风险62 6.参与度64 6.1政策参与度65 6.2行业倡议67 6.3 A刚刚过渡68 6.4内部气候参与度70 7.附录71 7.1与气候有关的数据72 7.2关于2023年范围1和范围2排放报废的碳信用来源74 7.3范围3方法75 7.4词汇表77 7.5索引80 7.6免责声明,风险、排放数据和其他重要信息81 7.7 GHD保证声明83伍德赛德?S气候过渡行动计划和2023年进展报告伍德赛德能源集团有限公司III

|

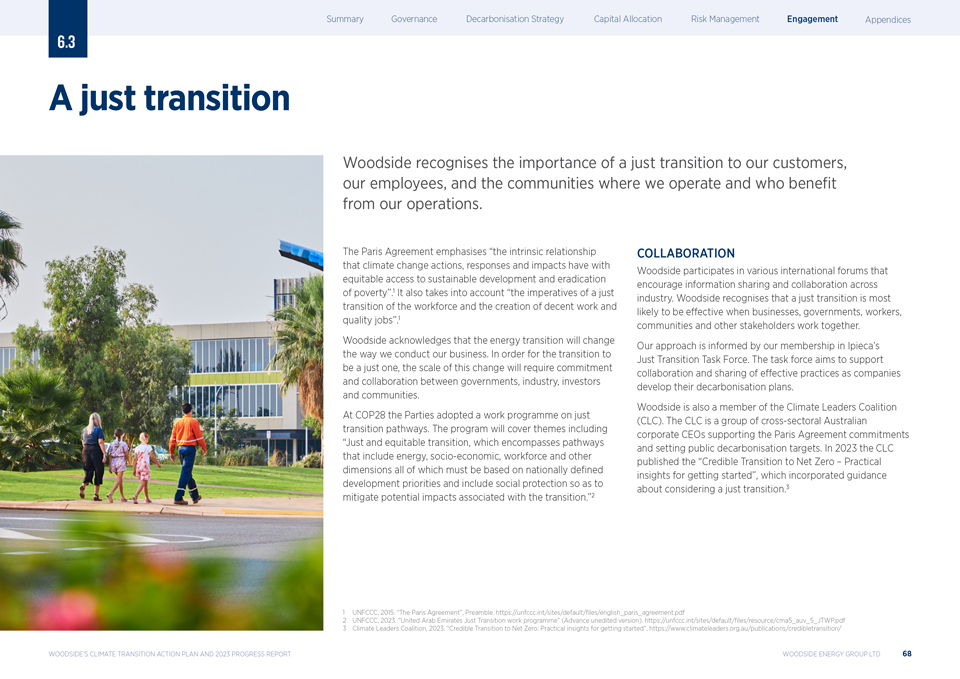

倾听和回应伍德赛德?S对气候变化的回应 融入了我们公司的战略,以在能源转型中蓬勃发展。在2023年期间,我仔细听取了我们的投资者的意见,他们告诉我,他们想要关于我们的气候行动计划的更详细的信息。因此,这份气候转型行动计划是我们之前披露的内容的演变。更新还记录了我们减少净资产范围1和2排放的计划的进展和结果,并投资于能源过渡的产品和服务。对我们产品的需求 投资者的一个关键要求是解释更多关于过渡期间对我们产品的未来需求,以及为什么我们相信伍德赛德?S项目将具有竞争力。这是成功且有利可图地将全球能源需求转化为我们产品实现销售的关键。因此,我们在本报告中包含了更多信息,包括:分析全球能源市场可能如何发展,包括可能将升温限制在1.5摄氏度以下的情况;天然气在能源转型中的潜在作用;我们如何评估我们的投资对能源转型关键方面的弹性;我们如何与客户合作加强我们的贸易关系;以及 了解我们关键市场的政策。将斯卡伯勒合资公司10%的股份出售给LNG日本公司,并将15.1%的股份出售给JERA,这是双方需求一致的一个例子。1这些战略关系还包括潜在的LNG承购和在新能源机会上的合作。范围1和范围2排放我们还提供了我们在范围1和范围2减排方面的最新进展,以及我们未来的计划。2023年,我们实现了净权益范围1和范围2排放量在起始基数下减少12.5%。与2022.2年度的11%相比,由于我们设施的潜在排放表现,我们使用的碳信用作为补偿比去年减少了13%。我们在我们合并的运营资产组合中完成了脱碳计划 ,确定了多个技术选项,以减少我们当前投资组合的范围1和范围2的总排放量。这些计划中的技术也可用于设计我们增长机会的排放 。我们继续发展我们的碳信用投资组合。我们还包括了有关其规模和组成的更多信息,以及我们用来评估其完整性的尽职调查程序。与本页相关的所有脚注均显示在下一页上。伍德赛德?S气候转型行动计划和2023年进展报告伍德赛德能源集团有限公司4

|

范围3排放我们的范围3方法包括 在我们的产品组合中引入新产品和服务,如氢和碳捕获利用和储存(CCUS)。这些产品和服务可以帮助我们的客户避免或减少其范围1或2的排放,从而降低我们产品组合的生命周期(范围1、2和3)的排放强度。2023年,我们继续审查我们对范围3目标的方法,以回应投资者的反馈,并决定用新的补充性减排目标来补充我们现有的投资目标。这一目标是到2030年在新能源产品和低碳服务方面做出国家投资决策,总减排能力达到5 Mtpa CO-E.3 2投资目标跟踪我们开发这些项目并将其推向市场的工作。减排目标将跟踪它们对客户排放的影响。2023年在碳捕获和储存(CCS)和氢气机会方面的支出超过2.35亿美元,与2022年相比增长了135% ,朝着我们到2030.3年前在新能源产品和低碳服务上投资50亿美元的目标不断迈进。4我们在本报告中是否包含了关于我们的CCS和氢气项目进展的更多信息,以及实现我们的目标的风险?例如确保有利可图的客户流失?以及我们正在做些什么来应对这些风险。治理由我们的主席Richard Goyder领导的董事会监督我们的气候工作,以便我们对气候变化的治理反映它对我们公司的战略重要性。作为我们对董事会技能和组成的持续审查的一部分,我们在2023年进行了改革,以加强我们的董事会和委员会,目的是使它们处于最佳地位,以支持我们的全球业务, 以及我们在能源转型期间的战略增长机会。董事会还决定修订我们的高管薪酬框架,以使范围1和2排放总量以及新能源项目进展的目标 将影响高管领导团队绩效薪酬的结果。除了披露我们的政策宣传活动外,我们还审查了我们的行业协会成员资格,包括评估行业协会活动是否支持《巴黎协定》的目标。我们已经在我们的网站上公布了审查结果。本气候转型行动计划将于2024年4月在我们的年度股东大会(AGM)上进行顾问股东投票。我相信它值得我们股东的坚定支持?这是对我们的计划、我们的进展和我们的挑战的彻底审查。但这并不是最后的决定。我们的战略和业绩已经并将在未来几年继续发展。我们将继续积极寻求股东的反馈意见。未来几年将发布进度报告,并对三年后计划的更新计划进行进一步投票?时间,或在特殊情况需要时更早 。梅格·奥尼尔担任董事首席执行官兼董事总经理2024年2月1请访问Woodside网站,查看题为?伍德赛德将向日本液化天然气公司出售10%斯卡伯勒权益?(2023年8月8日)和?伍德赛德将向杰拉出售15.1%斯卡伯勒权益?(2024年2月23日)的公告。温室气体排放数据,包括本气候过渡行动计划中对未来减排计划的图表和估计,没有更新以反映由于向JERA出售15.1%的权益而导致的伍德赛德?S在斯卡伯勒合资企业的股权份额的变化。2目标和期望是净权益范围1和2的温室气体排放量,相对于6.32公吨CO-e的起始基数,代表2016-2020年权益范围1和2温室气体排放的年均总量,可根据生产或受制裁资产的潜在权益变化进行调整(上调或下调),但在2021年前作出最终投资决定。净权益排放量包括利用碳信用作为补偿。3范围3的目标取决于商业安排、商业可行性、监管和合资企业的批准以及第三方活动(可能进行也可能不进行)。个人投资 以伍德赛德?S的投资目标为准。而不是指导。可能既包括有机投资,也包括无机投资。4包括RFSU之前在新能源产品和低碳服务上的支出,这些服务可以通过使用这些产品和服务来帮助我们的客户实现脱碳。这笔资金不用于为减少伍德赛德?S净股本范围1和2的排放提供资金,这两个范围通过资产脱碳计划单独管理。伍德赛德?S气候转型行动计划和2023年进展 报告沃德赛德能源集团能源集团有限公司5

|

重点介绍减少净权益范围1和2温室气体排放2023业绩范围1和2权益范围1和2总权益温室气体排放量(Mt CO?-e)温室气体排放强度3 8 35 6估计的避免生产排放量1 30抵消排放量Boe 4/Woodside净值-CO2 25必和必拓2资产排放津贴kg(合并前)合并实体0起点基数2 20 2022 2023全球平均伍德赛德森林2023估计2022 2023 2050净零预期潜在途径净零(权益范围1和2年平均Mtpa CO-e)4 2在投资组合中生产资产和批准项目8 6 4正在进行中的机会2抵消4 2016-2020年开始净排放量2 2023 2024-2030 2031-2040 2041-2050净排放量比开始基数低12.5%,从20222年度的11%上升?由于我们设施的潜在排放表现,用作补偿的碳信用比去年减少了13%。?正在实现净资产范围1和2的减排目标:到2025年减少15%,到2030年减少30%。?总排放强度低于(好于)可比能源组合的基准?并在2023.3作了进一步改进,1避免排放的量化本质上是不确定的。然而,可以通过与液化天然气、常规大陆架和深水资产组合的基准进行比较来提供估计,这些资产组合的产量为187.2 Mboe(2023年伍德赛德权益产量),产品组合与伍德赛德类似。有许多潜在基准可提供对2023年全球石油和天然气作业平均排放强度的估计。基于Wood Mackenzie?S排放基准工具,估计避免排放量约为391kt CO-e,而根据国际能源署S?石油和天然气行业净零过渡2(2023年11月)表3.1中报告的行业平均排放量,估计避免排放量约为1,705kt CO-e。此图表中显示的估计避免排放量 表示2两个估计值之间的范围。伍德赛德没有独立核实这些估计背后的数据。2目标和期望是净权益范围1和2温室气体排放量相对于6.32公吨CO-e的起始基数 ,这2代表2016-2020年权益范围1和2温室气体排放的年平均总量,可能会进行调整(在合并的运营资产组合中完成资产脱碳计划4?多个避免或减少排放的选项正在进行中:斯卡伯勒的设计中纳入了节省的约16公吨CO-e(累积到2050年),2个冥王星列车2和Trion项目约12公吨CO-e(累积到2050年),在现有资产的进一步削减 举措中,目标是在2030~35公吨CO-e(累积到2050年)之前实施2更多机会(大规模但追溯成本昂贵)2计划成熟技术和降低成本作为未来的选择选项。? 碳信用组合:管理下的20公吨CO-E,以2

|

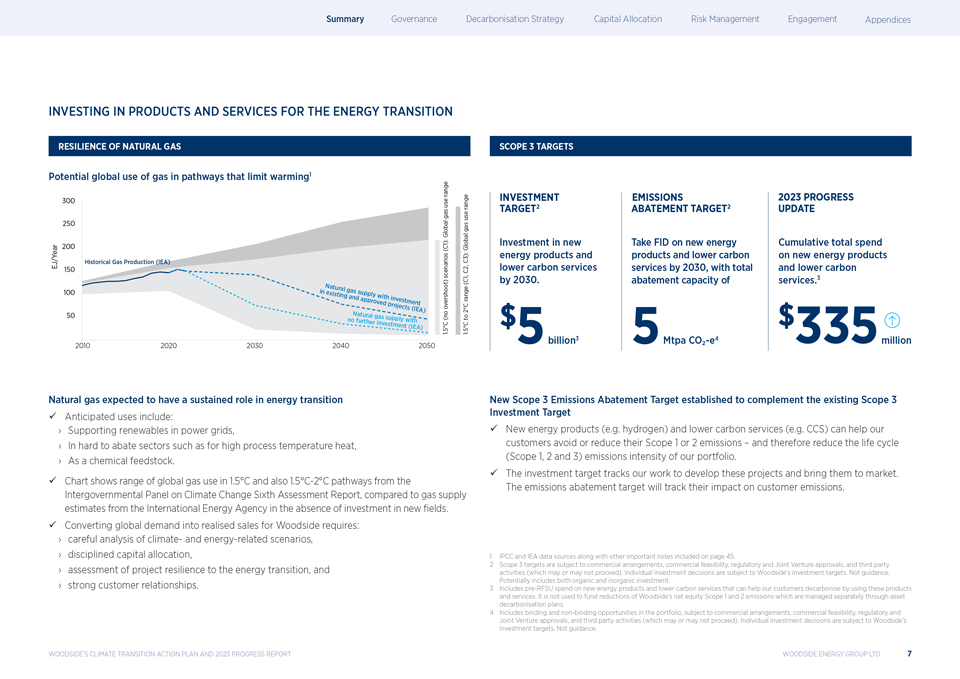

INVESTING IN PRODUCTS AND SERVICES FOR THE ENERGY TRANSITION RESILIENCE OF NATURAL GAS Potential global use of gas in pathways that limit warming1 range 300 use gas range 250 use Globalgas 200 (C1): Global C3): Historical Gas Production (IEA) EJ/Year 150 C2, scenarios (C1, Natural 100 in exis gas supply ting and with appr inves range oved projectmen ts t overshoot) (IEA) 2C 50 Natural gas supply (noto no further with investmen t (IEA) 5C 5C 1 . 1 . 2010 2020 2030 2040 2050 SCOPE 3 TARGETS INVESTMENT EMISSIONS 2023 PROGRESS TARGET2 ABATEMENT TARGET2 UPDATE Investment in new Take FID on new energy Cumulative total spend energy products and products and lower carbon on new energy products lower carbon services services by 2030, with total and lower carbon by 2030. abatement capacity of services.3 $ $ 5billion3 5Mtpa CO?-e4 335million Natural gas expected to have a sustained role in energy transition ? Anticipated uses include: Supporting renewables in power grids, In hard to abate sectors such as for high process temperature heat, As a chemical feedstock. ? Chart shows range of global gas use in 1.5C and also 1.5C-2C pathways from the Intergovernmental Panel on Climate Change Sixth Assessment Report, compared to gas supply estimates from the International Energy Agency in the absence of investment in new ?elds. ? Converting global demand into realised sales for Woodside requires: careful analysis of climate- and energy-related scenarios, disciplined capital allocation, assessment of project resilience to the energy transition, and strong customer relationships. New Scope 3 Emissions Abatement Target established to complement the existing Scope 3 Investment Target ? New energy products (e.g. hydrogen) and lower carbon services (e.g. CCS) can help our customers avoid or reduce their Scope 1 or 2 emissions ? and therefore reduce the life cycle (Scope 1, 2 and 3) emissions intensity of our portfolio. ? The investment target tracks our work to develop these projects and bring them to market. The emissions abatement target will track their impact on customer emissions. 1 IPCC and IEA data sources along with other important notes included on page 45. 2 Scope 3 targets are subject to commercial arrangements, commercial feasibility, regulatory and Joint Venture approvals, and third party activities (which may or may not proceed). Individual investment decisions are subject to Woodside?s investment targets. Not guidance. Potentially includes both organic and inorganic investment. 3 Includes pre-RFSU spend on new energy products and lower carbon services that can help our customers decarbonise by using these products and services. It is not used to fund reductions of Woodside?s net equity Scope 1 and 2 emissions which are managed separately through asset decarbonisation plans. 4 Includes binding and non-binding opportunities in the portfolio, subject to commercial arrangements, commercial feasibility, regulatory and Joint Venture approvals, and third party activities (which may or may not proceed). Individual investment decisions are subject to Woodside?s investment targets. Not guidance. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 7

|

How to read this report GOVERNANCE This section explains how Woodside manages and oversees its response to the challenge of climate change. It includes information about: Board oversight Board skills and composition Executive remuneration Management structure. DECARBONISATION STRATEGY This section explains how Woodside manages emissions associated with its current portfolio. It includes information about: Net equity Scope 1 and 2 emissions performance Net equity Scope 1 and 2 emissions reduction plans Focus topics: Asset decarbonisation in practice Methane emissions management Large scale abatement: vision for Pluto net zero Decarbonisation technology development Our utilisation of carbon credits Our approach to Scope 3 emissions Our progress in developing new energy products and lower carbon services. CAPITAL ALLOCATION This section explains how Woodside integrates consideration of climate change into its investment decisions about new projects. It includes information about: Our capital alignment approach How global energy markets might evolve, including in scenarios that could limit warming to 1.5C How we assess our investments for their resilience to key aspects of the energy transition Scenario analysis of Woodside?s portfolio, including with a 1.5C scenario How we collaborate with customers to strengthen our trading relationships. RISK MANAGEMENT This section explains how Woodside identi?es and manages climate-related risks and opportunities. It includes information about: Our approach to risk management Our identi?ed climate-related risks and opportunities Physical risks. ENGAGEMENT This section explains how Woodside engages with society on climate-related issues. It includes information about: Our advocacy and how we consider the Paris Agreement goals Our lobbying with governments Our memberships of industry associations Our approach to a just transition. Future of reporting This report contains disclosures consistent with TCFD?s four recommendations and eleven recommended disclosures, noting its Guidance for all Sectors and Guidance for Non-Financial Groups. A table cross-referencing the content in this document to the TCFD recommendations is provided on page 80. Woodside supports the harmonisation of climate and sustainability reporting standards intended by the International Sustainability Standards Board (ISSB), and encourages other standard-setting and benchmarking organisations to also align. The Australian Government has con?rmed that it intends to mandate climate reporting standards from 1 July 2024. Woodside and industry associations such as the Business Council of Australia are engaging with the government and the Australian Accounting Standards Board about detailed design issues. We intend to undertake analysis of any changes required in our reporting during the course of 2024, and note the high level alignment of the proposed standards with the recommendations of the TCFD. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 8

|

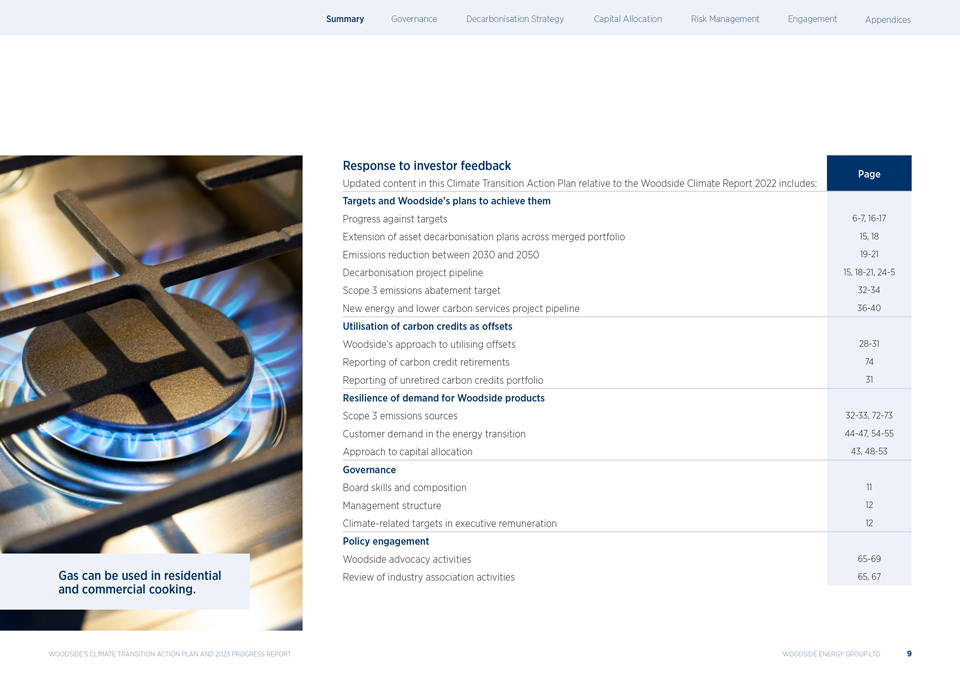

燃气可用于住宅和商业烹饪 。对投资者反馈的回应相对于2022年伍德赛德气候报告的最新内容包括:页面目标和伍德赛德?s的计划实现目标6—7、16—17的进展 在合并后的投资组合中延长资产脱碳计划15、18 2030年至2050年期间的减排19—21脱碳项目管道15、18—21,24—5范围3减排目标32—34新能源和低碳服务项目 管道36—40利用碳信用额作为抵消伍德赛德?利用抵消的方法28—31碳信用额度退役的报告74未退役的碳信用额度组合的报告31对伍德赛德产品的需求的弹性范围3排放源32—33,72—73能源转型中的客户需求44—47,54—55资本分配的方法43,48—53治理委员会的技能和组成11管理结构12高管薪酬中与气候有关的目标12政策参与伍德赛德倡导活动65—69审查行业协会活动65,67伍德赛德?2023年全球气候变迁行动计划与进展报告Woodside Energy Group Limited 9

|

政府天然气用于 发电,为我们的家庭供电。

|

Board oversight The Board of Woodside is responsible for the approval and oversight of our climate change strategy. Climate change is a standing agenda item at each regular meeting of the Sustainability Committee, or the Board when the Sustainability Committee does not meet, with information presented by management, external advisers or third party specialists where appropriate. The Board oversees our climate strategy and receives regular performance updates from management. During 2023, the Board and its Committees were informed about and considered climate-related issues on multiple occasions, including when reviewing and guiding strategy, risk management, annual budgets and business plans, and overseeing major capital expenditure, as well as when setting the Group?s performance objectives and monitoring implementation and performance. The Board continuously reviews progress towards our climate-related targets and our 2050 aspiration by receiving regular updates from the Executive Leadership Team and reports from other management involved in implementing the Group?s climate strategy. The Chair undertakes an annual Governance Roadshow with key institutional investors and investor organisations, including members of Climate Action 100+, to discuss Woodside?s approach to climate change and also listen to any concerns raised by investors. In 2023 the Chair held 43 such meetings. This engagement is supported by our Investor Relations function which had 70 meetings specifically on climate change. BOARD SKILLS AND COMPOSITION The non-executive directors contribute diverse operational and international experience, an understanding of the industry in which Woodside operates, knowledge of ?nancial markets and an understanding of the health, safety, environmental, community and other sustainability matters that are important to Woodside. The Board supplements its climate change awareness by seeking the input of executives and external advisers and specialists to further inform its decisions. The competencies and skills of the directors are set out in the skills matrix described in the Annual Report 2023, in section 4.1. In 2021, the Board skills matrix was updated to include energy transition and climate-related components to reflect the increasing importance of these issues to Woodside?s operations. The Board uses this skills matrix to assess the skills and experience of each director and the combined capabilities of the Board, to identify potential areas of focus for director recruitment and to identify any professional development opportunities that may bene?t directors. In 2023 and early 2024, Woodside announced changes to the membership of its Board of Directors, as part of its continuous review of Board skills and composition. These changes were intended to enhance Woodside?s Board and Committees so that they are best placed to support Woodside?s global operations and strategic growth opportunities through the energy transition. Further information on Board skills and composition is included in the Corporate Governance Statement in section 4.1 of the Annual Report 2023. BOARD COMMITTEES The Board has four standing committees to assist in the discharge of its responsibilities, including on climate change risk. The Sustainability Committee?s responsibilities include reviewing, and making recommendations to the Board on, the Company?s policy and performance in relation to sustainability-related matters, including climate change. The Audit & Risk Committee assists the Board to meet its oversight responsibilities in relation to the company?s financial reporting, compliance with legal and regulatory requirements, internal control structure, risk management and insurance procedures and the internal and external audit functions. Given the importance of climate change as a strategic risk to Woodside, and potential implications relating to financial reporting, it is one of the key risks considered by the Audit & Risk Committee during the review of the company?s risk management framework. The Committee also considers the inclusion of climate-related risks within Woodside?s internal audit program and the appropriateness of disclosures on climate-related risk within the consolidated financial statements. The Nominations & Governance Committee assists the Board with reviewing Board composition, performance and succession planning. This includes identifying, evaluating and recommending candidates for the Board, taking into account the factors set out in the Board skills matrix in section 4.1 of the Annual Report 2023, including energy transition and climate change. The Human Resources & Compensation Committee assists the Board with establishing human resources and compensation policies and practices. Performance based remuneration for the CEO, senior leadership team and all other permanent employees include metrics related to achieving our climate change strategy. Further details are provided in the 2023 Remuneration Report in section 4.3 of the Annual Report 2023. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 11

|

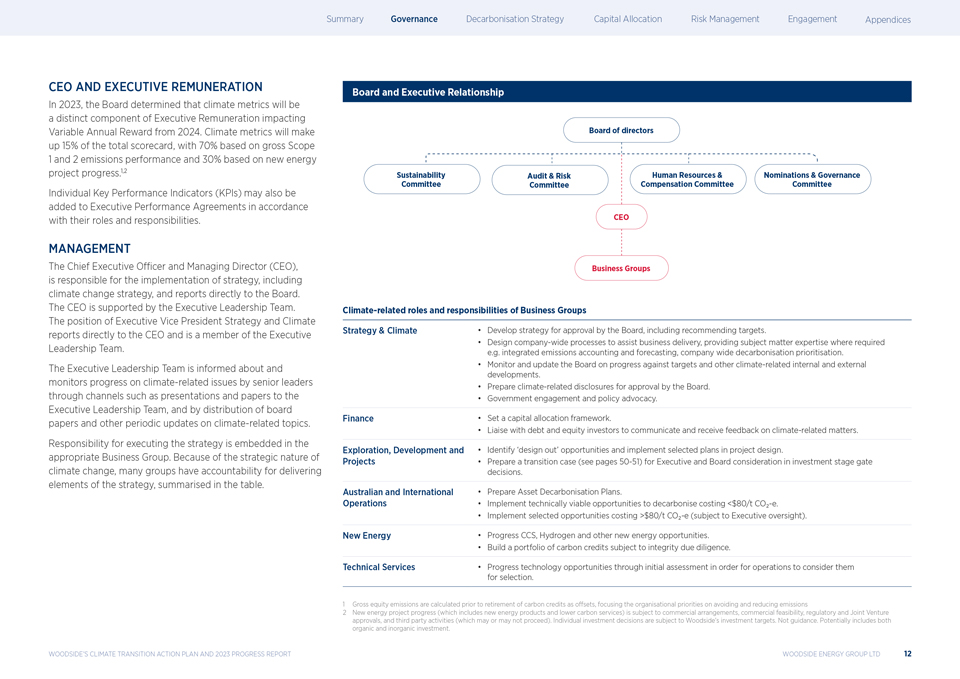

关于2023年CEO和高管薪酬,董事会 决定从2024年起,气候指标将成为影响可变年度薪酬的高管薪酬的一个独特组成部分。气候指标将占总记分卡的15%,其中70%基于总范围1和2排放绩效 ,30%基于新能源项目进度。1、2个单独的关键绩效指标(KPI)也可以根据其角色和职责添加到高管绩效协议中。管理层首席执行官兼董事董事总经理(首席执行官)负责战略的实施,包括气候变化战略,并直接向董事会报告。首席执行官由行政领导团队提供支持。执行副总裁总裁 战略与气候直接向首席执行官汇报,是执行领导团队的成员。高级领导人通过向执行领导团队作报告和文件等渠道,以及分发董事会文件和其他有关气候相关议题的定期更新,向执行领导团队通报气候相关问题的进展情况并监测进展情况。执行战略的责任嵌入到适当的业务组中。由于气候变化的战略性质,许多团体有责任交付该战略的内容,如表所示。董事会和执行关系董事会可持续发展审计和风险人力资源 &提名和治理委员会薪酬委员会首席执行官业务小组气候相关角色和责任业务小组战略和气候发展战略供董事会批准, 包括推荐目标。设计公司范围内的流程,以协助业务交付,在需要时提供主题专业知识,例如集成的排放核算和预测、公司范围内的脱碳优先顺序。监测 并向董事会通报目标的进展情况以及其他与气候有关的内部和外部事态发展。准备与气候有关的披露,以供董事会批准。政府参与和政策倡导。金融设定了资本配置框架 。与债务和股权投资者联络,就气候相关问题进行沟通和接受反馈。探索、开发和识别?设计?在项目设计中提供机会并实施选定的计划。项目准备一个过渡案例(见第50-51页),供执行委员会和董事会在投资阶段大门决策中考虑。澳大利亚和国际准备资产脱碳计划。运营实现了技术上可行的脱碳机会 成本低于80美元/吨CO-E。实施选定的商机,成本超过80美元/吨的CO-E(受管理层监督)。新能源进展CCS、氢气等新能源机遇。建立一个经过 诚信尽职调查的碳信用组合。技术服务通过初步评估提高技术机会,以便运营部门考虑进行选择。1总股本排放量在碳信用报废前计算为补偿 ,将组织重点放在避免和减少排放上2新能源项目进展(包括新能源产品和低碳服务)取决于商业安排、商业可行性、监管 和合资企业批准,以及第三方活动(可能进行也可能不进行)。个人投资决策受制于伍德赛德?S的投资目标。而不是指导。可能包括有机和无机投资。伍德赛德?S气候过渡行动计划和2023年进展报告伍德赛德能源集团有限公司12

|

脱碳策略气体用于各种高温工业流程,如玻璃生产。

|

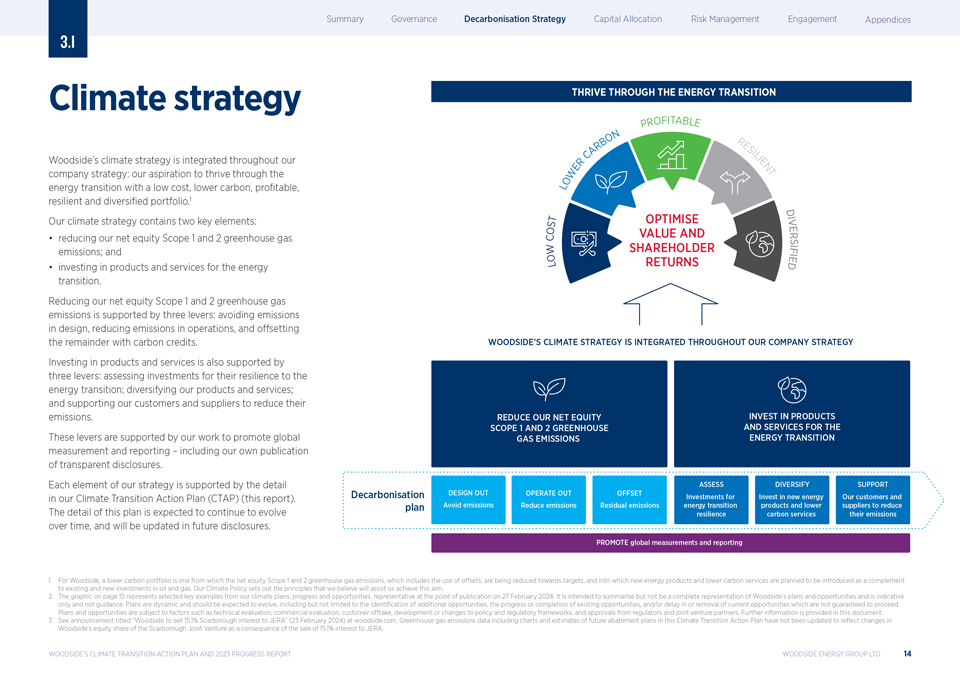

气候战略伍德赛德?S气候战略被整合到我们的公司战略中:我们渴望以低成本、低碳、盈利、弹性和多样化的投资组合在能源转型中蓬勃发展1我们的气候战略包含两个关键要素:减少我们的净权益范围1和2温室气体排放;以及投资于能源转型的产品和服务。减少我们的净权益范围1和2温室气体排放得到三个杠杆的支持:在设计中避免排放,在运营中减少 排放,以及通过碳信用来抵消其余部分。对产品和服务的投资也得到了三个杠杆的支持:评估投资对能源转型的适应能力;使我们的产品和服务多样化;以及支持我们的客户和供应商减少排放。这些杠杆得到了我们促进全球衡量和报告的工作的支持?包括我们自己发布的透明披露。我们的气候转型行动计划(CTAP)(本报告)中的详细内容支持了我们 战略的每一个要素。该计划的细节预计将随着时间的推移而继续演变,并将在未来的披露中更新。在能源转型中茁壮成长 有利可图的N B O R ES A I L R C I E E NT W L O D T优化I S V O价值和E C R S W股东F O回报E I L D伍德赛德?S气候战略整合在我们整个公司的战略脱碳计划1对于伍德赛德,较低的碳 投资组合是指净股权范围1和2的温室气体排放,包括使用抵消,正在朝着目标减少,并计划引入新的能源产品和低碳服务,作为对现有和新的石油和天然气投资的补充。我们的气候政策制定了我们相信将帮助我们实现这一目标的原则。2第15页的图表代表了我们在2024年2月27日发表时具有代表性的气候计划、进展和 机会中精选的关键例子。本文旨在对伍德赛德?S的计划和机会进行总结,但不是完整的表述,仅供参考,而不是指导。计划是动态的, 应预期会发生变化,包括但不限于确定其他机会、现有机会的进展或完成、和/或延迟或删除不能保证继续进行的当前机会。 计划和机会受以下因素的影响:技术评估、商业评估、客户承购、政策和监管框架的发展或更改,以及监管机构和合资伙伴的批准。本文档提供了更多 信息。3参见Woodside将15.1%的Scarborough权益出售给jera?(2024年2月23日)的公告。温室气体排放数据,包括本气候过渡行动计划中对未来减排计划的图表和估计,尚未更新,以反映由于向JERA出售15.1%权益而导致伍德赛德?S在斯卡伯勒合资企业中的股权份额的变化。伍德赛德?S气候转型行动计划和2023年进展报告伍德赛德能源集团有限公司14

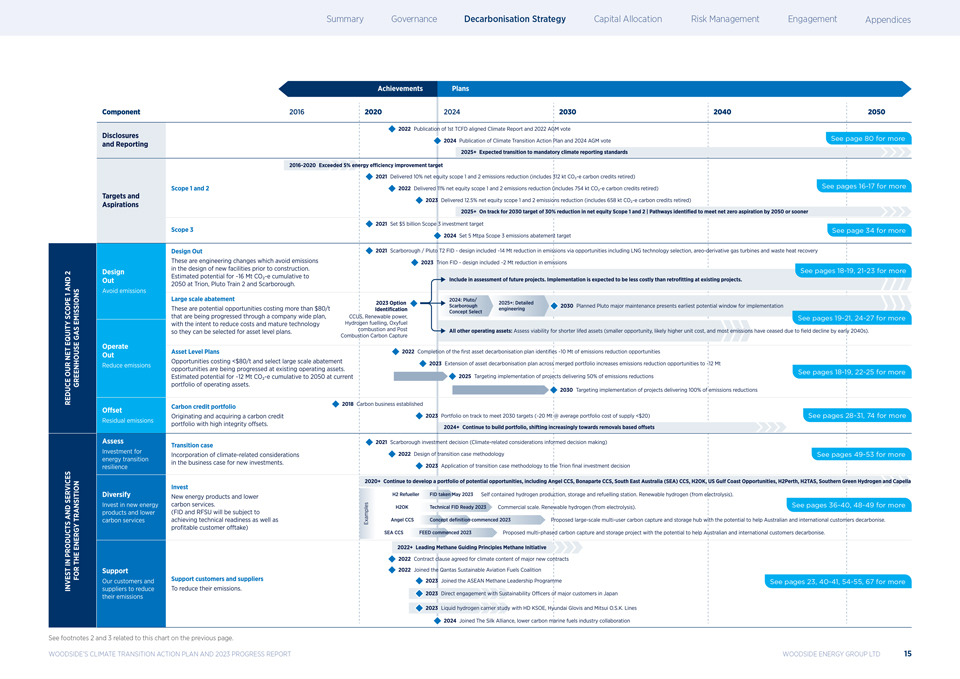

|

请参阅上一页中与此图表相关的脚注2和3。伍德赛德?S气候转型行动计划和2023年进展报告伍德赛德能源集团有限公司15

|

2023 emissions net equity performance Scope 1 and 2 Woodside is targeting a reduction of net equity Scope 1 and 2 greenhouse gas emissions of 15% by 2025 and 30% by 2030, with an aspiration of net zero by 2050 or sooner. The net equity Scope 1 and 2 emissions reduction targets are relative to a starting base of 6.32 million tonnes of CO -e, which is representative of the gross annual average equity 2 Scope 1 and 2 greenhouse gas emissions over 2016-2020. This starting base may be adjusted (up or down) for potential equity changes in producing or sanctioned assets with a ?nal investment decision prior to 2021. The targets mean that net equity Scope 1 and 2 emissions for the 12-month period ending 31 December 2025 are targeted to be 15% lower than the starting base, and that net equity Scope 1 and 2 emissions for the 12-month period ending 31 December 2030 are targeted to be 30% lower than the starting base. OUR PROGRESS TO DATE Woodside has a long standing focus on energy efficiency. Our ?rst formal climate-related target was a 5% energy efficiency target over the period 2016-20. We exceeded it, achieving 8%. Quantification of avoided emissions is inherently uncertain. However, it is possible to provide an estimate by comparison to benchmarks of a comparable portfolio of LNG, conventional shelf and deepwater assets producing 187.2 MMboe (Woodside equity production 2023) with a similar product mix to Woodside. There are a number of potential benchmarks providing estimates of the 2023 global average emissions intensity of oil and gas operations. Two examples are Wood Mackenzie?s Emissions Benchmarking Tool, and the industry average emissions reported in Table 3.1 of IEA?s ?The Oil and Gas Industry in Net Zero Transitions? (November 2023). Comparing Woodside?s Scope 1 and 2 emissions to their average intensity data indicates avoided emissions of 391 kt CO -e and 1,705 kt CO -e respectively. Woodside does not 2 2 independently verify the data behind these estimates.1 Contributions to this were made by the intrinsic characteristics of our oil and gas resources, the design of our facilities, the 2016-2020 energy efficiency target, and the implementation of asset decarbonisation plans from 2021 onwards. OUR 2023 PERFORMANCE 2023 was a strong emissions performance year for our facilities. Despite higher production due to a full year of our merger with BHP?s petroleum business, we advanced our net equity Scope 1 and 2 emissions reduction to 12.5% (compared to 11% in 2022), relative to an adjusted post merger base.2 We also utilised 13% fewer carbon credits than last year, offsetting 96 kt CO -e fewer emissions because of the emissions avoidance 2 and reduction we have achieved. A further indication of the underlying emissions performance at our facilities is that our Scope 1 and 2 gross emissions intensity (a measure of emissions, per unit of production) improved by 3% year on year, and is better than a comparable benchmark.3 We do not expect improvement of gross emissions like this every year: for example, from 2024 the start-up of the Sangomar facility in Senegal (including one-off commissioning emissions) is expected to increase gross emissions for a period. This is why our utilisation of carbon credits as offsets is an important stabiliser, so we are able to reduce our net emissions consistently, notwithstanding operational ?uctuations and while our asset decarbonisation plans build momentum. For more information on the use of carbon credits please see section 3.4. All footnotes related to this page are displayed on the next page. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 16

|

净股本范围1和2减排目标在2025年实现12.5%减排目标:2025年达到15%到2030年达到净零30%2050年或更早净股本范围1和2排放量(Mt CO-e)8 6估计避免排放量1 4抵消排放量伍德赛德净股本排放量 必和必拓2资产排放(合并前)合并实体0起点基数2 20232 2022年范围1和2总排放强度3 35产量30 boe/e二氧化碳排放25公斤20全球平均伍德赛德2023年甲烷排放量估计值0.2石油2023年甲烷排放强度4和气体气候倡议(%)(OGCI)目标远低于0.2%气体0.15上市0.1 SM3/SM3 0.05 0 OGCI行业伍德赛德2023年2022 2023伍德赛德?S净权益范围1和2 2023年温室气体排放量总计5,532 kt CO?-e,比起始基数低12.5%。2总权益范围1和2排放量为6,190 kt CO-e。为了实现这一净结果,658kt CO?-2E的碳信用额度已经报废。2023年,伍德赛德?S总权益范围1温室气体排放的70%来自于燃料燃烧为我们的资产提供动力,22%来自于排气,其中大部分与水库CO?作为液化天然气过程的一部分,8%来自燃烧。在上图中,为实现与2023年的全年可比性,增加了必和必拓石油投资组合在合并前5个月的排放额度。我们2023年的总权益范围1和2的排放量低于可比基准。通过与伍德赛德可比产品组合和产量的基准进行比较,可以 提供避免排放量的估计。有关估算的信息,请参见第16页。1总范围1和2排放强度是在应用补偿之前对我们生产效率的衡量。这是证明伍德赛德在我们的设施中适当优先考虑避免和减少排放的一种方式。伍德赛德的总排放强度低于(高于)液化天然气、常规大陆架和深水资产可比资产组合的全球平均水平,这表明了为避免和减少我们运营的排放而采取的行动的影响,以及我们石油和天然气资源的内在特征。1由于强大的可靠性表现,包括冥王星的减少等因素,2023年我们的总范围1和2的排放强度有所改善。伍德赛德的甲烷排放强度低于(高于)行业(OGCI)目标,并制定了进一步改善和争取接近零的甲烷排放的行动计划。5伍德赛德?S甲烷排放业绩和减少计划见第23页。甲烷排放对伍德赛德?S范围1的排放有贡献,但受到特别关注 ,因为它们对实现全球气候目标具有近期重要性。我们的甲烷强度在2023年有所改善,原因包括减少冥王星的排放和减少生产、储存和卸载(FPSO)设施的排放。1避免排放的量化本质上是不确定的。然而,可以通过与液化天然气、常规大陆架和深水资产组合的基准进行比较来提供估计,这些资产的产量为187.2 Mboe(伍德赛德股权生产2023年),产品组合与伍德赛德类似。有许多潜在的基准提供了对2023年全球石油和天然气作业平均排放强度的估计。基于Wood Mackenzie?S排放基准工具, 估计避免排放量约为391kt CO-e,而根据国际能源署?S?石油和天然气行业净零过渡?表3.1中报告的行业平均排放量?(2023年11月),估计避免的排放量约为1,705千吨CO-e。此图中显示的估算避免排放量代表两个估计值之间的范围。2伍德赛德没有独立核实这些估计背后的数据。2目标和期望是净权益范围1和2温室气体排放量相对于6.32公吨CO-e的起始基数,这代表2016-2020年权益范围1和2温室气体排放的年平均总量,可根据生产或批准资产的潜在权益变化进行调整(上调或下调) 在2021年之前作出最终投资决定。净股本排放量包括利用碳信用作为补偿。3伍德赛德分析,基于2022年和2023年伍德赛德范围1和2相对于液化天然气、常规大陆架和深水资产可比投资组合的排放数据,根据Wood Mackenzie?S排放基准工具中报告的这些主要资源主题的2023年排放强度计算得出。4伍德赛德分析,基于2022年和2023年伍德赛德甲烷排放数据,相对于OGCI平均值和目标。Https://www.ogci.com/action-and-engagement/reducing-methane-emissions/#methane-target.5 OGMP,2023年。?实施计划指南?,第2页https://ogmpartnership.com/wp-content/uploads/2023/02/OGMP-2.0-Implementation-Plan-Guidance_2.pdf.OGMP提供了OGCI上游作业的集体平均目标,作为接近零的例子。排放强度。伍德赛德?S气候转型行动计划和2023年进展报告伍德赛德能源集团有限公司17

|

Net equity Scope 1 and 2: net zero action plan In 2023, we completed the development of decarbonisation plans across our merged portfolio of operated assets including identifying potential large scale opportunities to reduce emissions beyond 2030. DECARBONISATION PLANNING We have three ways to achieve our net equity Scope 1 and 2 emissions reduction targets: avoiding emissions in the way we design facilities; reducing emissions in the way we operate; and both buying and originating carbon credits to utilise as offsets for the remainder. Our priority is to avoid and reduce emissions. All Woodside operated assets and projects must draw up decarbonisation plans to identify the technical opportunities to reduce emissions at the facility, so that the opportunities can be further assessed for engineering and commercial viability. Opportunities that are estimated to cost less than our internal long-term cost of carbon of $80/t CO -e (real terms 2022) are 2 incorporated into asset or project level business plans.1 These opportunities are at varying levels of maturity. To date: Opportunities that we estimate could avoid approximately 16 million tonnes CO -e (cumulatively to 2050) have been incorporated into the 2 design of the Scarborough, Pluto Train 2 and Trion projects;2,3 Around a further 70 opportunities, which we estimate could avoid approximately 12 million tonnes CO -e (cumulatively to 2050) are targeted for completion at our 2 existing facilities by 2030.2,3 We estimate that the opportunities still to be implemented at our existing operating facilities could have a combined capital cost of around $200 million.2,3 This does not include the cost of potential projects which we estimate to cost more than $80/t CO -e. Some of these may also be pursued following review by the Executive 2 Leadership Team ? such as the proposed Woodside Solar project. Other opportunities are pursued in an enterprise large scale abatement plan in order to reduce costs and/or improve maturity, so that they too can be considered for inclusion in asset level business plans. This large scale abatement plan is explained on the next pages. Asset decarbonisation: our progress and plans 2023 ? DELIVERED Completed the development of asset decarbonisation plans across full portfolio of operated assets. Opportunities costing $80/t CO -e: 2 Attention is focused on the assets with the longest remaining lifespan ? primarily the Pluto and Scarborough facilities. The 2024 scope of work at these facilities is to conclude engineering assessment of the technology options in order to select the preferred technology for application. 2025+ ? PLAN Following the selection of large scale abatement options we will undertake further design out engineering to reduce costs and emissions, seeking to advance towards ?FID-ready? status. Subject to FID, a scheduled maintenance shutdown at Pluto in 2030 presents the earliest potential window for implementation. Some projects will be accelerated ahead of this timeline ? e.g. the proposed Woodside Solar project. Woodside continues to progress commercial agreements, including for power transmission, to support the proposed project. 1 Woodside?s assumptions on carbon cost pricing include a long-term carbon price of US$80/tonne of emissions (real terms 2022). Woodside continues to monitor the uncertainty around climate change risks and will revise carbon pricing assumptions accordingly. 2 Indicative only, not guidance. Potential impact of opportunities identified in asset decarbonisation plans assuming all opportunities identified progress to execution, which is not certain and remains subject to further maturity of cost and engineering definition. Greenhouse gas quantities are estimated using engineering judgement by Woodside engineers. Please refer to section 7.6 ?Disclaimer, risks, emissions data and other important information? for important cautionary information relating to forward looking statements. 3 See announcement titled ?Woodside to sell 15.1% Scarborough interest to JERA? (23 February 2024) at woodside.com. Greenhouse gas emissions data including charts and estimates of future abatement plans in this Climate Transition Action Plan have not been updated to reflect changes in Woodside?s equity share of the Scarborough Joint Venture as a consequence of the sale of 15.1% interest to JERA. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 18

|

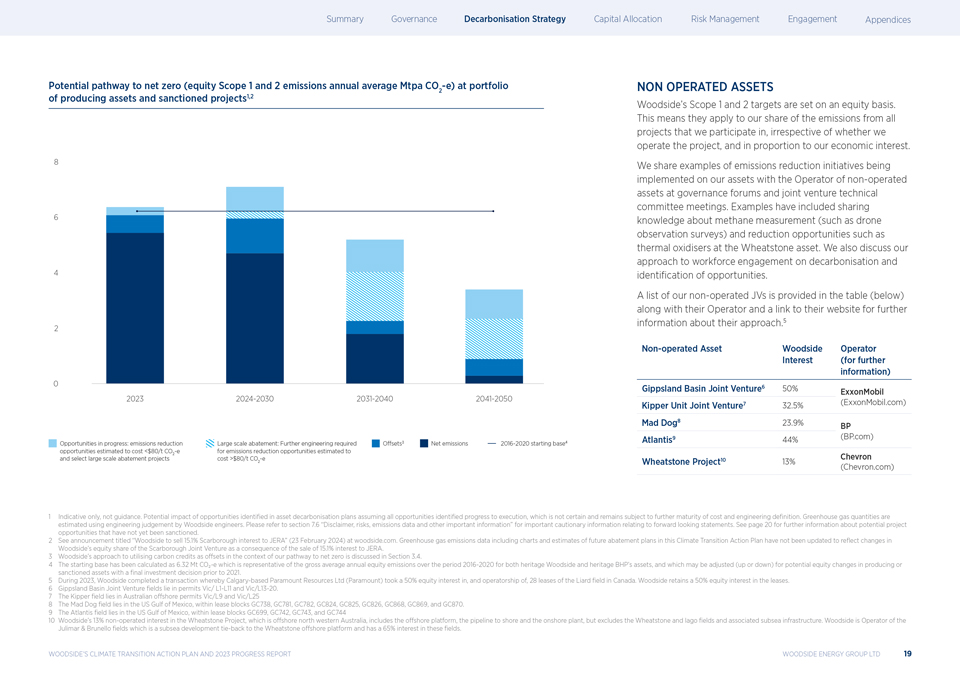

Potential pathway to net zero (equity Scope 1 and 2 emissions annual average Mtpa CO -e) at portfolio 1,2 2 of producing assets and sanctioned projects 8 6 4 2 0 2023 2024-2030 2031-2040 2041-2050 Opportunities in progress: emissions reduction Large scale abatement: Further engineering required Offsets3 Net emissions 2016-2020 starting base4 opportunities estimated to cost $80/t CO -e 2 NON OPERATED ASSETS Woodside?s Scope 1 and 2 targets are set on an equity basis. This means they apply to our share of the emissions from all projects that we participate in, irrespective of whether we operate the project, and in proportion to our economic interest. We share examples of emissions reduction initiatives being implemented on our assets with the Operator of non-operated assets at governance forums and joint venture technical committee meetings. Examples have included sharing knowledge about methane measurement (such as drone observation surveys) and reduction opportunities such as thermal oxidisers at the Wheatstone asset. We also discuss our approach to workforce engagement on decarbonisation and identification of opportunities. A list of our non-operated JVs is provided in the table (below) along with their Operator and a link to their website for further information about their approach.5 Non-operated Asset Woodside Operator Interest (for further information) Gippsland Basin Joint Venture6 50% ExxonMobil Kipper Unit Joint Venture7 32.5% (ExxonMobil.com) Mad Dog8 23.9% BP Atlantis9 44% (BP.com) 10 Chevron Wheatstone Project 13% (Chevron.com) 1 Indicative only, not guidance. Potential impact of opportunities identified in asset decarbonisation plans assuming all opportunities identified progress to execution, which is not certain and remains subject to further maturity of cost and engineering definition. Greenhouse gas quantities are estimated using engineering judgement by Woodside engineers. Please refer to section 7.6 ?Disclaimer, risks, emissions data and other important information? for important cautionary information relating to forward looking statements. See page 20 for further information about potential project opportunities that have not yet been sanctioned. 2 See announcement titled ?Woodside to sell 15.1% Scarborough interest to JERA? (23 February 2024) at woodside.com. Greenhouse gas emissions data including charts and estimates of future abatement plans in this Climate Transition Action Plan have not been updated to reflect changes in Woodside?s equity share of the Scarborough Joint Venture as a consequence of the sale of 15.1% interest to JERA. 3 Woodside?s approach to utilising carbon credits as offsets in the context of our pathway to net zero is discussed in Section 3.4. 4 The starting base has been calculated as 6.32 Mt CO?-e which is representative of the gross average annual equity emissions over the period 2016-2020 for both heritage Woodside and heritage BHP?s assets, and which may be adjusted (up or down) for potential equity changes in producing or sanctioned assets with a final investment decision prior to 2021. 5 During 2023, Woodside completed a transaction whereby Calgary-based Paramount Resources Ltd (Paramount) took a 50% equity interest in, and operatorship of, 28 leases of the Liard ?eld in Canada. Woodside retains a 50% equity interest in the leases. 6 Gippsland Basin Joint Venture ?elds lie in permits Vic/ L1-L11 and Vic/L13-20. 7 The Kipper ?eld lies in Australian offshore permits Vic/L9 and Vic/L25 8 The Mad Dog ?eld lies in the US Gulf of Mexico, within lease blocks GC738, GC781, GC782, GC824, GC825, GC826, GC868, GC869, and GC870. 9 The Atlantis ?eld lies in the US Gulf of Mexico, within lease blocks GC699, GC742, GC743, and GC744 10 Woodside?s 13% non-operated interest in the Wheatstone Project, which is offshore north western Australia, includes the offshore platform, the pipeline to shore and the onshore plant, but excludes the Wheatstone and Iago fields and associated subsea infrastructure. Woodside is Operator of the Julimar & Brunello fields which is a subsea development tie-back to the Wheatstone offshore platform and has a 65% interest in these fields. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 19

|

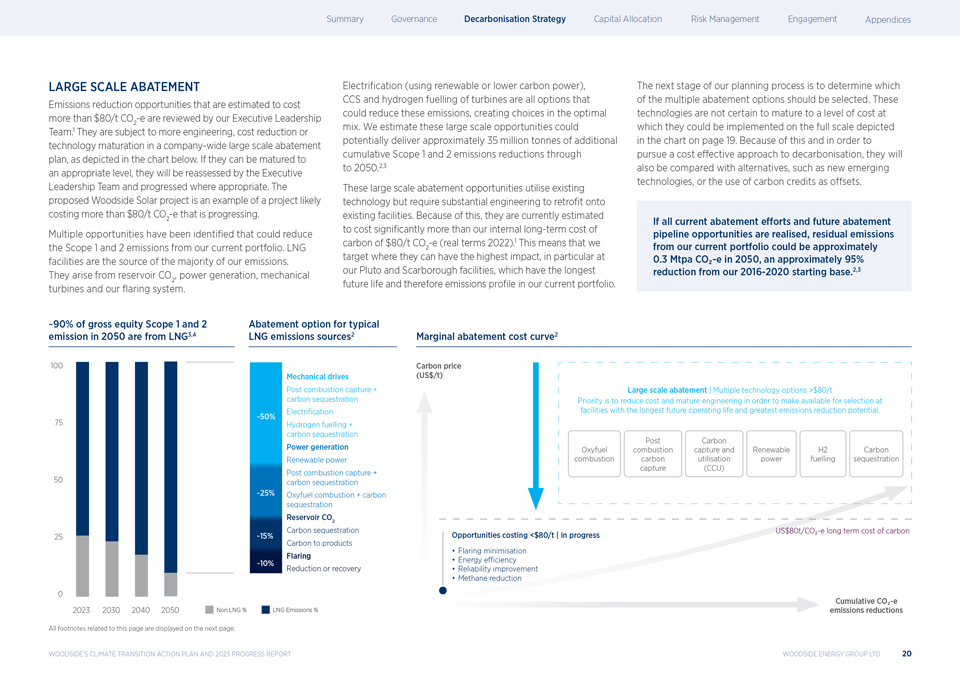

LARGE SCALE ABATEMENT Emissions reduction opportunities that are estimated to cost more than $80/t CO -e are reviewed by our Executive Leadership 2 Team.1 They are subject to more engineering, cost reduction or technology maturation in a company-wide large scale abatement plan, as depicted in the chart below. If they can be matured to an appropriate level, they will be reassessed by the Executive Leadership Team and progressed where appropriate. The proposed Woodside Solar project is an example of a project likely costing more than $80/t CO -e that is progressing. 2 Multiple opportunities have been identi?ed that could reduce the Scope 1 and 2 emissions from our current portfolio. LNG facilities are the source of the majority of our emissions. They arise from reservoir CO , power generation, mechanical turbines and our ?aring system 2 . Electri?cation (using renewable or lower carbon power), CCS and hydrogen fuelling of turbines are all options that could reduce these emissions, creating choices in the optimal mix. We estimate these large scale opportunities could potentially deliver approximately 35 million tonnes of additional cumulative Scope 1 and 2 emissions reductions through to 2050.2,3 These large scale abatement opportunities utilise existing technology but require substantial engineering to retro?t onto existing facilities. Because of this, they are currently estimated to cost signi?cantly more than our internal long-term cost of carbon of $80/t CO -e (real terms 2022).1 This means that we target where they can 2 have the highest impact, in particular at our Pluto and Scarborough facilities, which have the longest future life and therefore emissions pro?le in our current portfolio. The next stage of our planning process is to determine which of the multiple abatement options should be selected. These technologies are not certain to mature to a level of cost at which they could be implemented on the full scale depicted in the chart on page 19. Because of this and in order to pursue a cost effective approach to decarbonisation, they will also be compared with alternatives, such as new emerging technologies, or the use of carbon credits as offsets. If all current abatement efforts and future abatement pipeline opportunities are realised, residual emissions from our current portfolio could be approximately 0.3 Mtpa CO?-e in 2050, an approximately 95% reduction from our 2016-2020 starting base.2,3 ~90% of gross equity Scope 1 and 2 Abatement option for typical emission in 2050 are from LNG3,4 LNG emissions sources2 100 Mechanical drives Post combustion capture + carbon sequestration Electri?cation ~50% 75 Hydrogen fuelling + carbon sequestration Power generation Renewable power 50 Post combustion capture + carbon sequestration ~25% Oxyfuel combustion + carbon sequestration Reservoir CO 2 Carbon sequestration 25 ~15% Carbon to products ~10% Flaring Reduction or recovery 0 2023 2030 2040 2050 Non LNG % LNG Emissions % Marginal abatement cost curve2 Carbon price (US$/t) Large scale abatement | Multiple technology options >$80/t Priority is to reduce cost and mature engineering in order to make available for selection at facilities with the longest future operating life and greatest emissions reduction potential. Post Carbon Oxyfuel combustion capture and Renewable H2 Carbon combustion carbon utilisation power fuelling sequestration capture (CCU) US$80t/CO?-e long term cost of carbon Opportunities costing

|

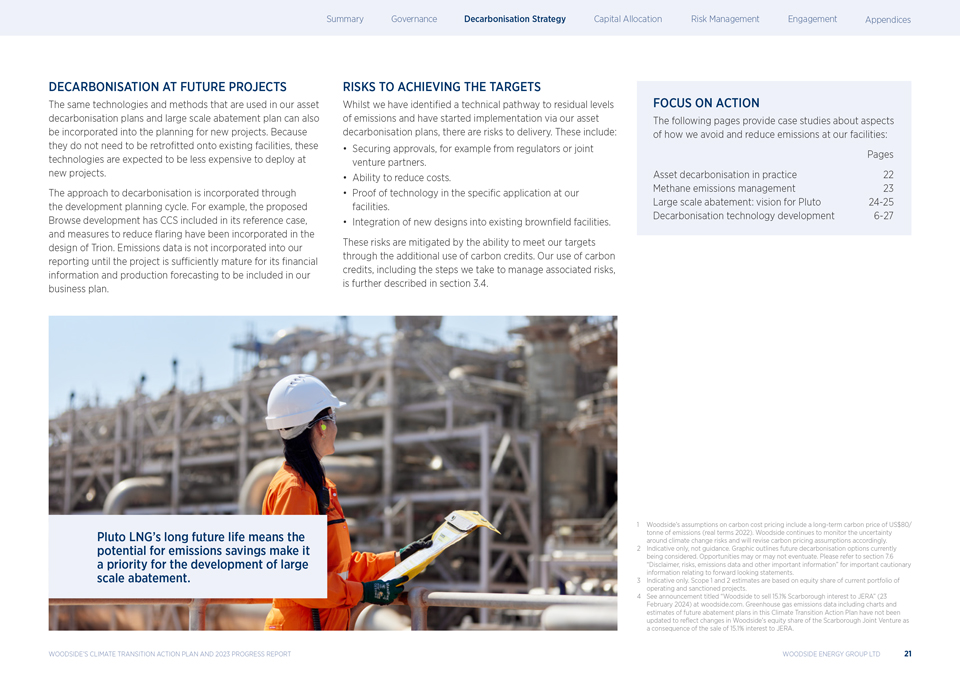

DECARBONISATION AT FUTURE PROJECTS The same technologies and methods that are used in our asset decarbonisation plans and large scale abatement plan can also be incorporated into the planning for new projects. Because they do not need to be retro?tted onto existing facilities, these technologies are expected to be less expensive to deploy at new projects. The approach to decarbonisation is incorporated through the development planning cycle. For example, the proposed Browse development has CCS included in its reference case, and measures to reduce ?aring have been incorporated in the design of Trion. Emissions data is not incorporated into our reporting until the project is sufficiently mature for its ?nancial information and production forecasting to be included in our business plan. RISKS TO ACHIEVING THE TARGETS Whilst we have identi?ed a technical pathway to residual levels of emissions and have started implementation via our asset decarbonisation plans, there are risks to delivery. These include: Securing approvals, for example from regulators or joint venture partners. Ability to reduce costs. Proof of technology in the speci?c application at our facilities. Integration of new designs into existing brown?eld facilities. These risks are mitigated by the ability to meet our targets through the additional use of carbon credits. Our use of carbon credits, including the steps we take to manage associated risks, is further described in section 3.4. FOCUS ON ACTION The following pages provide case studies about aspects of how we avoid and reduce emissions at our facilities: Pages Asset decarbonisation in practice 22 Methane emissions management 23 Large scale abatement: vision for Pluto 24-25 Decarbonisation technology development 6-27 Pluto LNG?s long future life means the potential for emissions savings make it a priority for the development of large scale abatement. 1 Woodside?s assumptions on carbon cost pricing include a long-term carbon price of US$80/ tonne of emissions (real terms 2022). Woodside continues to monitor the uncertainty around climate change risks and will revise carbon pricing assumptions accordingly. 2 Indicative only, not guidance. Graphic outlines future decarbonisation options currently being considered. Opportunities may or may not eventuate. Please refer to section 7.6 ?Disclaimer, risks, emissions data and other important information? for important cautionary information relating to forward looking statements. 3 Indicative only. Scope 1 and 2 estimates are based on equity share of current portfolio of operating and sanctioned projects. 4 See announcement titled ?Woodside to sell 15.1% Scarborough interest to JERA? (23 February 2024) at woodside.com. Greenhouse gas emissions data including charts and estimates of future abatement plans in this Climate Transition Action Plan have not been updated to reflect changes in Woodside?s equity share of the Scarborough Joint Venture as a consequence of the sale of 15.1% interest to JERA. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 21

|

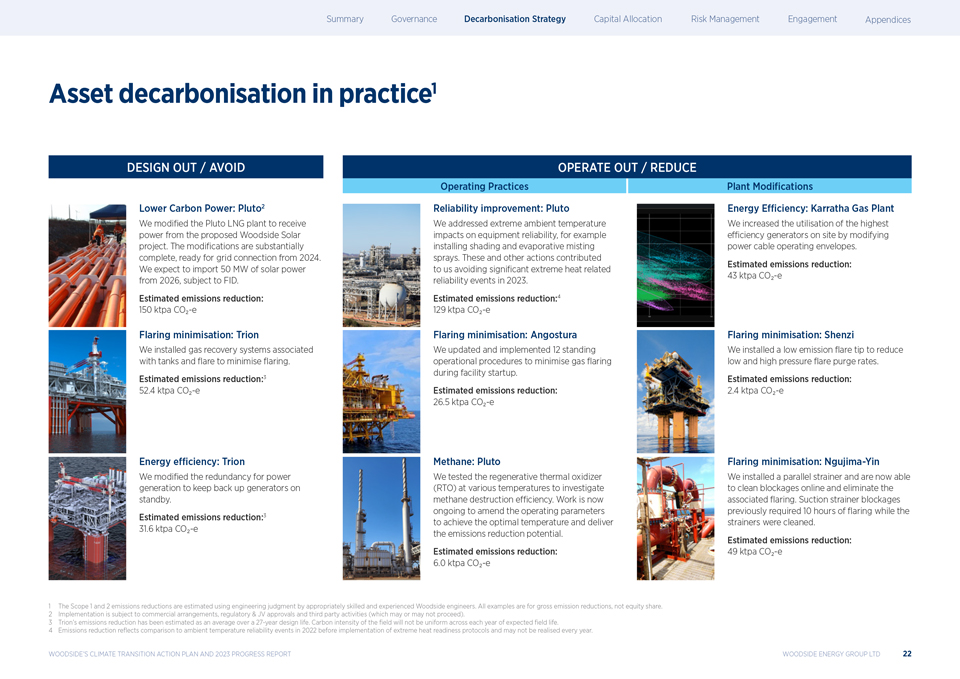

Asset decarbonisation in practice1 DESIGN OUT / AVOID Lower Carbon Power: Pluto2 We modi?ed the Pluto LNG plant to receive power from the proposed Woodside Solar project. The modi?cations are substantially complete, ready for grid connection from 2024. We expect to import 50 MW of solar power from 2026, subject to FID. Estimated emissions reduction: 150 ktpa CO?-e Flaring minimisation: Trion We installed gas recovery systems associated with tanks and ?are to minimise ?aring. Estimated emissions reduction:3 52.4 ktpa CO?-e Energy efficiency: Trion We modi?ed the redundancy for power generation to keep back up generators on standby. Estimated emissions reduction:3 31.6 ktpa CO?-e OPERATE OUT / REDUCE Operating Practices Plant Modi?cations Reliability improvement: Pluto Energy Efficiency: Karratha Gas Plant We addressed extreme ambient temperature We increased the utilisation of the highest impacts on equipment reliability, for example efficiency generators on site by modifying installing shading and evaporative misting power cable operating envelopes. sprays. These and other actions contributed Estimated emissions reduction: to us avoiding signi?cant extreme heat related 43 ktpa CO?-e reliability events in 2023. Estimated emissions reduction:4 129 ktpa CO?-e Flaring minimisation: Angostura Flaring minimisation: Shenzi We updated and implemented 12 standing We installed a low emission ?are tip to reduce operational procedures to minimise gas ?aring low and high pressure ?are purge rates. during facility startup. Estimated emissions reduction: Estimated emissions reduction: 2.4 ktpa CO?-e 26.5 ktpa CO?-e Methane: Pluto Flaring minimisation: Ngujima-Yin We tested the regenerative thermal oxidizer We installed a parallel strainer and are now able (RTO) at various temperatures to investigate to clean blockages online and eliminate the methane destruction efficiency. Work is now associated ?aring. Suction strainer blockages ongoing to amend the operating parameters previously required 10 hours of ?aring while the to achieve the optimal temperature and deliver strainers were cleaned. the emissions reduction potential. Estimated emissions reduction: Estimated emissions reduction: 49 ktpa CO?-e 6.0 ktpa CO?-e 1 The Scope 1 and 2 emissions reductions are estimated using engineering judgment by appropriately skilled and experienced Woodside engineers. All examples are for gross emission reductions, not equity share. 2 Implementation is subject to commercial arrangements, regulatory & JV approvals and third party activities (which may or may not proceed). 3 Trion?s emissions reduction has been estimated as an average over a 27-year design life. Carbon intensity of the field will not be uniform across each year of expected field life. 4 Emissions reduction re?ects comparison to ambient temperature reliability events in 2022 before implementation of extreme heat readiness protocols and may not be realised every year. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 22

|

Methane emissions management In January 2024, Woodside joined the UN Environment Programme?s (UNEP) flagship reporting and mitigation program, the Oil and Gas Methane Partnership (OGMP 2.0). Methane management plan: 2023 progress Methane emissions management is an important part of global efforts to limit climate change because it has a higher global warming potential than carbon dioxide, especially in the near term, and is estimated to have made the second largest contribution to human-induced climate change after carbon dioxide. Woodside?s reported methane emissions are around 0.1% of production by volume. This calculation is supported by our improving ability to directly monitor and measure methane at our facilities. It is lower than the Oil and Gas Climate Initiative (OGCI) 2025 target of below 0.2%.1 It re?ects our long standing focus on reducing methane leaks, which if they occur at sufficient volume would be a loss to our production and a potential safety hazard. We continue to strive for further reductions through our methane plan (2023 progress against four pillars of the plan is shown on the right). When we assess emissions reduction opportunities, we multiply our internal long-term cost of carbon of $80/t CO -e (real terms 2022) by 84 (an effective price for 2 methane of $6,720/t) to align with the higher global warming potential of methane in the near term. MEASURE We are improving our ability to measure methane emissions. In 2023 we: Built and maintained a database of methane emissions sources, con?rmed with selected site measurements across all operated assets. Trialled a spectrometric aerial methane measurement technique at onshore facilities. Conducted methane point source detection and quanti?cation trials from two satellite vendors to test capability. Completed strategic drone surveys trialling the use of CO /CH ratios for combustion assessment 2 4 . Piloted several fugitive detection tools including quanti?ed optical gas imaging. Partnered with the University of Western Australia to prototype novel methane sensors. REDUCE We are taking action to reduce methane emissions to near-zero at our operated assets by prioritising the mitigation of our most material sources.2 In 2023 we took action to reduce methane emissions by 2.0 ktpa including:3 Performance optimisation of wet gas seals on two boil off gas (BOG) compressors, estimated saving of 1.5 ktpa of methane. Recti?cation of a trunkline fugitive leak at the Karratha Gas Plant onshore terminal, estimated saving of 0.3 ktpa of methane. Automation of a manual venting procedure on three acid gas removal units, estimated saving of 0.2 ktpa of methane. REPORT We aim to report our methane emissions data accurately and transparently. In 2023 we: Conducted surveys which support our calculation that our methane emissions are around 0.1% (of production by volume), consistent with historical aerial (top down) and point source (bottom up) site measurements. Engaged with Australia?s Climate Change Authority to support improvement of methane reporting regulations In 2024, we joined the Oil and Gas Methane Partnership (OGMP) 2.0 to support transparent methane emissions reporting. LEAD We support the adoption of methane best practice across industry through leadership, advocacy and collaboration. In 2023 we: Led the Methane Guiding Principles ?Global Midstream Initiative?. Joined the ASEAN Methane Leadership Program to share methane reduction learnings. Sponsored the ?rst technical workshop of the Australian Energy Producers methane taskforce. Collaborated with researchers conducting science studies as part of UNEP?s International Methane Emissions Observatory?s efforts to fill knowledge gaps in methane emissions. Shared knowledge on methane management through a presentation and journal article publication at the 2023 Australian Energy Producers conference. Presented and participated in panels at the Global Methane Summit and International Gas Union conference. 1 OGCI, 2024. https://www.ogci.com/action-and-engagement/reducing-methane-emissions/#methane-target. 2 OGMP, 2023. ?Implementation Plan Guidance?, p. 2 https://ogmpartnership.com/wp-content/uploads/2023/02/OGMP-2.0-Implementation-Plan-Guidance_2.pdf. OGMP provides the OGCI collective average target for upstream operations as an example of ?near zero? emissions intensity. 3 The methane emissions reductions are estimated using engineering judgment by appropriately skilled and experienced Woodside engineers. All examples are for gross emission reductions, not equity share. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 23

|

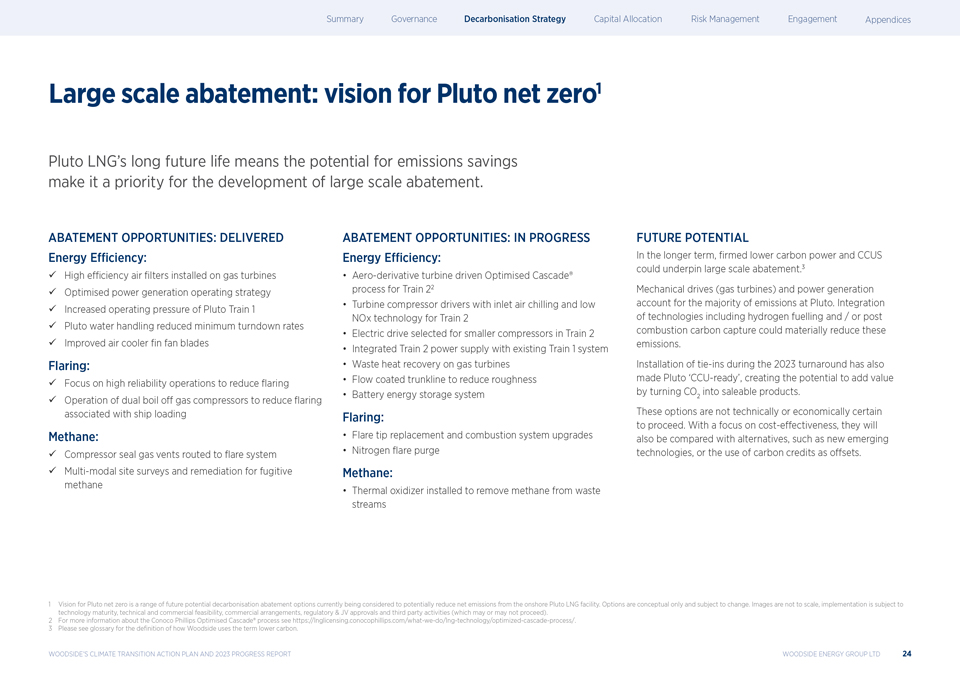

大规模减排:冥王星净零1冥王星液化天然气的愿景?其长期的未来寿命意味着减排的潜力使其成为发展大规模减排的优先事项。减少机会:提供的能源效率:?高效空气?安装在燃气轮机上的? 优化?发电运营策略?冥王星列车1号运行压力增加?冥王星水处理降低了最低夜床率?改进的空气冷却器?n风扇叶片扩口:?专注于高可靠性操作以减少?aring ?运行双蒸发气体压缩机以减少??与装载甲烷有关的船舶:?压缩机密封排气口路由至?系统?多模式现场调查和对散逸性甲烷减排的补救机会:正在 进展中的能源效率:用于22列涡轮压缩机驱动器的航空衍生涡轮机驱动优化级联工艺,具有入口空气冷却和低NOx?第2列的技术为第2列的小型压缩机选择电驱动器与现有的第1列系统集成的第2列电源供应燃气涡轮机废热回收流动涂层干线减少粗糙度电池储能系统燃烧:火炬尖端更换和燃烧系统升级氮气? 清除甲烷:安装了热氧化器以去除废物流中的甲烷未来潜力从长远来看,?更低碳发电和CCUS可以支持大规模减排。3机械驱动(燃气轮机)和发电 占冥王星排放的大部分。包括氢燃料和/或燃烧后碳捕集在内的技术的整合可以大大减少这些排放。在2023年的转折期间安装连接也使 冥王星?CCU准备好了吗?通过将一氧化碳转化为可销售产品,创造附加价值的潜力。2这些选择在技术上或经济上都不一定会进行。在注重成本效益的情况下,它们还将与替代品进行比较, 例如新兴技术,或使用碳信用额作为抵消。1冥王星净零排放愿景是目前正在考虑的一系列未来潜在脱碳减排方案,以潜在地减少陆上 冥王星液化天然气设施的净排放。备选方案只是概念性的,可能会有所改变。图像不按比例绘制,实施取决于技术成熟度、技术和商业可行性、商业安排、监管和合资企业批准以及 第三方活动(可能会进行也可能不会进行)。2有关康菲石油优化级联工艺的更多信息,请访问www.example.com。3请参见术语表 以了解de?伍德赛德如何使用低碳一词。伍德赛德?2023年全球气候变迁行动计划与进展报告Woodside Energy Group Limited 24

|

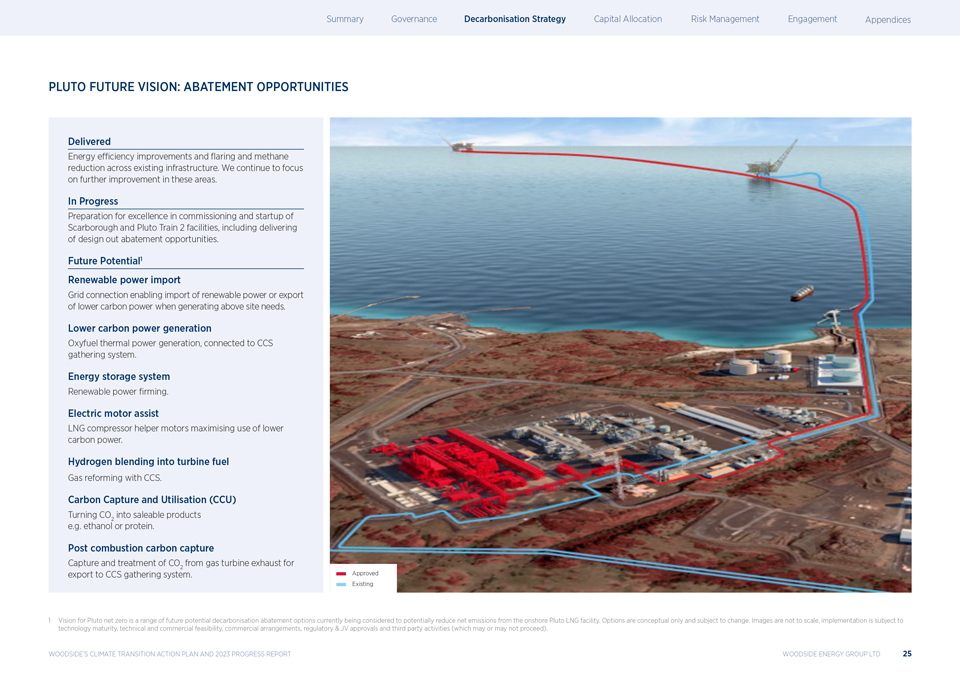

Pluto未来愿景:减少机遇 实现能源效率的提高和?在现有基础设施中减少甲烷和甲烷。我们将继续致力于进一步改善这些领域。正在进行中,为Scarborough 和Pluto Train 2设施的卓越调试和启动做好准备,包括提供设计出的减排机会。未来潜力1可再生能源输入电网连接,在发电厂以上需求时,可输入可再生能源或输出低碳电力。 低碳发电含氧燃料热发电,连接CCS集输系统。储能系统可再生能源?rming。电动机辅助LNG压缩机辅助电机,最大限度地利用低碳能源。氢气 混合到涡轮机燃料中使用CCS进行气体重整。碳捕集和利用(CCU)将一氧化碳转化为可销售的产品,如乙醇2或蛋白质。燃烧后碳捕集从燃气轮机排气中捕集和处理CO,以输出至CCS 集气系统2. 1冥王星净零愿景是目前正在考虑的一系列未来潜在脱碳减排方案,以潜在地减少陆上冥王星液化天然气设施的净排放。选项仅为概念性的, 可能会发生变化。图像不按比例绘制,实施取决于技术成熟度、技术和商业可行性、商业安排、监管和合资企业批准以及第三方活动(可能会进行也可能不会进行)。 伍德赛德?2023年全球气候变迁行动计划与进展报告Woodside Energy Group Limited 25

|

脱碳技术开发Woodside看到了一条潜在的途径,通过利用已在其他地方成功部署的现有成熟技术,到2050年或更早实现我们的净零排放目标。但是复古的价格贵吗?我们的工程 重点是降低成本。新技术也在不断涌现,它们有可能在不同的时间框架内取代我们当前计划中的机会。Woodside正在努力使技术成熟,并推动其成本的逐步变化, 使其成为可行的选项,可以在不同的时间范围内进行部署。与Heliogen合作开发可再生能源技术,以推进更长时间的可再生能源。其中包括加州的商业规模示范工厂 Capella项目。混合燃料H2燃烧我们正在与贝克休斯合作,旨在鉴定一种在燃气轮机中使用氢气的技术和途径,而无需昂贵的基础设施更换。 氧燃烧技术我们正在努力?有几家公司要审查开发发电技术,通过燃烧天然气和2个接近纯氧,实现高浓度CO 捕集,可实现90%以上的CO捕集效率。2监测甲烷监测我们正在与供应商合作,测试一系列技术,以准确测量各种来源的甲烷排放量,如?排放,排放和逃逸排放。我们的目标是使用自上而下和自下而上的方法来检测和减少这些排放,包括无人机、机器人,?固定的设备,手持设备,卫星图像。伍德赛德?2023年全球气候变迁行动计划与进展报告Woodside Energy Group Limited 26

|

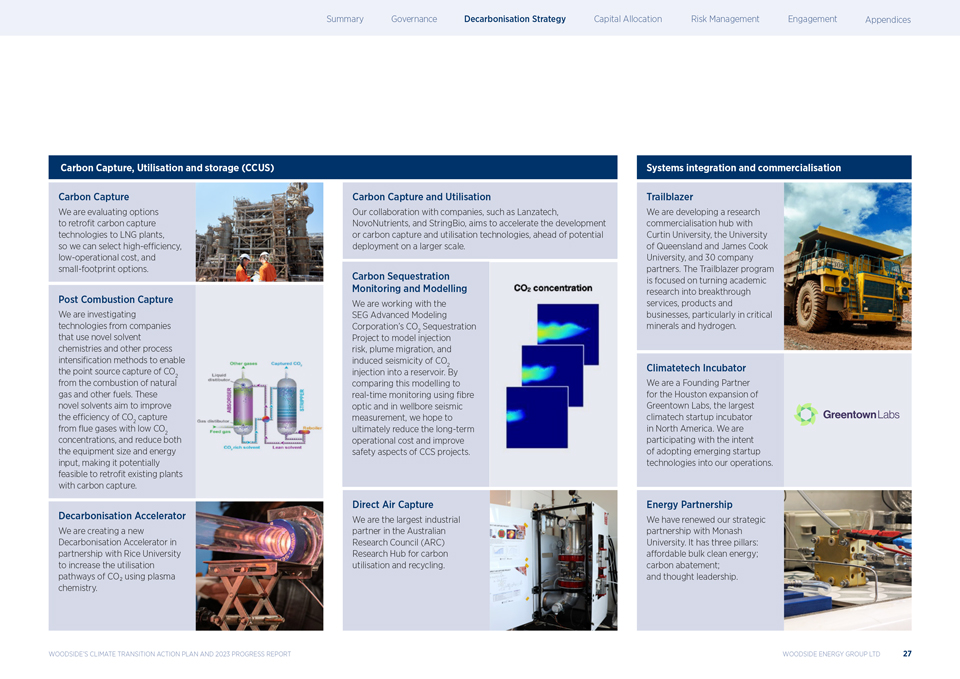

Carbon Capture, Utilisation and storage (CCUS) Carbon Capture We are evaluating options to retro?t carbon capture technologies to LNG plants, so we can select high-efficiency, low-operational cost, and small-footprint options. Post Combustion Capture We are investigating technologies from companies that use novel solvent chemistries and other process intensi?cation methods to enable the point source capture of CO from the combustion of natural2 gas and other fuels. These novel solvents aim to improve the efficiency of CO capture from ?ue gases with2 low CO concentrations, and reduce both 2 the equipment size and energy input, making it potentially feasible to retro?t existing plants with carbon capture. Decarbonisation Accelerator We are creating a new Decarbonisation Accelerator in partnership with Rice University to increase the utilisation pathways of CO? using plasma chemistry. Carbon Capture and Utilisation Our collaboration with companies, such as Lanzatech, NovoNutrients, and StringBio, aims to accelerate the development or carbon capture and utilisation technologies, ahead of potential deployment on a larger scale. Carbon Sequestration Monitoring and Modelling We are working with the SEG Advanced Modeling Corporation?s CO Sequestration Project to model 2 injection risk, plume migration, and induced seismicity of CO injection into a reservoir. 2 By comparing this modelling to real-time monitoring using ?bre optic and in wellbore seismic measurement, we hope to ultimately reduce the long-term operational cost and improve safety aspects of CCS projects. Direct Air Capture We are the largest industrial partner in the Australian Research Council (ARC) Research Hub for carbon utilisation and recycling. Systems integration and commercialisation Trailblazer We are developing a research commercialisation hub with Curtin University, the University of Queensland and James Cook University, and 30 company partners. The Trailblazer program is focused on turning academic research into breakthrough services, products and businesses, particularly in critical minerals and hydrogen. Climatetech Incubator We are a Founding Partner for the Houston expansion of Greentown Labs, the largest climatech startup incubator in North America. We are participating with the intent of adopting emerging startup technologies into our operations. Energy Partnership We have renewed our strategic partnership with Monash University. It has three pillars: affordable bulk clean energy; carbon abatement; and thought leadership. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 27

|

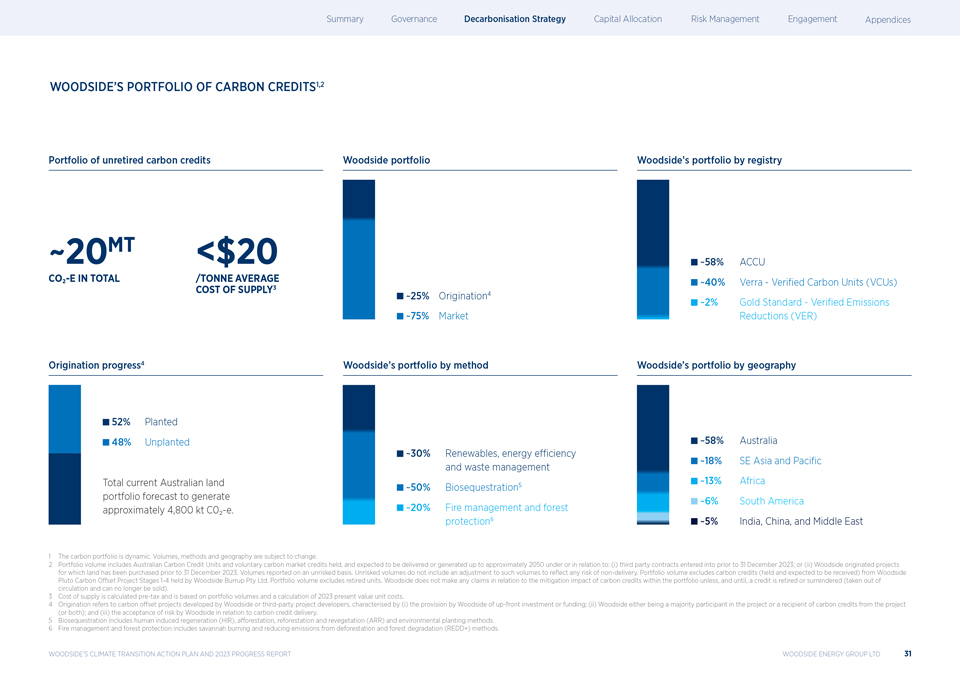

Carbon credits Investing in carbon credits contributes to preserving the world?s carbon budget, by accelerating emissions reduction, avoidance and removal activities that would not otherwise have taken place. ? Tree planting as part of the Woodside Native Reforestation Project. ROLE OF CARBON CREDITS IN OUR DECARBONISATION PLANS Woodside utilises certified carbon credits to offset equity Scope 1 and 2 emissions that are above our targets in a given year after design out and operate out measures have been taken. The availability of carbon credits to offset emissions is important because: gross emissions can fluctuate, for example, due to portfolio change or for operational reasons, asset decarbonisation plans can take time to implement, especially where they are large scale or complex engineering projects, and some decarbonisation technologies may prove too expensive to implement efficiently. The ability to utilise carbon credits means that we can maintain our target trajectory and continue to reduce our net equity Scope 1 and 2 greenhouse gas emissions, despite these variable factors. Like our asset decarbonisation plans, our portfolio of carbon credits enables our base business to manage the price risk associated with regulations and our corporate net equity Scope 1 and 2 emissions targets. Carbon credits are available now and can be used in the short and medium term for emissions that are otherwise not technically or economically viable to avoid or reduce.1 OUR PORTFOLIO APPROACH We established a Carbon Business in 2018 in order to develop a portfolio of carbon credits and our skills and expertise in managing carbon credit integrity. Since then we have invested more than $150 million, with approximately one third of that spend focused on the origination of our own projects, and the remainder on purchase of credits.2,3,4,5 Today, Woodside manages a portfolio of more than 20 million carbon credits, which it has acquired with an average cost of supply of less than $20/t.3,5 Over time we are increasing our focus on project origination as this enables us to better manage the cost and integrity of our carbon credits. In 2023, Woodside planted approximately 2.7 million mixed biodiverse seedlings in Western Australia as part of our Native Reforestation Project across approximately 4,700 ha of land at Woodside owned properties.6 In Senegal, Woodside is funding the restoration of up to 7,000 hectares of mangroves in the Sine Saloum and Casamance regions. Woodside is expected to receive up to 1.4 million carbon credits from this project over 30 years. A wide range of activities can generate carbon credits. These activities can be categorised into avoidance/reduction (e.g. land?ll gas capture or renewable energy) or removal (e.g. reforestation) activities. *All footnotes related to this page are displayed on the next page. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 28

|

虽然在近期至中期内,避免和减少信贷仍将占投资组合的很大份额,但我们计划随着时间的推移增加清除信贷的比例,以支持我们的净零目标。我们目前拥有并将目标维持一个由50%基于自然的 清除信用(例如生物封存)组成的投资组合。我们也认识到,长期存储将变得越来越重要。我们认识到,使用碳信用额作为抵消受到了一些团体的批评,如果这些批评得不到回应, 可能会对其持续的可接受性构成风险。我们相信,这些风险可以通过我们计划评估诚信和管理多样化信贷组合的方式来减轻。Woodside订阅新兴的独立碳信用评级 平台,评估碳信用的完整性。我们亦会在制定方法时监察独立机构制定的诚信评估框架及标准的演变。我们的方法受到当前和新兴的 外部框架的影响,如自愿碳市场诚信委员会(ICVCM)?气候变化投资者组织的核心碳原则?s(IGCC)?7,8,9在我们的设施中优先避免和减少排放我们的首要任务是避免和减少排放。例如,我们寻求机会,在设计和运营我们的资产时,当使用内部长期碳成本(目前为80美元/吨二氧化碳当量(2022年实际价值)进行评估时,这些资产在经济上是可行的。这超过了目前碳信用额的市场价格2。在清洁能源监管机构于二零二三年十二月公布的季度市场报告中,澳大利亚碳信用单位(ACCU)的通用现货价格约为31. 25澳元(约21美元)。 虽然我们优先考虑避免和减少设施的排放,但碳排放额度仍然是实现我们公司目标和监管需求的重要选择,直至2030年(如果需要)。到目前为止,我们已经获得了到2030年预期ACCU需求的90%以上,并制定了一个规划。否则在技术上或经济上都不可行,以避免或减少?我们指的是使用 碳信用额来处理在之后仍然高于我们的目标的排放量?designout?然后呢?手术了吗我们的内部碳价格为80美元/吨CO—E(2022年实际价格)。 22投资金额为于二零二三年十二月三十一日之前就市场购买碳信用额及Woodside开发的碳来源项目产生的税前开支。分配至范围1和范围2排放的碳信用额投资不会有助于实现我们的范围3投资目标。本报告中引用的1.5亿美元碳信用额度投资未归因于本报告中3.35亿美元的范围3投资目标更新。3投资组合数量不包括碳信用额(持有并预期收到)来自Woodside Pluto碳抵消 由Woodside Burght Pty Ltd.持有的项目阶段1—4。4起源指Woodside或第三方项目开发商开发的碳抵消项目,其特征在于(i)Woodside提供前期投资或资金;(ii) Woodside是项目的多数参与者或项目的碳信用额接受者(或两者兼有);及(iii)Woodside接受与碳信用额交付有关的风险。5碳投资组合是动态的。方法、 和地理位置可能会发生变化。投资组合数量包括持有的澳大利亚碳信用单位和自愿碳市场信用,并预计将根据或与以下各项相关交付或产生至2050年:(i)2023年12月31日之前订立的第三方合同;或(ii)2023年12月31日之前购买土地的伍德赛德起源项目。该公司在没有风险的基础上报告了。无风险量不包括对此类量的调整,以重新?排除 任何无法交付的风险。投资组合数量不包括已退休的单位。Woodside不就投资组合中碳信用额度的缓解影响提出任何索赔,除非且直到某个信用额度被收回或放弃(从 循环中取出,并且不能再出售)。6该项目有可能在25年内封存约2,000千吨CO?-E。?核心碳原则?,https://icvcm.org/the-core-carbon-principles/.8 IGCC,2022年。?企业环境转型计划:投资者预期指南?, https://igcc.org.au/wp-content/uploads/2022/03/IGCC-corporate-transition-plan-investor-expectations.pdf.牛津大学,2020年。?《牛津净零对齐碳补偿原则》, https://www.smithschool.ox.ac.uk/sites/default/files/2022-01/Oxford-Offsetting-Principles-2020.pdf.2023年,10 CER。?十二月?碳市场季度报告?2023年9月季度?, https://www.cleanenergyregulator.gov.au/Infohub/Markets/quarterly-carbon-market-reports.11卷包括Woodside Burrup Pty Ltd.持有的Woodside Pluto碳抵消项目阶段1-4的碳信用(持有并预计将收到)的伍德赛德股权。12参见伍德赛德将向jera出售15.1%斯卡伯勒权益?(2024年2月23日)的公告。本气候过渡行动计划中的温室气体排放数据(包括图表和未来减排计划的估计)尚未更新,以反映由于向JERA出售15.1%的权益而导致伍德赛德?S在斯卡伯勒合资企业中的股权份额的变化。

|

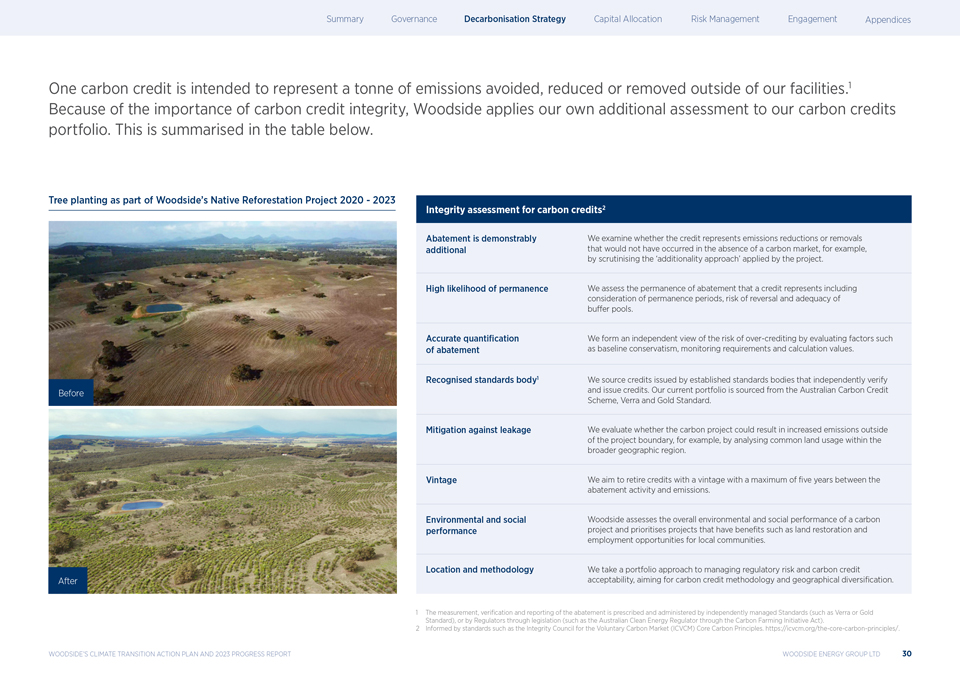

One carbon credit is intended to represent a tonne of emissions avoided, reduced or removed outside of our facilities.1 Because of the importance of carbon credit integrity, Woodside applies our own additional assessment to our carbon credits portfolio. This is summarised in the table below. Tree planting as part of Woodside?s Native Reforestation Project 2020—2023 Integrity assessment for carbon credits2 Abatement is demonstrably We examine whether the credit represents emissions reductions or removals additional that would not have occurred in the absence of a carbon market, for example, by scrutinising the ?additionality approach? applied by the project. High likelihood of permanence We assess the permanence of abatement that a credit represents including consideration of permanence periods, risk of reversal and adequacy of buffer pools. Accurate quanti?cation We form an independent view of the risk of over-crediting by evaluating factors such of abatement as baseline conservatism, monitoring requirements and calculation values. Recognised standards body1 We source credits issued by established standards bodies that independently verify and issue credits. Our current portfolio is sourced from the Australian Carbon Credit Scheme, Verra and Gold Standard. Mitigation against leakage We evaluate whether the carbon project could result in increased emissions outside of the project boundary, for example, by analysing common land usage within the broader geographic region. Vintage We aim to retire credits with a vintage with a maximum of ?ve years between the abatement activity and emissions. Environmental and social Woodside assesses the overall environmental and social performance of a carbon performance project and prioritises projects that have bene?ts such as land restoration and employment opportunities for local communities. Location and methodology We take a portfolio approach to managing regulatory risk and carbon credit acceptability, aiming for carbon credit methodology and geographical diversi?cation. 1 The measurement, veri?cation and reporting of the abatement is prescribed and administered by independently managed Standards (such as Verra or Gold Standard), or by Regulators through legislation (such as the Australian Clean Energy Regulator through the Carbon Farming Initiative Act). 2 Informed by standards such as the Integrity Council for the Voluntary Carbon Market (ICVCM) Core Carbon Principles. https://icvcm.org/the-core-carbon-principles/. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 30

|

伍德赛德?碳信用投资组合1,2未退休碳信用投资组合 伍德赛德投资组合?s投资组合按注册表~20MT

|

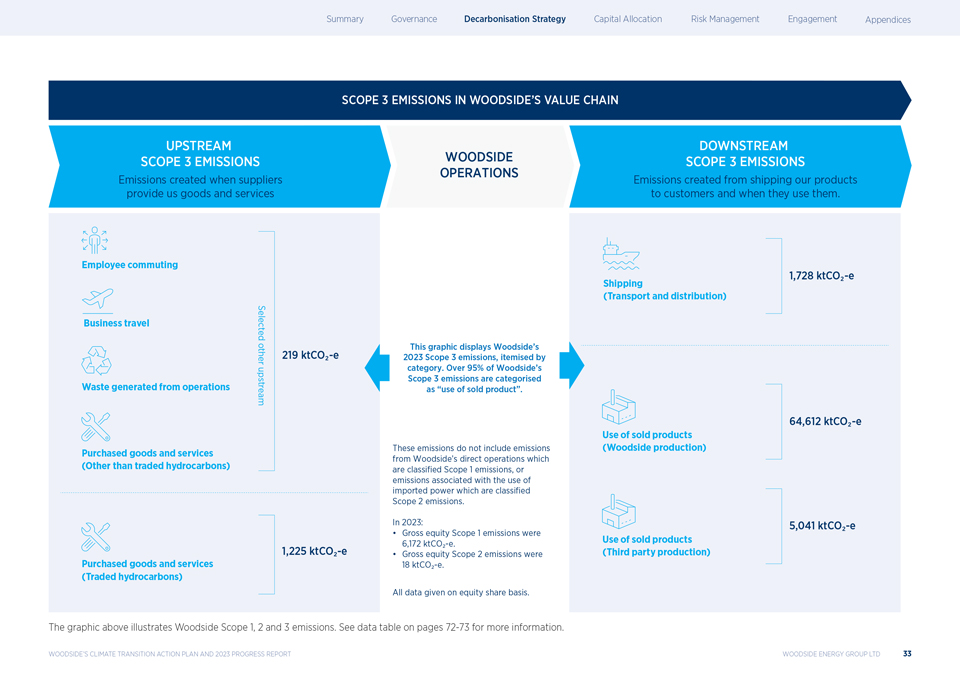

3.5范围3排放范围3排放对 Woodside很重要,因为它们是我们客户和供应商的范围1和2排放。范围3的排放发生在我们的价值链内,但在我们的运营之外。例如,供应商的排放量?在向我们提供商品和 服务时,或从客户那里进行的活动?当他们使用我们的产品时。随着我们的客户脱碳,他们可能无法再以同样的方式或 同样的成本使用我们的产品(供应商可能无法向我们交付产品)。因此,范围3排放是一个指南,如何我们的客户?S和供应商?我们的脱碳可能会影响我们的业务。衡量范围3排放风险的一个指标是我们产品组合的生命周期强度(范围1、2和3排放,我们生产和销售的每单位(兆焦耳)能源)。伍德赛德?由于我们的投资组合对天然气的权重,其强度低于石油和天然气行业的平均水平。Woodside计划通过以下方式管理其对范围3排放的敞口 :评估我们的投资对能源转型的弹性。我们的方法将在第42页开始的资本分配一节中作更全面的介绍。通过投资于新能源产品和低碳 服务,使我们的产品组合多样化,以避免或减少客户排放。支持我们的客户和供应商减少排放,并达到范围1或2的目标。促进一致的全球排放量计量和报告。气体用于各种 高温工业过程,如铁和铝生产。范围1、2、3生命周期强度1 Woodside?由于与必和必拓合并整整一年的影响,2023年的强度有所增加?美国的石油业务, 石油相对较多,但仍低于(好于)行业平均水平。伍德赛德?气候过渡行动计划和2023年进展报告1伍德赛德分析,基于伍德赛德范围1、2和3的2023年排放数据,相对于过渡 路径倡议石油和天然气部门平均评估日期2023年6月30日。https://www. transitionpathwayinitiation.org.伍德赛德能源集团有限公司32

|

上游范围3排放 供应商向我们提供货物和服务时产生的排放木材作业下游范围3排放将我们的产品运送给客户以及客户使用时产生的排放。员工通勤商务差旅运营产生的废物采购 货物和服务(贸易碳氢化合物除外)(贸易碳氢化合物)选定的其他上游(运输和分销)1,728 ktCO_e销售产品的使用(Woodside生产) 64,612 ktCO_—e销售产品的使用(第三方生产)5,041 ktCO_—e此图显示Woodside?2023年范围3排放,按类别分列。超过95%的伍德赛德?s范围3的排放被分类为?销售产品的使用?这些 排放不包括伍德赛德的排放?分类为范围1排放的直接操作,或分类为范围2排放的与使用进口电力有关的排放。2023年:总权益范围1排放量为 6,172 ktCO—e。总权益范围2排放量为18吨二氧化碳当量。所有数据均以权益份额为基础。上图显示了Woodside范围1、2和3的排放。更多信息见第72—73页的数据表。伍德赛德?气候变迁 行动计划与2023年进展报告伍德赛德能源集团有限公司33

|

3.6 Scope 3 targets In 2023, we continued to review our approach to Scope 3 targets in response to investor feedback and have decided to supplement our existing investment target with a new complementary emissions abatement target. Our Scope 3 approach includes the introduction of new products and services into our portfolio, like hydrogen and CCUS. These products and services can help our customers avoid or reduce their Scope 1 or 2 emissions and therefore reduce the life cycle (Scopes 1, 2 and 3) emissions intensity of our portfolio. For example, products like hydrogen have the potential to increase our sales of energy, without materially adding to the Scope 3 emissions from their use. Customers of CCUS have the potential to reduce their Scope 1 emissions, adding negative emissions to our value chain. The investment target tracks our work to develop these projects and bring them to market. The emissions abatement target will track the potential impact of these projects on customer emissions. SCOPE 3 INVESTMENT TARGET1 In 2021, Woodside set a Scope 3 investment target ? aiming to invest $5 billion in new energy products and lower carbon services by 2030.2 At the end of 2023, we have cumulatively spent more than $335 million towards this target. 2023 expenditure increased over 135% compared to 2022. We expect expenditure to continue to ramp up towards the back end of the target period, subject to markets developing, because most project expenditure occurs in the construction phase. SCOPE 3 EMISSIONS ABATEMENT TARGET1 Woodside has now also set a related Scope 3 emissions abatement target, to indicate the potential abatement impact of these products and services upon customer Scope 1 or 2 emissions. This target is to take ?nal investment decisions on new energy products and lower carbon services by 2030, with total abatement capacity of 5 Mtpa CO -e. 2 The customers for these products and services may be the same as the customers of our oil and gas business, directly substituting their energy for new products or directly abating the associated emissions. They may also be customers of the new products and services, without also being customers of oil and gas. Our methodology for reporting emissions in these different circumstances is described on page 75-76. SCOPE 3 EMISSIONS Investment target1 Emissions abatement target1 Investment in new energy Take FID on new energy products products and lower carbon and lower carbon services by 2030, services by 2030 with total abatement capacity of $ 5BILLION2 5MTPA CO?-e3 1 Scope 3 targets are subject to commercial arrangements, commercial feasibility, regulatory and Joint Venture approvals, and third party activities (which may or may not proceed). Individual investment decisions are subject to Woodside?s investment targets. Not guidance. Potentially includes both organic and inorganic investment. 2 Includes pre-RFSU spend on new energy products and lower carbon services that can help our customers decarbonise by using these products and services. It is not used to fund reductions of Woodside?s net equity Scope 1 and 2 emissions which are managed separately through asset decarbonisation plans. 3 Includes binding and non-binding opportunities in the portfolio, subject to commercial arrangements, commercial feasibility, regulatory and Joint Venture approvals, and third party activities (which may or may not proceed). Individual investment decisions are subject to Woodside?s investment targets. Not guidance. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 34

|

天然气是生产氨的原料,氨在农业中用于 化肥。伍德赛德?2023年全球气候变迁行动计划与进展报告Woodside Energy Group Limited 35

|

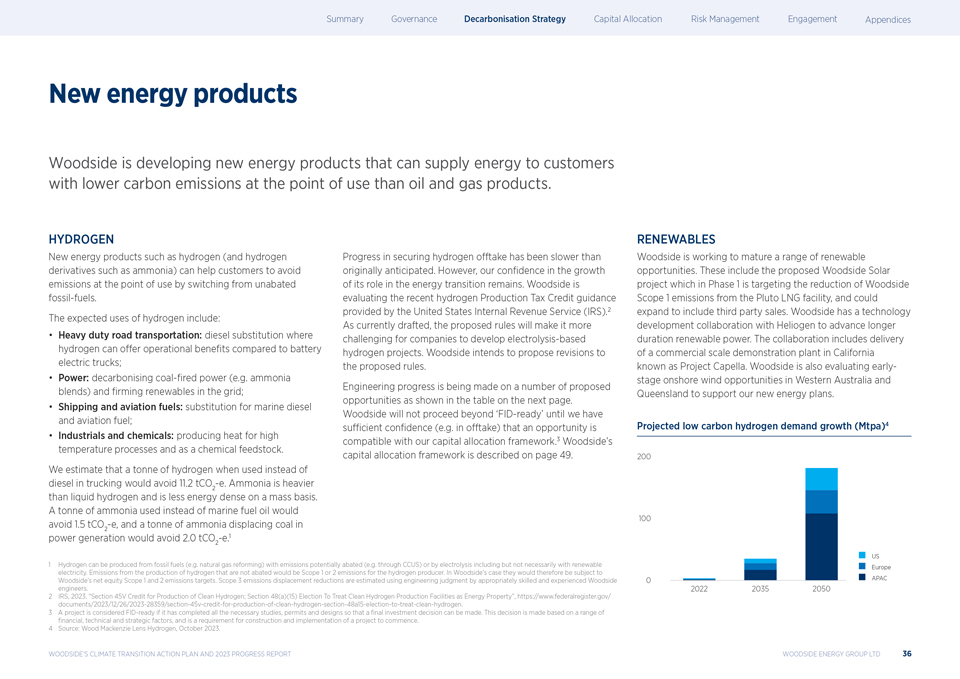

New energy products Woodside is developing new energy products that can supply energy to customers with lower carbon emissions at the point of use than oil and gas products. HYDROGEN New energy products such as hydrogen (and hydrogen derivatives such as ammonia) can help customers to avoid emissions at the point of use by switching from unabated fossil-fuels. The expected uses of hydrogen include: Heavy duty road transportation: diesel substitution where hydrogen can offer operational bene?ts compared to battery electric trucks; Power: decarbonising coal-?red power (e.g. ammonia blends) and ?rming renewables in the grid; Shipping and aviation fuels: substitution for marine diesel and aviation fuel; Industrials and chemicals: producing heat for high temperature processes and as a chemical feedstock. We estimate that a tonne of hydrogen when used instead of diesel in trucking would avoid 11.2 tCO -e. Ammonia is heavier than liquid hydrogen and is less energy 2 dense on a mass basis. A tonne of ammonia used instead of marine fuel oil would avoid 1.5 tCO -e, and a tonne of ammonia displacing coal in 2 power generation would avoid 2.0 tCO -e.1 2 Progress in securing hydrogen offtake has been slower than originally anticipated. However, our con?dence in the growth of its role in the energy transition remains. Woodside is evaluating the recent hydrogen Production Tax Credit guidance provided by the United States Internal Revenue Service (IRS).2 As currently drafted, the proposed rules will make it more challenging for companies to develop electrolysis-based hydrogen projects. Woodside intends to propose revisions to the proposed rules. Engineering progress is being made on a number of proposed opportunities as shown in the table on the next page. Woodside will not proceed beyond ?FID-ready? until we have sufficient confidence (e.g. in offtake) that an opportunity is compatible with our capital allocation framework.3 Woodside?s capital allocation framework is described on page 49. RENEWABLES Woodside is working to mature a range of renewable opportunities. These include the proposed Woodside Solar project which in Phase 1 is targeting the reduction of Woodside Scope 1 emissions from the Pluto LNG facility, and could expand to include third party sales. Woodside has a technology development collaboration with Heliogen to advance longer duration renewable power. The collaboration includes delivery of a commercial scale demonstration plant in California known as Project Capella. Woodside is also evaluating early-stage onshore wind opportunities in Western Australia and Queensland to support our new energy plans. Projected low carbon hydrogen demand growth (Mtpa)4 1 Hydrogen can be produced from fossil fuels (e.g. natural gas reforming) with emissions potentially abated (e.g. through CCUS) or by electrolysis including but not necessarily with renewable electricity. Emissions from the production of hydrogen that are not abated would be Scope 1 or 2 emissions for the hydrogen producer. In Woodside?s case they would therefore be subject to Woodside?s net equity Scope 1 and 2 emissions targets. Scope 3 emissions displacement reductions are estimated using engineering judgment by appropriately skilled and experienced Woodside engineers. 2 IRS, 2023. ?Section 45V Credit for Production of Clean Hydrogen; Section 48(a)(15) Election To Treat Clean Hydrogen Production Facilities as Energy Property?, https://www.federalregister.gov/ documents/2023/12/26/2023-28359/section-45v-credit-for-production-of-clean-hydrogen-section-48a15-election-to-treat-clean-hydrogen. 3 A project is considered FID-ready if it has completed all the necessary studies, permits and designs so that a ?nal investment decision can be made. This decision is made based on a range of ?nancial, technical and strategic factors, and is a requirement for construction and implementation of a project to commence. 4 Source: Wood Mackenzie Lens Hydrogen, October 2023. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 36

|

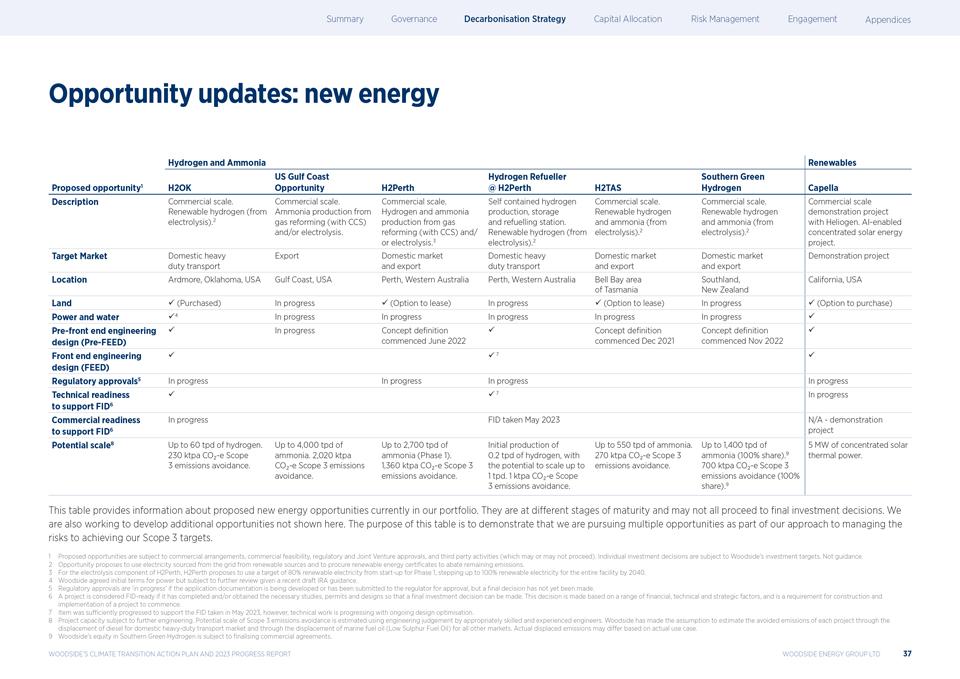

机会更新:新能源氢气和氨 可再生能源美国墨西哥湾沿岸氢气加油商Southern Green提议的机会1 H2 OK机会H2 Perth@H2 Perth H2 TAS氢Capella描述商业规模。商业规模。商业规模。自含式氢气商业规模。 商业规模。工业规模可再生氢(来自制氢制氨、储存可再生氢可再生氢示范项目电解)2.气体重整(带CCS)从天然气生产和加气站。和氨(来自)和氨(来自氦。人工智能启用和/或电解。重整(使用CCS)和/或可再生氢(来自电解).2.电解).2.集中太阳能或电解.3.电解).目标市场国内重型出口国内市场重型国内市场国内市场示范项目关税运输和出口关税运输以及出口和出口地点阿德莫尔,俄克拉何马州,美国墨西哥湾,美国珀斯,西澳大利亚州珀斯,西澳大利亚州贝尔湾区南区,加利福尼亚州,美国塔斯马尼亚州新西兰土地??(购买)正在进行??(选择租赁)正在进行??(选择租赁)正在进行??(选择购买)水电?4正在进行中?前端工程?正在进行的概念定义?概念定义?设计(进料前)2022年6月开始2021年12月开始2022年11月前端工程?7?设计(FEED)监管审批5正在进行技术准备??7正在进行以支持FID6正在进行的商业准备FID 2023年5月不适用演示以支持FID6项目的潜在规模8至60吨/日的氢气。日产量高达4,000吨,初期日产量高达2,700吨,氨日产量高达550吨。高达1,400吨/日的5兆瓦聚光太阳能230吨/年的CO?-E示踪器氨。2,020 ktpa氨(第一阶段)。每天0.2tpd的氢气,270ktpa的CO?-e示波器3氨(100%份额).9火力。3避免排放。CO?-E范围3排放1,360 ktpa CO?-E范围3扩大到避免排放的可能性。700 ktpa CO?-E范围3避让。避免排放 。1 tpd。1 ktpa CO?-E范围排放避免(100%3排放避免此表提供了有关我们目前投资组合中的拟议新能源机会的信息。它们处于不同的成熟阶段,可能不会全部进入投资决策阶段。我们还在努力开发这里没有显示的更多机会。此表的目的是展示我们正在寻求多个机会作为我们管理风险的方法的一部分 以实现我们的范围3目标。1建议的机会取决于商业安排、商业可行性、监管和合资企业的批准,以及第三方活动(可能进行也可能不进行)。个人投资 以伍德赛德?S的投资目标为准。而不是指导。机遇号建议使用来自可再生能源的电网电力,并采购可再生能源证书,以减少剩余的排放。3对于H2 Perth的电解组件,H2 Perth建议在第一阶段使用80%的可再生电力,到2040年整个设施的可再生电力逐步达到100%。4伍德赛德同意了权力的初步条款,但 根据最近的爱尔兰共和军指导草案进行了进一步审查。5监管审批正在进行中吗?申请文件正在编制或已提交监管机构审批,但尚未做出最终决定的 。6如果一个项目已经完成和/或获得了必要的研究、许可和设计,以便作出投资决定,则该项目被视为FID准备就绪。这一决定是基于一系列财务、技术和战略因素作出的,是项目开始建设和实施的要求。7项工作进展充分,足以支持2023年5月进行的FID,然而,技术工作正在进行设计优化。8项目 容量有待进一步设计。范围3排放避免的潜在规模是由具有适当技能和经验的工程师利用工程判断来估计的。伍德赛德假设通过为国内重型运输市场置换柴油和通过为所有其他市场置换船用燃料油(低硫燃料油)来估计每个项目的避免排放量。实际置换排放可能会根据实际使用案例而有所不同。 9伍德赛德?S在南方绿色氢气的股权有待最终敲定商业协议。伍德赛德?S气候转型行动计划和2023年进展报告伍德赛德能源集团有限公司37

|

低碳服务伍德赛德正在开发可减少客户排放的低碳服务。碳捕获和储存CCS是一项成熟的技术,代表了一种经过验证的减少大规模工业排放的解决方案。像CCS这样的服务可以帮助客户减少他们在使用Woodside产品(或来自其他来源的类似产品)时会产生的排放。由于CCS也是减少我们资产中伍德赛德?S范围1排放的解决方案,因此我们有潜力在客户需求发展的同时支持我们自己使用的CCS项目的开发。我们相信CCS将在能源转型中发挥越来越大的作用,伍德赛德也拥有竞争优势,包括其在地球科学、地下工程和散装天然气处理方面的知识。碳信用组合我们的碳信用组合主要是为了解决伍德赛德?S范围1和2的排放问题而开发的(见第28-31页)也可以出售,以抵消客户的排放。我们目前正在探索向与我们的碳氢化合物产品捆绑在一起的客户提供碳信用的机会,例如来自斯卡伯勒的液化天然气货物。在过去,我们为相关的范围1和2的排放提供货物的碳信用。碳捕获和利用从长远来看,碳捕获和利用(CCU,也称为碳转化产品)有可能大规模利用第三方来源的CO。2 2023年,伍德赛德与CCU技术开发商LanzaTech、NovoNutrients、StringBio和几家工程公司一起完成了多项工程研究 。这些研究有助于了解如何整合和优化他们的技术,以将温室气体转化为各种有用的产品。 Woodside是莫纳什大学RECARB ARC Hub的创始合作伙伴,该中心正在探索直接空气捕获CO用于产品。2 CCS在科学途径中的作用?CO捕获和地下注入是一项成熟的天然气处理和提高石油采收率的技术2。与石油和天然气部门相比,CCS在电力部门以及水泥和化学品生产方面不那么成熟,在这些领域,CCS是一个关键的缓解选择。技术地质CO存储容量估计约为1,000~20亿吨CO,高于将全球变暖控制在1.5摄氏度以内的CO存储需求2到2100,尽管区域地质存储的可用性可能是一个限制因素 。如果适当地选择和管理地质储存地点,估计可以将CO与大气永久隔离2。CCS的实施目前面临技术、经济、体制、生态环境和社会文化障碍。目前,全球部署CCS的速度远远低于将全球变暖限制在1.5摄氏度或2摄氏度以内的模拟路径。政策手段、更大的公共支持和技术创新等有利条件可以减少这些障碍。气专委第六次评估报告1气专委2022年。《2022年气候变化:减缓气候变化》。第三工作组对政府间气候变化专门委员会第六次评估报告的贡献?供决策者参考的摘要,第C.4.6段。伍德赛德?S气候转型行动计划和2023年进展报告伍德赛德能源集团有限公司38

|

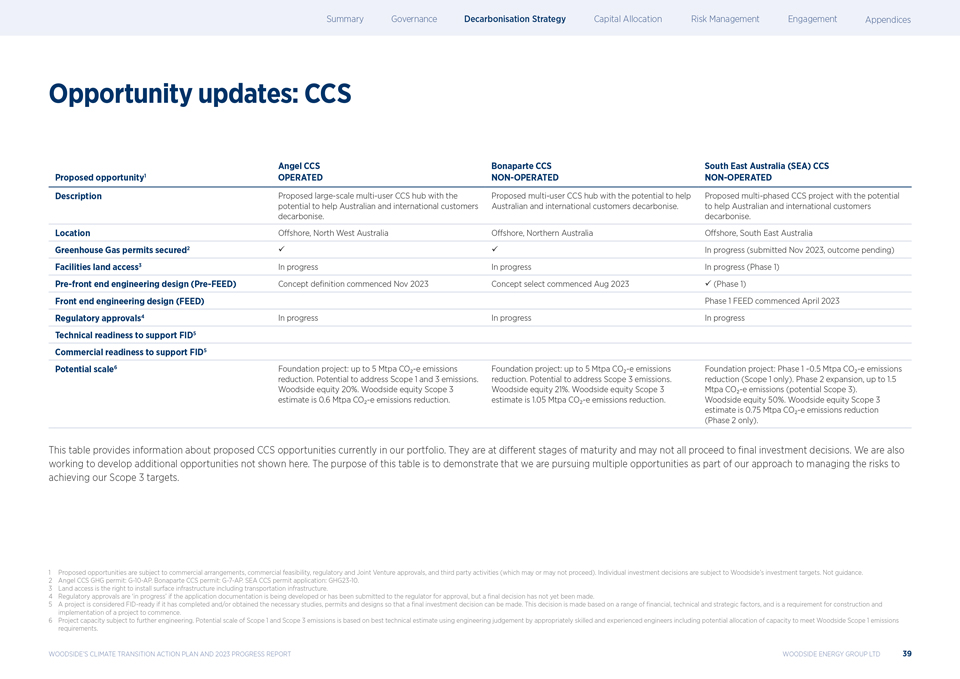

Opportunity updates: CCS Angel CCS Bonaparte CCS South East Australia (SEA) CCS Proposed opportunity(1) OPERATED NON-OPERATED NON-OPERATED Description Proposed large-scale multi-user CCS hub with the Proposed multi-user CCS hub with the potential to help Proposed multi-phased CCS project with the potential potential to help Australian and international customers Australian and international customers decarbonise. to help Australian and international customers decarbonise. decarbonise. Location Offshore, North West Australia Offshore, Northern Australia Offshore, South East Australia Greenhouse Gas permits secured(2) 9 9 In progress (submitted Nov 2023, outcome pending) Facilities land access(3) In progress In progress In progress (Phase 1) Pre-front end engineering design (Pre-FEED) Concept definition commenced Nov 2023 Concept select commenced Aug 2023 9 (Phase 1) Front end engineering design (FEED) Phase 1 FEED commenced April 2023 Regulatory approvals(4) In progress In progress In progress Technical readiness to support FID(5) Commercial readiness to support FID(5) Potential scale(6) Foundation project: up to 5 Mtpa CO -e emissions Foundation project: up to 5 Mtpa CO -e emissions Foundation project: Phase 1 ~0.5 Mtpa CO -e emissions reduction. Potential to address Scope 1 and 3 emissions. reduction. Potential to address Scope 3 emissions. reduction (Scope 1 only). Phase 2 expansion, up to 1.5 Woodside equity 20%. Woodside equity Scope 3 Woodside equity 21%. Woodside equity Scope 3 Mtpa CO -e emissions (potential Scope 3). estimate is 0.6 Mtpa CO -e emissions reduction. estimate is 1.05 Mtpa CO -e emissions reduction. Woodside equity 50%. Woodside equity Scope 3 estimate is 0.75 Mtpa CO -e emissions reduction (Phase 2 only). This table provides information about proposed CCS opportunities currently in our portfolio. They are at different stages of maturity and may not all proceed to ?nal investment decisions. We are also working to develop additional opportunities not shown here. The purpose of this table is to demonstrate that we are pursuing multiple opportunities as part of our approach to managing the risks to achieving our Scope 3 targets. 1 Proposed opportunities are subject to commercial arrangements, commercial feasibility, regulatory and Joint Venture approvals, and third party activities (which may or may not proceed). Individual investment decisions are subject to Woodside?s investment targets. Not guidance. 2 Angel CCS GHG permit: G-10-AP. Bonaparte CCS permit: G-7-AP. SEA CCS permit application: GHG23-10. 3 Land access is the right to install surface infrastructure including transportation infrastructure. 4 Regulatory approvals are ?in progress? if the application documentation is being developed or has been submitted to the regulator for approval, but a final decision has not yet been made. 5 A project is considered FID-ready if it has completed and/or obtained the necessary studies, permits and designs so that a ?nal investment decision can be made. This decision is made based on a range of ?nancial, technical and strategic factors, and is a requirement for construction and implementation of a project to commence. 6 Project capacity subject to further engineering. Potential scale of Scope 1 and Scope 3 emissions is based on best technical estimate using engineering judgement by appropriately skilled and experienced engineers including potential allocation of capacity to meet Woodside Scope 1 emissions requirements. WOODSIDE?S CLIMATE TRANSITION ACTION PLAN AND 2023 PROGRESS REPORT WOODSIDE ENERGY GROUP LTD 39

|